Download

1 / 7

70 likes | 92 Views

Learn about different types of transactions like asset purchase, stock purchase, mergers, and more, and their tax consequences. Explore asset allocation, taxable transactions, goodwill treatment, and installment sales.

E N D

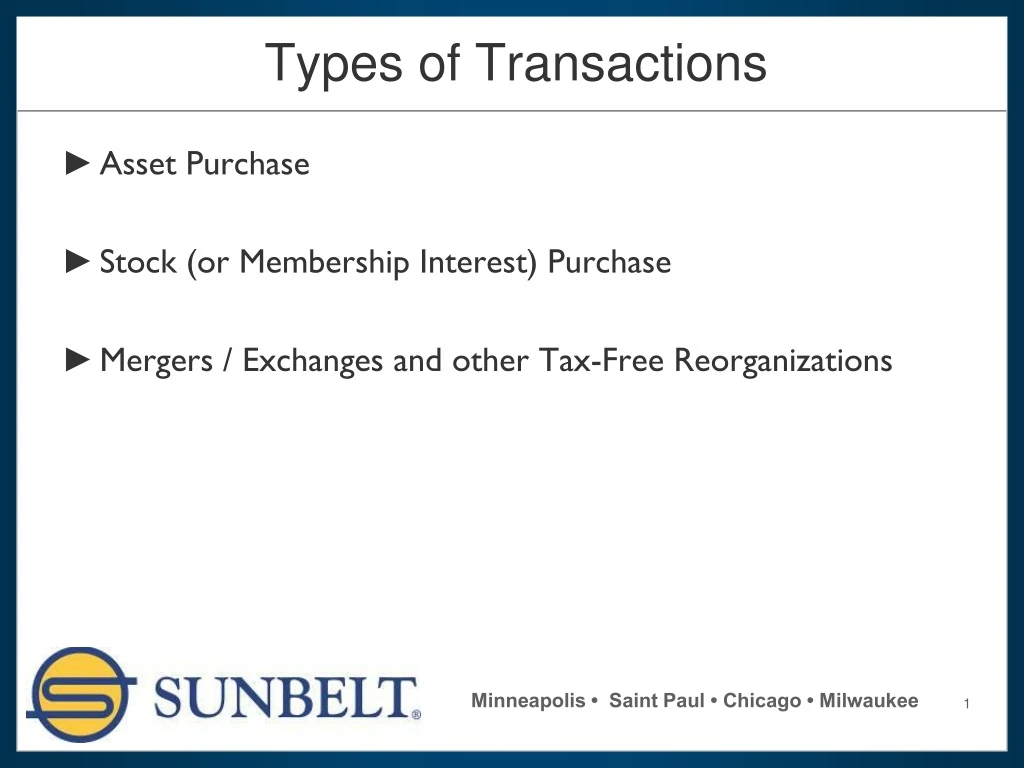

Types of Transactions Asset Purchase Stock (or Membership Interest) Purchase Mergers / Exchanges and other Tax-Free Reorganizations

Taxable TransactionsAsset Transactions Allocation of Purchase Price • Accounts Receivable • Seller: ordinary income • Buyer: carry at allocated value • Inventory • Seller: ordinary income • Buyer: carry at allocated value

Taxable TransactionsAsset Transactions Allocation of Purchase Price • Depreciable Assets (Personal Property) • Seller: ordinary income to the extent of depreciation recapture • Buyer: carry at allocated value and depreciate (fresh start) • Real Estate • Land • Seller: capital gain • Buyer: carry at allocated value • Building • Seller: recapture / capital gain • Buyer: depreciate

Taxable TransactionsAsset Transactions Allocation of Purchase Price • Goodwill • Seller: capital gain • Buyer: capitalize and amortize over 15 years • Non-Compete Payments • Seller: ordinary income • Buyer: capitalize and amortize over 15 years • Consulting Payments • Seller: ordinary income subject to FICA • Buyer: current deduction

Taxable TransactionsAsset Transactions Installment Sales • A portion of the Seller’s gain can be deferred until such time as the Seller receives the principal payments under the promissory notes. • A portion of each payment received by the Seller will be treated in part as (i) a nontaxable recovery of the Seller’s basis in the property and (ii) a gain equal to the amount of the payment multiplied by the gross profit percentage on the sale. • Seller must receive at least one payment in a year after the close of the tax year in which the disposition occurs.

Personal GoodwillWhy do you care? Personal Goodwill Generally • May be owned/property of shareholders, members or partners • Sold separately from business assets or equity • Can result in favorable tax treatment is C corporation is involved • NEED FACTS TO SUPPORT ITS EXISTENCE

Personal GoodwillProfile C Corporation Closely Held • Prerequisite • Identity of business and owner intertwined Technical or professional businesses • Value comes from owners education, reputation and experience Few customers or suppliers • Relationships are key • Vendor deals add value