Download

1 / 15

150 likes | 193 Views

Learn about OECD's guidelines for governance of state-owned enterprises, covering legal framework, ownership policies, transparency, stakeholder management, and the role of boards. Discover the importance of implementing these guidelines for improved corporate governance and value creation.

E N D

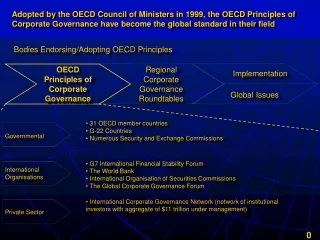

OECD Guidelines on Corporate Governance of State Owned Enterprises Lars Johan Cederlund Senior advisor Ministry of Industry, Employment and Communications, Sweden Chairman OECD Working Group on Privatisation and Corporate Governance of State Owned Assets

The Guidelines and the role of SOEs • Direct application in commercial SOEs • Focus on federal or state-owned SOEs • Comparative report gives information • Comparative report allows benchmarking

Why Guidelines? • Need for an integrated Corporate Governance model, best practice collection • Contribution to growth from professional governance of SOE:s • Better balance between privatisation and governance was asked for by politicians

SOE employees as percentage of total employment in OECD countries

Turnover/GDP and value added/GDP for SOEs in OECD countries (percent)

New Corporate Governance model • Complement to the OECD Principles of Corporate Governance which are developed for privately-owned companies • Non-binding guidelines, agreed by member states for their proper activities, best practice • The Guidelines is an integrated product, with individual Guidelines linked/connected to the others • Do not preclude/alter Privatisation policies

Priorities • Level-playing field with the private sector • Reinforcing the ownership function • No mixing of political and business decisions • Improving transparency • Empowering SOE boards

Chapter I, Legal and regulatory framework • Separate regulation and shareholding • Transparency on special obligations • Level-playing field in markets • Competitive conditions in access to finance

Chapter II The state as an Owner • Clear and disclosed ownership policy • No direct interference in day-to-day activities • Let boards carry out their responsibilities • Centralisation/coordination of the ownership function • Accountability secured • Effective exercise of ownership rights

Chapter III Other Shareholders • All shareholders should be treated equitably • High degree of transparency towards all shareholders • Facilitate participations in AGM for minority shareholders

Chapter IV Stakeholders • Rely on OECD Principles of Corporate Governance • Report on stakeholder relations • Develop, implement and communicate compliance with codes of ethics

Chapter V Transparency Basis for much of the other Guidelines • Disclosure at ownership level and at company level • Internal audit • Independent external audit • High quality standards for accounting and audit • Disclosure as listed companies • Disclosure of material information, including objectives, ownership and voting rights, financial assistance from the state transactions with related entities and risk factors

Chapter VI Boards Critical governance organ • Full responsibility • Able to appoint CEO • Act in the best interest of the company • Independent judgement • Good corporate governance standards • Systematic evaluation

Possible effects of the Guidelines • Basis for structured reform • Facilitate benchmarking • Awareness of important values on the state’s balance sheet • Better value-creation due to more effective corporate governance