Download

1 / 66

680 likes | 899 Views

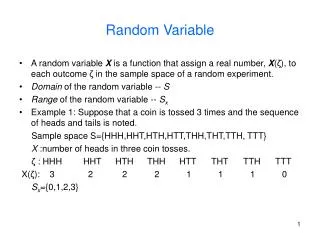

Discrete Random Variable. Let X denote the return of the S&P 500 tomorrow, rounded to the nearest percent what are the possibilities, i.e. 0, 1%, … what is the probability of each of the above possibilities Probability distribution function: f ( x ) = P ( X=x ).

E N D

Discrete Random Variable • Let X denote the return of the S&P 500 tomorrow, rounded to the nearest percent • what are the possibilities, i.e. 0, 1%, … • what is the probability of each of the above possibilities • Probability distribution function: f(x) = P(X=x)

Discrete Random Variable • Expectation • Variance

Expectation of a Function of a R.V. • Function g(X): • What is the expectation E(g(X))? • General result: • Example – call option on the S&P 500

Binomial Distribution • Bernoulli distribution • A r.v. X has two possible outcomes, 0 or 1 • Binomial distribution • Number of successes that occur in n trials • Example: Ch. 4, 6b

Poisson • A r.v. X takes on values 0, 1, 2, .... • Poisson distribution iffor some l > 0, • The Poisson r.v. is an approximation for binomial with l = np. • Example: how many days in a year will the S&P500 drop more than 1%? • Example 7b

Geometric • Independent trials with prob. of success p • How many trials until a success occurs? • What happens when n goes to infinity? • Example: how many days until we get a stock market drop of 2% or more?

Negative Binomial • Independent trials with prob. of success p • How many trials until r successes occur? • What happens when n goes to infinity? • Example: how many days until we get three stock market drops of 2% or more (not necessarily consecutive)?

Hyper-Geometric • Choose n balls out of N, without replacement • m white, N – m black • X = number of white balls selected • Example 8i • What happens if you choose the n balls with replacement?

Continuous Random Variable • Let X denote the return of the S&P 500 tomorrow, no rounding • what are the possibilities • what is the probability of each of the above possibilities • Probability density function:

Continuous Random Variable • Expectation • Variance • Example Ch5, 1a, 1b, 2a

Continuous Random Variable • For any real-valued function g and continuous r.v. X: • Example: payoff on a call option, 2b

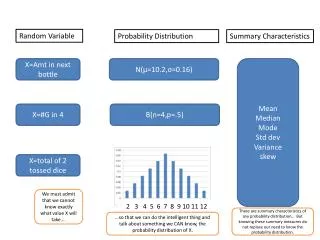

Additional Sample Questions • Given a discrete probability function (pdf) (i.e., all possible outcomes and their probabilities), compute the mean and the variance • Given a graph of several discrete or continuous pdf, estimate which ones has the highest mean, variance, skewness, kurtosis • Given two random variables, guess whether they have positive or negative covariance and/or correlation

The Uniform Distribution Example 3b

The Normal Distribution Example Ch 5, 4b, 4e

Normal is an Approximation to Binomial • Sn = number of successes in n independent trials with individual prob. of success p. • The DeMoivre-Laplace limit theorem:

Lognormal Distribution • What is the distribution of the S&P 500 index tomorrow? • If the return on the S&P500 is normally distributed, the index itself is lognormally distributed

Chi-squared Distribution • Sum of squared standard normal variables

F distribution • Ratio of two independent chi-squared variables with degrees of freedom n1 and n2

t distribution • Very important for hypothesis testing

Exponential Distribution • PDF: • CDF: • Exercise:

Joint Distributions of R. V. • Joint probability distribution function: f(x,y) = P(X=x, Y=y) • Example Ch 6, 1c, 1d

Independence • Two variables are independent if, for any two sets of real numbers A and B, • Operationally: two variables are indepndent iff their joint pdf can be “separated” for any x and y:

Joint Distributions of R. V. • The expectation of a sum equals the sum of the expectations: • The variance of a sum is more complicated: • If independent, then the variance of a sum equals the sum of the variances

Additional Sample Questions • Find the distribution of a transformation of two or more normal random variables • By looking at a graph of a pdf, guess whether it is normal, log-normal, or t-distribution • What normally distributed random variables do you need to construct an F distribution with 3 and 5 degrees of freedom

Conditional Distributions (Discrete) • For any two events, E and F, • Conditional pdf: • Examples Ch 6, 4a, 4b

Conditional Distributions (Discrete) • Conditional cdf:

Conditional Distributions (Discrete) • Example: what is the probability that the TSX is up, conditional on the S&P500 being up?

Conditional Distributions (Continous) • Conditional pdf: • Conditional cdf: • Example 5b

Conditional Distributions (Continous) • Example: what is the probability that the TSX is up, conditional on the S&P500 being up 3%?

Joint PDF of Functions of R.V. • = joint pdf of X1 and X2 • Equations and can be uniquely solved for and given by: and • The functions and have continuous partial derivatives:

Joint PDF of Functions of R.V. • Under the conditions on previous slide, • Insert eq. 7.1, p275 • Example: You manage two portfolios of TSX and S&P500: • Portfolio 1: 50% in each • Portfolio 2: 10% TSX, 90% S&P 500 • What is the probability that both of those portfolios experience a loss tomorrow?

Joint PDF of Functions of R.V. • Example 7a – uniform and normal cases

Estimation • Given limited data we make educated guesses about the true parameters • Estimation of the mean • Estimation of the variance • Random sample