Download

1 / 35

350 likes | 454 Views

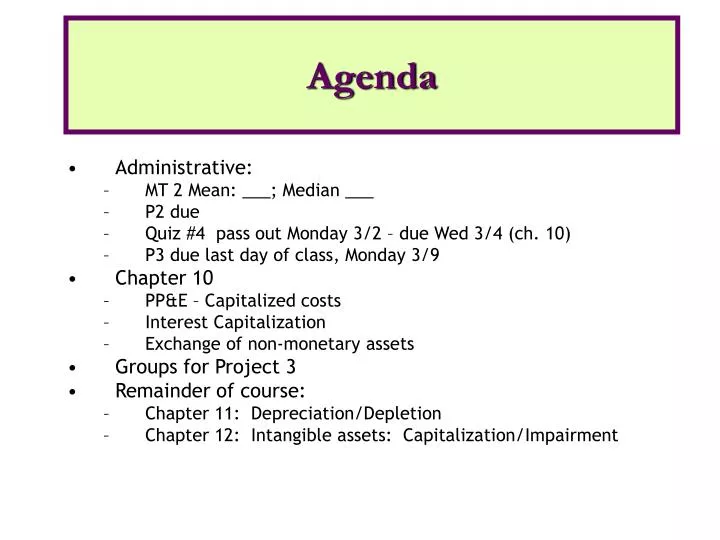

Agenda. Administrative: MT 2 Mean: ___; Median ___ P2 due Quiz #4 pass out Monday 3/2 – due Wed 3/4 (ch. 10) P3 due last day of class, Monday 3/9 Chapter 10 PP&E – Capitalized costs Interest Capitalization Exchange of non-monetary assets Groups for Project 3 Remainder of course:

E N D

Agenda • Administrative: • MT 2 Mean: ___; Median ___ • P2 due • Quiz #4 pass out Monday 3/2 – due Wed 3/4 (ch. 10) • P3 due last day of class, Monday 3/9 • Chapter 10 • PP&E – Capitalized costs • Interest Capitalization • Exchange of non-monetary assets • Groups for Project 3 • Remainder of course: • Chapter 11: Depreciation/Depletion • Chapter 12: Intangible assets: Capitalization/Impairment

Property, Plant & Equipment: Valuation PP&E is initially valued at historical cost: • the asset’s cash or cash equivalent price, and • the cost of readying the asset for use • E.g., freight-in, insurance for trip, installation and testing • US GAAP vs. IFRS • US GAAP uses a cost model (PP&E is carried at cost less any accumulated depreciation and accumulated impairment losses) • IFRS allows PP&E to be reported using either a cost model – OR- a revaluation model (PP&E is reported at fair value at the date of revaluation)

Cost of Land Land costs include: • purchase price • closing costs, attorney fees, and recording fees • costs of getting land ready for use (clearing, etc.) • this includes the cost of buildings on the land and their removal, if they are demolished and removed • special assessments for local improvements • assumption of liens or encumbrances, and • additional improvements with an indefinite life Sale of salvaged materials reduces cost

Land Improvements, Building and Equipment Land improvements: • Improvements with limited lives are recorded as Land Improvements (and not as Land) Building cost includes: • costs of materials and labor, and overhead • professional fees and building permits Equipment cost includes: • purchase price • freight and handling charges • costs of special foundation, installation, and initial testing.

Self-Constructed Assets These are assets constructed by the business for use in operations. The cost of self-constructed assets includes: • cost of direct materials, • cost of direct labor, • variable manufacturing overhead, • a pro rata portion of the fixed overhead, and • interest costs incurred during construction (subject to rules).

Interest Capitalization: Factors Three tasks: • Determine qualifying assets • Determine capitalization period • Determineamount of interest to be capitalized

Interest Capitalization To be a Qualifying Asset, must: • Self construct the asset (have the economic burden while under construction) • The asset must be something that will be used in the business to generate revenue • Two types of qualifying assets: • Assets under construction for use in operations (ex. Factory that will generate products) • Discrete assets intended for sale or lease (ex. Developer developing property)

Interest Capitalization: Capitalization Period Capitalization period begins when: • expenditures for the asset have been made, and • activities for readying the asset are in progress, and • interest costs are being incurred Capitalization period ends when: • The asset is substantially complete and ready for its intended use.

