Download

1 / 24

250 likes | 399 Views

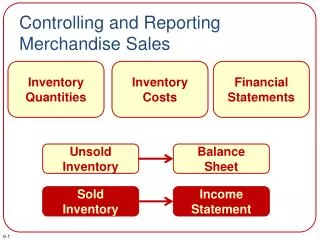

Chapter 7 Merchandise Inventory and Cost of Sales. In this chapter…. Inventory Items and Cost. Merchandise Inventory (Inventory) – includes all items held by the organization for sale

E N D

Chapter 7Merchandise Inventory and Cost of Sales Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

In this chapter… Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Inventory Items and Cost • Merchandise Inventory (Inventory) – includes all items held by the organization for sale • Items are considered inventory items if they contribute to the regular on-going operations of the company. Example • A car used by a business to help make deliveries is a fixed asset, • Cars on a car dealer’s lot intended for resale as part of the on-going operations would be considered inventory Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Inventory Items and Cost • Goods in transit • deemed to be owned by the trading partner responsible for it (who bears the rights and risks of ownership) at any given time. • A good indicator is the FOB terms (FOB destination, or factory or somewhere in the middle) • Consignment • goods shipped by the owner to another party who sells them on behalf of the owner • Consignment inventory is owned by the original owner and is held on their balance sheet • Goods Damaged or Obsolete • Non-sellable goods cannot be counted in inventory as they are no longer an asset (they can’t be used to create revenue) • If they are sellable, they should be included in inventory at a reduced cost to reflect their reduced value Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Costs of Merchandise Inventory • Costs are • Those costs needed to directly or indirectly bring the item to saleable condition and location • Would include the invoice cost of the goods plus • shipping, insurance, duties, storage, less, discounts Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Capitalization • Capitalization – To record an expenditure as an asset and thereby defer its recognition as an expense at a later point • Costs which are intended to provide some future benefit are capitalized • Ex: purchase of buildings, trucks, other fixed or “capital” assets • When costs (like direct labour, delivery costs) associated with inventory are incurred, they are rolled into inventory (or, capitalized into inventory) and expensed as part of COGS when the inventory is sold • Capitalization is founded on the matching principle. If a cost will only support future revenues, it is capitalized as an asset until the revenue is realized • When to capitalize and when not to: • If a cost is directly related to “building up” an asset, it needs to be capitalized along with that asset (as per previous examples) • If costs are not directly related to a specific asset, then they are expensed in the period in which they occur (like rent, insurance, hydro, etc) Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Physical Count • Units on hand need to be confirmed through a physical count on a periodic basis • Usually occurs at the end of a fiscal year. • The physical count is used to adjust the inventory value on the books by either debiting CoGS (if the count is less that expected) or crediting CoGS (if it is more) • This end of period catch-all adjustment will account for damage, theft, obsoletion, errors in data entry Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Assigning Costs to Inventory • One of the most important items is to determine inventory costs • Easy to do when all items are purchased at identical per unit costs, • More difficult to do when identical items are purchased at different costs (due to inflation, purchase volumes, duties, insurance, etc) • When sales are made, using a perpetual inventory system, one needs to assign costs to the COGS account on a per sale/per unit basis • 4 ways to assign costs to inventory and COGS • Specific Identification • Moving Weighted Average • First-In, First-Out • Last-In, First-Out • All 4 messages are cool under GAAP, although LIFO is not acceptable for tax purposes or if reporting under the new IFRS rules Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Specific Identification • Specific Identification – as it implies, allows the accountant to specifically identify a cost/invoice with a piece of inventory. • Works best when each item is unique and identifiable • Applicable for art galleries, some auto dealerships, custom furniture • Requires that the inventory be tracked to specific items (through a serial number) • Calculating the Inventory is simply adding up the costs relating to each item in the inventory • Similarly, COGS is calculated by simply noting/adding the cost of the item sold. Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Moving Weighted Average • Weighted Average – a computed cost per unit of inventory. • The average is calculated at each time of purchase • Weighted Average = Total Cost of all Inventory/Total Qty Units • Requires that the inventory value be recalculated at every purchase of inventory Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

