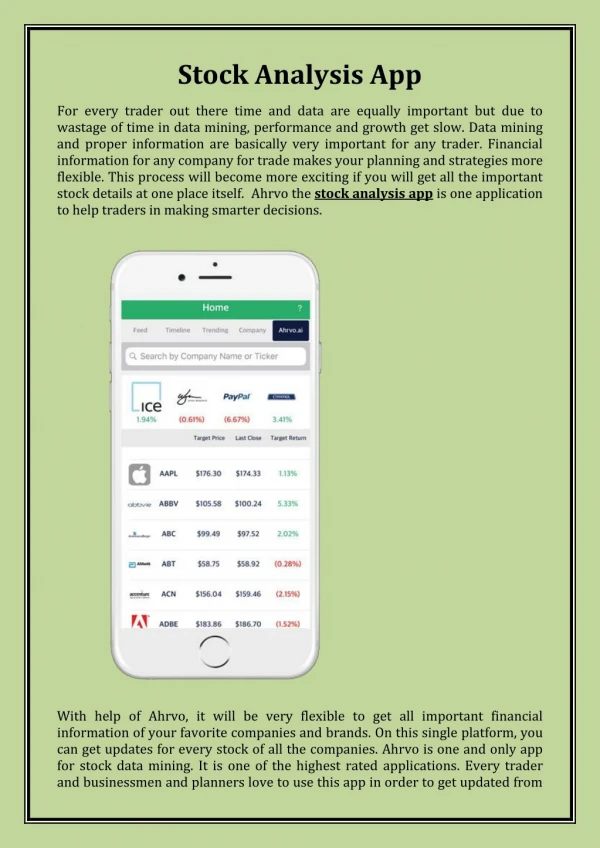

Download

1 / 27

270 likes | 404 Views

Initial Stock Analysis. Andrew Bentley February 8 , 2012. Outline. Price and returns for Apple Inc. (AAPL) and Ford Motor Inc. (F) Measures of Volatility RV, BV, Sub-Sampled RV, TV Volatility Signatures RV and BV Relative Contribution of Jumps Basic Comparison Between these Measures.

E N D

Initial Stock Analysis Andrew Bentley February 8, 2012

Outline • Price and returns for Apple Inc. (AAPL) and Ford Motor Inc. (F) • Measures of Volatility • RV, BV, Sub-Sampled RV, TV • Volatility Signatures • RV and BV • Relative Contribution of Jumps • Basic Comparison Between these Measures

Price and Returns • Unadjusted plots of price data against time • Adjusted plots of price data against time after correcting backwards for stock splits • Minute-by-minute geometric returns • “Returns” graphs consider intraday minute-by-minute returns as well as overnight returns.

AAPL: Unadjusted Prices 2:1 Split 2:1 Split

AAPL: Stock Splits • Three 2:1 Stock Splits • June 15, 1987 • June 21, 2000 • February 28 2005 • The June 2000, and February 2005 splits fall in the data range • Price adjusts “backwards” to account for the splits

F: Price Nov. 2006 Dec. 2008

Measures of Volatility • Goal is to measure the integrated variation • for a process: • The realized variance:

Estimators for IVt • Bipower Variation (BV): • Threshold/Truncated Variation (TV)

Truncated Variation, TVt(AAPL) • AAPL, cutoff of 4 standard deviations

Truncated Variation, TVt(F*) • F, cutoff of 4 standard deviations

Effects of Microstructure Noise • Observed data is actually some price plus some noise term • Look for ways to wash out the effect of the noise without loosing the vast majority of the data • Sub-Sampling • k can be thought of as an “offset”

Volatility Signatures • Measure of the calculated unconditional variance of the stock as a function of the sampling interval Δ • For T time periods, the average realized variance is: • This number is then properly annualized. • Replace RVt by BVtand other measures of intraday variance

Next Steps: • Examine Relative Contribution of Jumps of AAPL vs. those of F • Calculate correlation of the two vectors • Expected to be low. • Look at stock that are both in the same industry • Examine volatility of Apple with that of Microsoft, Google, Intel, and other technology sector firms. • Examine volatility of Ford with other car manufacturers like GM. • Examine correlation of intra-industry stocks • Expected to be high.