Download

1 / 3

30 likes | 166 Views

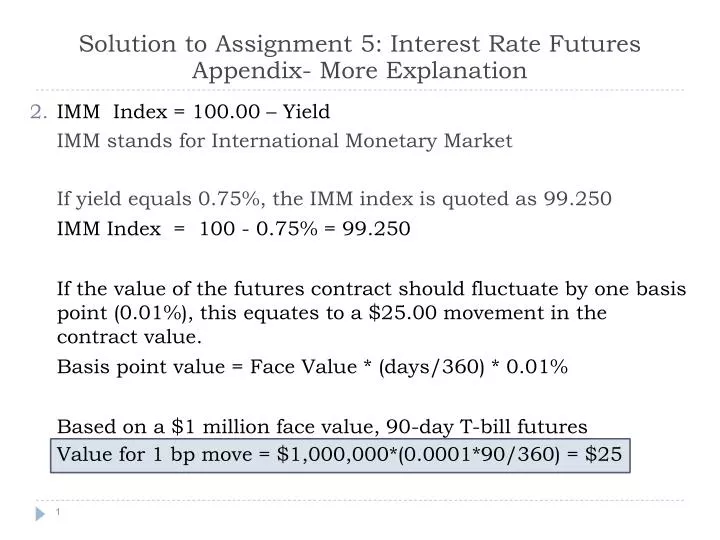

Solution to Assignment 5: Interest Rate Futures Appendix- More Explanation. IMM Index = 100.00 – Yield IMM stands for International Monetary Market If yield equals 0.75%, the IMM index is quoted as 99.250 IMM Index = 100 - 0.75% = 99.250

E N D

Solution to Assignment 5: Interest Rate Futures Appendix- More Explanation • IMM Index = 100.00 – Yield IMM stands for International Monetary Market If yield equals 0.75%, the IMM index is quoted as 99.250 IMM Index = 100 - 0.75% = 99.250 If the value of the futures contract should fluctuate by one basis point (0.01%), this equates to a $25.00 movement in the contract value. Basis point value = Face Value * (days/360) * 0.01% Based on a $1 million face value, 90-day T-bill futures Value for 1 bp move = $1,000,000*(0.0001*90/360) = $25

Solution to Assignment 5: Interest Rate Futures Appendix- More Explanation 4. Delivery Process From First Position Day until the end of the delivery month, all clearing firms are required to make daily report to CME Clearing of all open long positions in the expiring contract For all Treasury futures, First Intention Day for short position holder coincides with First Position Day for long position holders. Position Day for long position holder First Position Day: Two business days prior to the first day allowed for delivery First Intention Day: the second business day prior to the delivery month. Last Intention Day: the second business day before the last business day of the delivery month. The first business day of the expiring contract

Solution to Assignment 5: Interest Rate Futures Appendix- More Explanation 5. Invoice Amount and Profit from Delivery Calculations Converted Futures Price Invoice Price = Settlement Price * Contract scaling factor (1,000) * Conversion Factor + Accrued Interest (AI) Profit from delivery = Converted Futures Price + AI – (Cash Market Price + AI) = Converted Futures Price – Cash Market Price