First-In, First-Out (FIFO) • As implied, this method assumes the first items bought for inventory are the first items sold. • When sales are made, the costs of the earliest units in inventory are applied to arrive at COGS • Requires that the inventory be tracked in lots of units purchased Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Last-In, First-Out (LIFO) • As implied, this method assumes that the most recently purchased goods are those sold first, thus the latest units in inventory are assigned to COGS • Because LIFO assumes the latest items are applied to COGS, it may be a more close approximation of costs to revenues (matching principle) • But in markets where pricing is generally rising, it means that Net Income can be reduced since more recent units would have higher costs Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Mid-Chapter Demo Problem • Lets look at the mid-chapter demo problem • Use each of FIFO, LIFO, WA and SI to calculate Inventory and COGS for the Tale Company scenario Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Inventory and Financial Reporting • As you can see, the method used for inventory valuation can have an effect on the value of Inventory and COGS. • Of course this only applies when inventory pricing is changing, but when does it not change??? • Therefore, the inventory valuation method must be disclosed in the financial statements (required by GAAP). • This is called the Full Disclosure Principle • The Consistency Principle requires that companies adhere to a consistent valuation method (this actually applies to all aspects of the accounting) • Note: that companies can use different methods for valuing different portions of their inventory • Also, companies can change their valuation methods, but they must justify the change as improving the quality of the reporting, not improving the outcome of the reports Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Trends • FIFO always uses the oldest unit prices for COGS • Therefore in a rising prices market, Net Income is always higher than what would be calculated by WA or LIFO • In a falling prices market, LIFO would calculate Net Income as higher than FIFO • Generally, WA is somewhere in the middle of LIFO and FIFO Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Conservatism • Conservatism Principle – requires that inventory be reported at the lower of cost or market value • The least optimistic value should always be chosen (this applies to all aspects of accounting) • If changes in market value cause there to be a requirement to restate inventory, adjustments are made to end of period adjusting entries…. Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Adjusting Entries • If inventory was previously stated at cost of 1000, but market has now fallen to 900, then the adjusting entry is: • The inventory line item on the Balance Sheet would then read 900 and the COGS line item in the Income Statement would be 100 more than otherwise stated Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Effect of Errors • Incorrectly stating inventory value has a large and cascading effect. It effects • Inventory on the balance sheet • Owner’s Equity • COGS • Net Income • Plus in the following period (since ending inventory from a previous period is the starting inventory for the next period), the above errors would continue • When one considers that lenders, shareholders and internal staff make decisions based on this info, the effects broaden further Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Estimating Inventory • Why would we want to estimate inventory? • Sometimes inventory information is incomplete, due to obsolescence, destruction, etc • We can use the historical connection between COGS and Net sales to determine the proportion of COGS making up current Net sales (extrapolation) • Gross Profit Method • Uses the above ratio (previous COGS to Net Sales ratio) to extrapolate current COGS from current Net Sales. • Once we calculate current COGS, we can subtract it from beginning inventory balance to determine end of period inventory balance Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Estimating Inventory • We won’t cover this in detail, but FYI • Retail Inventory Method • Again, a method to estimate COGS and ending inventory without having to take a physical inventory count • To calculate using the Retail Inventory Method, you need • Beginning period balance of inventory at both cost and selling prices • Both cost and selling prices of any purchases during the period • The amount of net sales at retail • Follow Exhibit 7.18 and review Exhibit 7.19 Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Estimating Shortage • Inventory can be short due to a number of reasons (theft, obsolescence, spoilage, etc) • You can estimate shortage by subtracting the estimated inventory cost as calculated in the Retail Inventory Estimating method from the actual physical count Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Prepping for the Mid-term Exam • The Mid-term exam • Covers Chapters 1 to 7 • Closed book • Please bring a calculator • You can’t bring in a consultant, chartered accountant, CMA or CGA. • I will hand out a question sheet, you need to provide your own answer paper • A typical exam question will cover the various exercises and problems we have been covering • There is no multiple choice, no essay type questions. • It will just be based on business transactions and business events Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

A Typical Mid-term Exam Question • Present a series of business transactions and events • You’ll be asked to prepare • the journal entries (ensure you label them (a), (b), etc) • show the journal entries in T-accounts (make sure you label the transactions (a), (b),…, in the T-accounts • Create the unadjusted trial balance • Show the various calculations to complete the end of period adjustments • Complete the journal entries to adjust (again, use labeling) • Prepare the adjusted trial balance • Prepare the closing entries and journalize (label them) • Prepare the post closing trial balance • Complete an Income Statement, Balance Sheet (with proper classifications) and Statement of Owner’s Equity • MAKE SURE YOU FINISH THE STATEMENTS even if your numbers are not accurate Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD

Onward… • Chapter 9 Financial Accounting Dave Ludwick, P.Eng, MBA, PMP, PhD