Download

1 / 9

90 likes | 223 Views

Integrating Renewables on the Grid: Meeting the Challenge of the Midwest's Energy Future. Melissa Seymour Midwest Market Structure Iberdrola Renewables June 7, 2010 Mid-America Regulatory Conference Kansas City, MO. Elk River Wind Power Project, Kansas.

E N D

Integrating Renewables on the Grid: Meeting the Challenge of the Midwest's Energy Future Melissa Seymour Midwest Market Structure Iberdrola Renewables June 7, 2010 Mid-America Regulatory Conference Kansas City, MO Elk River Wind Power Project, Kansas

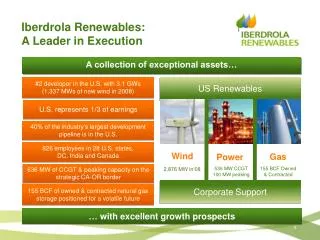

Iberdrola Renewables:A Leader in Execution A collection of exceptional assets… US Renewables #2 developer in the U.S. with nearly 3.6 GWs(1,311 MWs of wind started up in 2009) U.S. represents 1/3 of earnings 24.5 GWs of wind development pipeline is in the U.S. 851 employees in 28 U.S. states, DC, and Canada Wind Gas Power 521 MW CCGT100 MW peaking 155 BCF Owned & Contracted 3,600+ MW 621 MW of CCGT & peaking capacity on the strategic CA-OR border Corporate Support 155 BCF of owned & contracted natural gas storage positioned for a volatile future … with excellent growth prospects Updated Feb. 23, 2010

Mid-Continent Wind Assets Rugby 149.1 MW Owned Moraine 51 MW Owned Moraine II 49.5 MW Owned MinnDakota 150 MW Owned Trimont 101 MW Owned Top of Iowa II 80 MW Owned Buffalo Ridge 50.4 MW Owned Barton 160 MW Owned Elm Creek99 MW Owned Flying Cloud 43.5 MW Owned Streator Cayuga Ridge300 MW Owned Winnebago 20 MW Owned Farmers City 146 MW Owned ProvidenceHeights 72 MW Owned Elk River 150 MW Owned Barton Chapel 120 MW Owned MID-CONTINENT REGION Operating wind projects Penascal 202 MW Owned Updated March 1, 2010

U.S. Markets for Renewable Energy: 28 states with mandatory RPS requirements • States with circles: • RPS • high KWh use • high electricity price Those states ~= 50% of US KWh (map shows population density) Source of maps: UCS, US Census

Connecting Renewables to Loads The best wind resources in the U.S. are located in areas where the grid is the weakest Source of maps: NREL, Platts

Wind Integration Solutions Storage Additional Flexible Generation Pumped Storage Batteries Flywheels SMES CAES Capacitors PHEV Wind Curtailment Simple Cycle GT Combined Cycle GT Markets In Range of 1-2% AccurateForecasting Accessing Intra-hour flexibility Price Responsive Load Demand ResponseDynamic Scheduling Real time forecastingCentralized Forecasting High Cost Integrating wind is a cost issue, not a reliability issue Low Cost Low Wind Penetration Level High Wind Penetration Level Source: UWIG

Mid-Continent Market Attributes for Optimal Wind Integration

Summary • The Mid-Continent has many favorable market attributes for cost-effectively integrating renewables • Successful wind integration in the Mid-Continent will require transmission expansion - transmission costs are a small fraction of the total costs of the power system • Incenting accurate forecasting and incorporating forecasting in system operations will significantly reduce the uncertainty about future wind output • Need to continue to develop market rules, processes, incentives, and products that ensure that low-cost wind integration solutions are developed prior to implementing higher costs solutions

Questions? Melissa Seymour melissa.seymour@iberdrolausa.com 503-708-8148 Big Horn Wind Power Project, Washington