Interest Capitalization: Amount to be Capitalized Capitalize the lesser of: • actual interest costs • avoidable interest Avoidable interest is the amount that could have been avoided if expenditures for the asset had not been made • Note that after being capitalized, capitalized interest is treated just as any other component in the cost of the constructed asset (so if construction goes over a year/end, capitalized interest from the prior year is included in the Weighted Average Accumulated Expenditures (WAAE) for the next year)

Interest Capitalization: Amount to be Capitalized Computing Avoidable Interest (the approximation of interest that could have been avoided if the expenditures had been used to repay debt instead of being used for construction): • Determine weighted-average accumulated expenditures (WAAE) • Accumulated expenditures for the project weighted based on when the expenditures were made during the year • Multiply by appropriate interest rate(s). These are, in the following order: • Interest rate for debt specifically incurred for construction of the project • Weighted average interest from all other borrowing, regardless of the use of funds (because expenditures above construction loan could have been used to repay general company debt) • The result is the “avoidable interest” ( the approximation of interest that could have been avoided if the expenditures had been used to repay debt instead of being used for construction) • Capitalize the lesser of avoidable or actual interest

1 2 Determine weighted-average accumulated expenditures Appropriate interest rate(s) Multiply by Avoidable interest Capitalize, lesser of avoidable and actual interest Computing Avoidable Interest: Steps

Determining Weighted-Average Accumulated Expenditures (WAAE): Example Amber makes the following two payments in 2004: Jan 31: $24,000 July 31: $18,000 Capitalization period ran from Jan 31 – Dec 31. What is the WAAE? Jan 31: $24,000 * (11/12) $22,000 July 31: $18,000 * (5/12) $ 7,500 WAAE $29,500

Determining the Appropriate Interest Rate: Example Amber had the following debt outstanding throughout 2004: 10%, 2-year note specifically for the project: $25,000 8%, 5-year note (other debt): $20,000 What is the appropriate interest rate(s) and the avoidable interest?

Up to specific loan, $25,000 at 10% $2,500 avoidable 2 1 Weighted- average accumulated expenditures: $29,500 + Excess WAAE ($29,500 less $25,000 = $4,500) at 8% $360 avoidable 3 $2,860 The Appropriate Interest Rate and Avoidable Interest: Example

Comparing Actual and Avoidable Interest: Example Avoidable interest: $2,860 Actual interest: • $25,000 @ 10% = $2,500 • $20,000 @ 8%= 1,6004,100 • Capitalize avoidable interest of $2,860 (the lesser of avoidable and actual interest). • Expense $1,240 ($4,100 less $2,860).

Up to specific loan, $2,000,000 at 12% $240,000 avoidable 2 1 Weighted- average accumulated expenditures: $3,600,000 + Excess WAAE ($3.6m less $2m = $1.6m) at 10.42% $166,667 avoidable 3 $406,667 E 10-7

Up to Specific construction Loan $ X loan% $ avoidable 2 1 Weighted- average accumulated expenditures (WAAE) + Excess WAAE ($) at Weighted ave% of Other Debt $ avoidable 3 $ Total Avoidable Capitalization of Interest

Up to Specific construction Loan $0 $0 avoidable 2 1 Weighted- average accumulated expenditures: $1,500,000 + Excess WAAE ($1.5m) at 13% $195,000 avoidable 3 $195,000 P 10-7

US GAAP vs. IFRS • IFRS: companies have choice whether or not to capitalize interest. Companies must consistently apply method to qualifying assets. • By 2009, IFRS will require capitalization

Miscellaneous Valuation Issues • Assets, purchased through long term credit, are recorded at the present value of the consideration exchanged. • Cost of assets, acquired in a basket purchase, is allocated to assets on the basis of their relative fair market values. • If assets are acquired in exchange for stock then the market valuation of the stock is the basis for valuation. • More generally, we first look to the fair value of what is given up to determine the value of the asset received

Exchange of Non-Monetary Assets The basic rule is that the exchange must be based on: • The fair value of the asset given up, or • The fair value of the asset received whichever is clearly more evident. • This applies to monetary and non-monetary exchanges (when cash is given up, the Fair Value of what is given up is obvious) For non-monetary exchanges: • We recognize gains and losses when the transaction has “commercial substance.” • When the transaction has NO “commercial substance,” we recognize losses. Gains are either NOT recognized or are only partially recognized.

What is Commercial Substance? Ask: • Have future cash flows changed as a result of the exchange? Does asset received have different timing of future cash flows than the asset gave up? If yes, the exchange has commercial substance • Ex: Exchange truck with 5-year useful life for land. Look at cash flow generated from the truck during the 5 years; look at cashflow coming in over land’s indefinite life • If the firms economic position has not changed, then the exchange does not have commercial substance • Ex: exchange two items with the same NPV and the timing of future cashflows is the same • So an exchange can have commercial substance even if the assets exchanged are similar (e.g., a truck exchanged for a truck with a longer life or more usefulness)

Commercial Substance Example: on December 31, 2005, Max exchanges a check-signing machine with Oly. The book value of the machine Max gives up is $5,000 (original cost of $20,000 and AD of $15,000), and its fair value is $10,000. The machine received by Max has a fair value of $10,000 (and was carried on Oly’s books at $7,000). The machines have the same remaining useful life and perform the same functions. Does this have commercial substance? No – ask: why would these companies undertake the exchange? They are in the same position after the exchange in all respects. Thus, it appears that the only reason for the exchange was to attempt to recognize a gain. If: one machine had more versatility, or a longer life, etc, then there could be economic substance to the exchange.

