Download

1 / 10

100 likes | 227 Views

Board Structure, Antitakeover Provisions, and Stockholder Wealth. Chamu Sundaramurthy, James M. Mahoney, and Joseph T. Mahoney Strategic Management (1997) BADM 546, Group #1 Meredith Blumthal Wooje Cho Barclay James Kumar Sarangee. Purpose of this Study :.

E N D

Board Structure, Antitakeover Provisions, and Stockholder Wealth Chamu Sundaramurthy, James M. Mahoney, and Joseph T. Mahoney Strategic Management (1997) BADM 546, Group #1 Meredith Blumthal Wooje Cho Barclay James Kumar Sarangee

Purpose of this Study: • This study examine the wealth effects of antitakeover provisions, viewing the influence of the market for corporate control as inter-dependent with other governance mechanisms suggested by agency theory. • Prior empirical research does not provide insight on how other governance mechanisms suggested by agency theory affect the market reactions to takeover defenses. • This paper tests the proposition that a strong board is likely to reduce the negative wealth effects associated with the adoption of antitakeover provisions UIUC BADM 546, Spring 2005

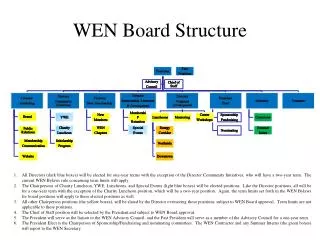

Overview What happens when the board of a firm adopts Antitakeover Provisions? Firm CEO Market Response Same individual? Board Leader Insiders Outsiders Proportions? UIUC BADM 546, Spring 2005

Hypotheses • H1: The market is likely to react less negatively to antitakeover provisions adopted by corporate boards with a greater proportion of outsiders on the board than to those adopted by corporate boards with a lower proportion of outsiders. • H2: The market is likely to react more negatively to antitakeover provisions adopted by corporate boards chaired by the CEO than to antitakeover provisions adopted by corporate boards not chaired by the CEO UIUC BADM 546, Spring 2005

Data • Sample • 261 Standard and Poor’s (S&P) 500 firms that Adopted 486 antitakeover provisions for the 1984-1988 • Antitakeover provision data were obtained from the Investor Responsibility Research Center’s (IRRC) publication • Empirical Analysis • The standardized cumulative average abnormal returns (CARs) of firms in the sample are regressed on board composition, leadership, and control variables • Methodologies based on the market model using OLS UIUC BADM 546, Spring 2005

Measures • Dependent Variable • CARs: the Cumulative Average abnormal Returns earned by shareholders accompanying the adoption of antitakeover provisions • An event window of 50 days before the proxy mailing date to 4 days following the proxy mailing date • Independent Variables • OURSIDER PERCENTAGE: the proportion of outsiders • PRE-CEO OUTSIDER PERCENTAGE: the proportion of outside members who were not appointed during the incumbent CEO’s tenure on the corporate board • SEPARATE CEO/CHAIRPERSON: 1, if the CEO and chairperson of the board are held by different individuals and 0, if they are held by the same individual UIUC BADM 546, Spring 2005

Measures • Control Variables: • INSIDE OWNERSHIP • INSTITUTINAL OWNERSHIP • MARKET VALUE OF EQUITY • EQUITY BOOK/MARKET • TAKEOVER INDICATOR • NUMBER PREVIOUSLY ADOPTED • NUMBER CURRENTLY ADOPTED • NON-POISON PILL INDICATOR • MIXED INDICATOR UIUC BADM 546, Spring 2005

Results • For H1 the results were contrary to the hypothesis: • Both measures of outsiders’ independence indicate that a greater proportion of outside board members leads to a more negative stock reaction to antitakeover provisions • For H2 the hypothesis is corroborated empirically: • The market is likely to react more negatively to antitakeover provisions adopted by boards chaired by the CEO than to antitakeover provisions adopted by board not chaired by the CEO UIUC BADM 546, Spring 2005

Results • For Control Variables • Inside ownership and institutional ownership appear to have no (linear) relationship with stock price reaction to antitakeover provisions • Large firms receive a more negative stock market response upon adoption of antitakeover provisions • Firms with larger book equity/market equity receive a more negative stock market reaction upon adoption of antitakeover provisions • The number of previously adopted and currently adopted antitakeover provisions were not statistically significant • Antitakeover amendments do not differ significantly from poison pill provisions UIUC BADM 546, Spring 2005

Discussion and Conclusions • From the result of H1 test • Contrary to agency theory predictions, the market not only does not take into account the monitoring role of outsiders but actually discounts their presence. • Outside directors are more likely to be aligned with top management than with shareholders • When board has almost no outside directors, the stock market can already suspect that the board will resist takeover offers • Actual contribution of outsiders in practice is little • Using a proportion of outsiders on the board as a measure of board vigilance is not appropriate • From the result of H2 test • The market seems to take the monitoring role of the chairperson into account in its reaction to antitakeover provisioins UIUC BADM 546, Spring 2005