Download

1 / 17

170 likes | 360 Views

MTRA 16 th Annual Conference November 14, 2006 The Banking Environment for Money Services Businesses Lisa Arquette FDIC Associate Director Anti-Money Laundering & Financial Crimes Section. U.S. Banking System. US Banking System is Large, Diverse, and Complex

E N D

MTRA 16th Annual ConferenceNovember 14, 2006The Banking Environment for Money Services BusinessesLisa Arquette FDIC Associate DirectorAnti-Money Laundering & Financial Crimes Section

U.S. Banking System US Banking System is Large, Diverse, and Complex • Four federal-level bank supervisors • Fifty state-level bank supervisors • Nearly 9,000 FDIC-insured banks • $11.5 trillion in banking assets • $4 trillion in FDIC-insured deposits • Three largest banks have $3.5 trillion in assets • Biggest bank: >$1.1 trillion in assets • Smallest bank: <$3 million in assets • 8,138 community banks with total assets <$1 billion • Median bank size about $140 million Data as of June 30, 2006

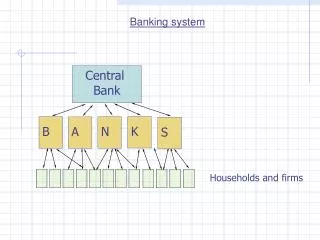

FDIC Insurer & Regulator Federal Reserve Central Bank & Regulator State Banking Supervisors Office of Thrift Supervision Thrifts Office of the Comptroller of the Currency National Banks Banks & Thrifts U.S. Bank Regulatory System

FDIC’s Primary Responsibilities An independent agency of the United States government created to provide insurance protection for depositors in banks and savings associations throughout the United States. Provides Federal deposit insurance for banks and savings associations in the United States. Supervises state-chartered nonmember banks. Acts as receiver for failed banks and thrifts and then liquidates assets.

1933 1934 1935 Today • 4,000 Banks Fail • FDIC Created in Banking Act of 1933 • FDIC Authorized to Regulate and Supervise Banks • 9 Banks Fail • Insurance: Initially - $2,500Raised to $5,000 • FDIC opens for business • FDIC pays first insured depositor • 27 banks fail • FDIC made permanent • Last bank failure was in 2004 • FDIC Insurance: $100,000 • New Deposit Insurance Legislation Enacted

Deposit Insurance 2006 Balance ~ $50 Billion

Why Coordination is Paramount The FDIC is the primary Federal regulator of over half of the institutions it insures. • FDIC supervises 5,241 state-chartered nonmember banks and state-chartered savings banks out of the total of 8,778 FDIC-insured institutions. • All Federal Banking Agencies (FBAs) provide prudential supervision for these institutions through examination and enforcement. • All FBAs also have delegated authority to examine for BSA compliance.

On-Site Exam Regional Office Follow-up On- or Off-Site Follow-up Off-Site Surveillance Risk-Focused Supervision Combination of On-Site Examinations and Off-Site Surveillance

Anti-Money Laundering Issues for Depository Institutions • FinCEN’s March 2005 Hearing • April 2005 Interagency Guidance • 2005 Revised FFIEC Manual • FDIC’s December 2005 AML Conference for Examiner Subject Matter Experts • FinCEN’s 2006 Request for Comment

Apply Customer Identification Program Confirm FinCEN Registration (if applicable) Confirm State Licensing (if applicable) Confirm Agent Status (if applicable) Conduct a Risk Assessment FFIEC BSA / AML Examination Manual Minimum Due Diligence for MSB Accounts

Lack ongoing customer relationships and require minimal or no identification by customers. Maintain limited or inconsistent recordkeeping on customers and transactions. Engage in frequent currency transactions. Are subject to varying levels of regulatory requirements and oversight. Can quickly change their product mix or location and quickly enter or exit an operation. Sometimes operate without proper registration or licensing. FFIEC BSA / AML Examination Manual Risk Factors for MSB Accounts

Identify MSB relationships. Assess the potential risks posed by the MSB relationship. Conduct adequate and ongoing due diligence. Ensure MSB relationships are appropriately considered within the bank’s suspicious activity monitoring and reporting systems. FFIEC BSA / AML Examination Manual Risk Mitigation for MSB Accounts

Types of products and services offered. Locations and markets served. Anticipated account activity. Purpose of account. FFIEC BSA / AML Examination Manual Risk Assessment factors for MSB Accounts

Banking Institutions - Lessons Learned • Not all MSBs pose a heightened risk of money laundering. • Initial Due Diligence is important – establish and document an expectation of account activity based on interviews with the MSB account holder and knowledge of the geographical area and industry norms. • Initial Due Diligence should address expectations for all account activity including ACH, wires, cross-border transactions, sweep transactions, and transactions involving secondary lines of business. • The Risk Rating assigned should be based on the initial due diligence and subsequent/ongoing account reviews. • Ongoing Due Diligence – Periodically review account activity to ensure that the initial expectation of account activity remains valid.

Banking Institutions - Lessons Learned (continued) • The nature and volume of cash, check, wire, and ACH activities should be consistent with the expectation established during the initial due diligence. • High-risk indicators for MSBs should be pre-established as part of the banking institution's AML Policies. • New accounts should generally receive more frequent reviews than “seasoned” accounts that have not presented any previous concerns. • If the activity is not consistent with the initial expectation, the account holder should be contacted to provide is a reasonable explanation. • Enhanced Due Diligence - MSBs that exhibit high-risk characteristics such as unexplained or unusual account activity require increased monitoring and scrutiny.

CONCLUSIONS • Banks should not treat all MSB accounts as having the same degree of risk. • Obtaining and documenting a thorough initial expectation of account activity is extremely important. • Neither FinCEN nor the Federal Banking Agencies expect, banking institutions to serve as the de facto regulator of the MSB industry. • Banks that open or maintain accounts for MSBs should apply the requirements of the BSA on a risk-assessed basis, as they do for all customers, taking into account the products and services offered and the individual circumstances. • The decision to accept or maintain an account with an MSB customer rests with the institution’s management and should be based on the institution’s capacity to identify, monitor, and manage the associated risks.