What’s The Journal Entry? Assuming No Commercial Substance: Dr. AD – old machine 15,000 Dr. New Machine 5,000 Cr. Old Machine 20,000 (Here the gain not recognized, $5,000, is taken out of the Fair Value of the new machine) If there was commercial substance: Dr. AD – old Machine 15,000 Dr. New Machine 10,000 Cr. Old Machine 20,000 Cr. Gain 5,000

Boot • “Boot” refers to a small amount of cash added to the exchange to “kick” it along. • A transaction can be deemed not to have commercial substance even if a small amount of cash is involved • For smaller cash amounts (where cash is received) where there is no commercial substance, a gain is partially recognized: Cash Received x Total Gain = Recognized Gain Cash Received + FV of Other Assets Received

Example with “boot” Example: on December 31, 2005, ABoy exchanges a machine with Ace. The book value of the machine ABoy gives up is $58,000 (original cost of $110,000 and AD of $52,000), and its fair value is $75,000. The machine received by ABoy has a fair value of $60,000 (and was carried on Ace’s books at $51,000). Ace also paid ABoy $15,000 in cash as part of the exchange. • Record exchange in ABoy’s books assuming the transaction has commercial substance. • Record exchange in ABoy’s books assuming the transaction lacks commercial substance (the machines have the same remaining useful life and perform the same functions)

Journal Entries • Assuming commercial substance: Dr. Cash 15,000 Dr. AD – old machine 52,000 Dr. New Machine (@ FMV) 60,000 Cr. Old Machine 110,000 Cr. Gain 17,000 2. Assuming NO commercial substance: Dr. Cash 15,000 Dr. AD – old machine 52,000 Dr. New Machine (FMV – def’d gain) 46,400 Cr. Old Machine 110,000 Cr. Gain 3,400 Total Gain: FV asset given up – BV asset given up (75,000) – (110,000 – 52,000) = 17,000 Partial Gain to Recognize: (boot)/(boot + FV asset received) 15,000 / (15,000 + 60,000) = 20% x 17,000 = 3400 New Machine Carrying Value: ( FMV – deferred gain [Gain – recognized gain]) [60,000 – (17,000 – 3400)]

Accounting for Exchanges Types of Accounting Exchange Guidance Has Commercial Recognize gain Substance and losses Lacks Commercial No Gain Substance No Commercial No Gain Subst. w/cash pd. No Comm. Subst. Partial Gain w/ cash received Note: a loss is always recognized

Accounting for Exchanges • Compute the total gain or loss on the transaction. This amount is equal to the difference between the fair value of the asset given up and the book value of the asset given up. • If a loss is computed in step 1, always recognize the entire loss. • If a gain is computed in step 1: • And the exchange has commercial substance, recognize the entire gain. • And the exchange lacks commercial substance, • And no cash is involved, no gain is recognized • And some cash is given, no gain is recognized • And some cash is received, the following portion of the gain is recognized: Total gain X Cash received (boot) / (Boot) + FV of assets received)

Dispositions of PP&E Plant assets may be: • retired voluntarily, or • disposed of by sale, exchange, involuntary conversion Depreciation is recorded up to the date of disposal before determining gain or loss • Note: Follow the policy of the firm consistently Gains or losses from involuntary conversion are often reported as extraordinary items.

Disposition Example On July 1, 2005, Vincent Inc. sells an executive back-scratching machine for $10,000 that was bought on 1/1/01 for $50,000. Vincent Inc. recorded depreciation on the machine for 4 years (through 12/31/04) at the rate of $10,000 per year. Show the journal entry for the disposal of the old machine.

Journal Entry Dr. Depreciation Expense 5,000 Cr. Accum. Deprec. 5,000 (10,000/yr X 6/12 mo.’s) Dr. AD – Machine 45,000 Dr. Cash 10,000 Cr. Gain on disposal (plug) 5,000 Cr. Machine 50,000

Costs Subsequent to Acquisition • If cost incurred increase future benefits, capitalize costs. • If costs maintain a given level of services, expense costs. Costs incurred after acquisition can be classified as: • Additions (capitalize) • Improvements and replacements (capitalize) • Rearrangements and reinstallation (capitalize if service potential increased) • Repairs (expense – if ordinary)

They increase future service potential Improvements Replacements or Substitution of a better asset for present asset Substitution of a similar asset for present asset Improvements and Replacements Capitalize costs, if In terms of accounting, these are treated exactly the same