Download

1 / 1

10 likes | 169 Views

Materialism, the Love of Money, and Consumer Optimism in Spain Thomas Li-Ping Tang, Roberto Luna-Arocas, Ismael Quintanilla Pardo, Theresa Li-Na Tang E-Mail: ttang@mtsu.edu. Abstract

E N D

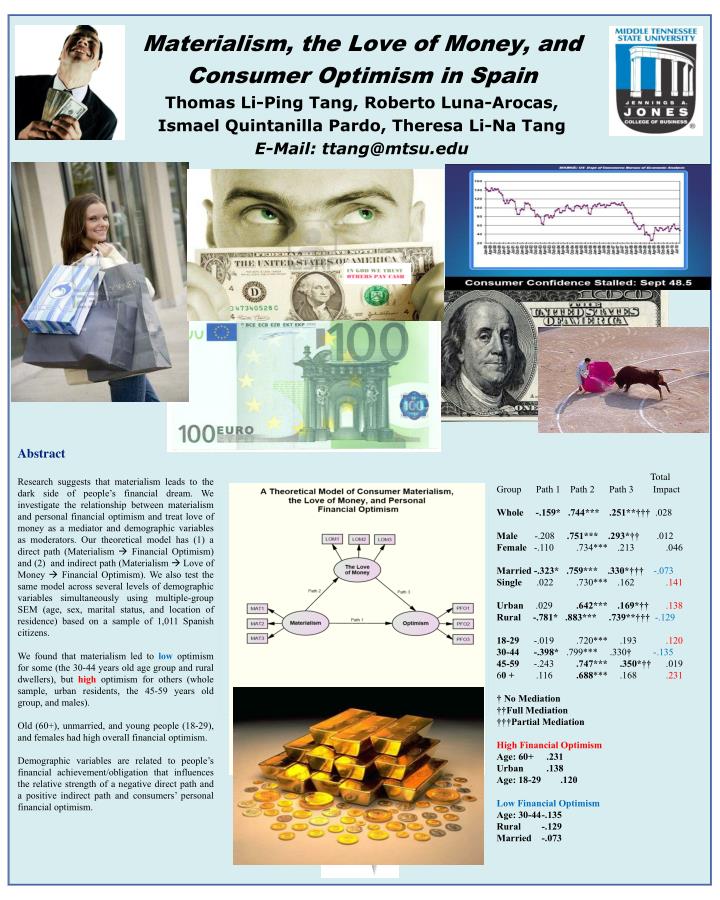

Materialism, the Love of Money, and Consumer Optimism in SpainThomas Li-Ping Tang, Roberto Luna-Arocas, Ismael Quintanilla Pardo, Theresa Li-Na TangE-Mail: ttang@mtsu.edu Abstract Research suggests that materialism leads to the dark side of people’s financial dream. We investigate the relationship between materialism and personal financial optimism and treat love of money as a mediator and demographic variables as moderators. Our theoretical model has (1) a direct path (Materialism Financial Optimism) and (2) and indirect path (Materialism Love of Money Financial Optimism). We also test the same model across several levels of demographic variables simultaneously using multiple-group SEM (age, sex, marital status, and location of residence) based on a sample of 1,011 Spanish citizens. We found that materialism led to low optimism for some (the 30-44 years old age group and rural dwellers), but high optimism for others (whole sample, urban residents, the 45-59 years old group, and males). Old (60+), unmarried, and young people (18-29), and females had high overall financial optimism. Demographic variables are related to people’s financial achievement/obligation that influences the relative strength of a negative direct path and a positive indirect path and consumers’ personal financial optimism. Total Group Path 1 Path 2 Path 3 Impact Whole-.159*.744***.251**††† .028 Male -.208 .751*** .293*†† .012 Female -.110 .734*** .213 .046 Married -.323* .759*** .330*††† -.073 Single .022 .730*** .162 .141 Urban .029 .642*** .169*††.138 Rural -.781* .883*** .739**††† -.129 18-29 -.019 .720*** .193 .120 30-44 -.398* .799*** .330† -.135 45-59 -.243 .747*** .350*†† .019 60 + .116 .688*** .168 .231 † No Mediation ††Full Mediation †††Partial Mediation High Financial Optimism Age: 60+ .231 Urban .138 Age: 18-29 .120 Low Financial Optimism Age: 30-44 -.135 Rural -.129 Married -.073