Download

1 / 11

110 likes | 511 Views

Cashless Transactions. Platforms, Challenges and Opportunities. The Story. A paper presented at the annual Conference of The Computer Professionals Registration Council of Nigeria. Segun Akano CEO, Upperlink Limited. How We Got Here….

E N D

Cashless Transactions Platforms, Challenges and Opportunities The Story A paper presented at the annual Conference of The Computer Professionals Registration Council of Nigeria Segun Akano CEO, Upperlink Limited

How We Got Here… • CBN introduced a cashless policy which is to enhance the Nigerian Payment system, reduce the use of cash in payments for goods/services and improve the use of Electronic Payment Systems. • The specific advantages are to reduce the heavy burden of Cost of Cash Management, Security of money and people, Money Laundering, Transaction Losses due to Fraud and Counterfeit among others • The policy attempts to place a tab on a daily cumulative cash lodgments & withdrawal from banks of N150,000 & N1m for individuals &corporate customers respectively . • CBN recently reviewed upward the limit for free cash transactions for individuals to N500,000 from N150,000 and for corporate bodies to N3 million from N1 million • The policy took off in Lagos on April, 1, 2012 and is expected to begin nationwide in Jan 2013. • Since its implementation, many issues have arisen and there have been efforts made to respond to them

The Journey So far… • Presently there are between 18 to 20 million different types of cards in the hands of Nigerians. • There are over 60,000 POS in use across Nigeria presently. CBN plans to deploy 350,000 by 2015 of which 90,000 will be done in 2012 alone. • POS Transaction grew from N100m in May 2011, it has now reached N2.34bn in May 2012 with over 7000 transactions done daily (about N78m per day) • POS transactions are expected to grow by 200% in the next year [Interswitch} • Of the over 11,000 ATMS deployed nationwide, transactions have hit 110m monthly up from 100m recorded as at last year July. • CBN has however encouraged the banks to deploy additional 75,000 ATMs to beef up capacity.

Cashless (Cashlite) Regime: What is involved? Specific economic activities covered within the context of the cashless initiative include: -Paying for services -Buying items -Subscribing for services -Collecting from one or more payer -Aggregating deductible funds.

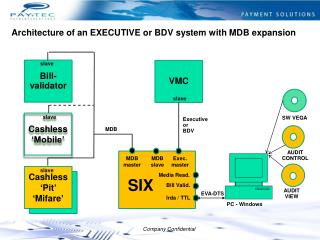

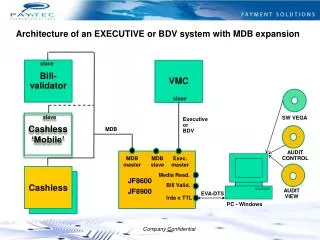

Cashless (Cashlite) Regime: Platforms There are about 6 Principal Platforms viz: -Point of Sale Terminal [POS] -Automated Teller Machines [ATM] -Web Gateways [Paydirect/Webpay] -Mobile [M-Money] -NIPS [NIBSS Instant Payment System] -Account-to-Account Transfer [NEFT, RTGS]

Cashless (Cashlite) Regime: Stakeholders • Cashless Transactions Stakeholders include but not limited to: • 1. Merchant Acquirers [Banks] • 2. Card Issuers [Banks] • 3. Merchants [Stores, Schools, Hospitals, Churches] • 4. Cardholders [Individuals] • 5. Card Schemes and Card Associations [Loyalty Schemes,] • 6. Switches [Interswitch, Chams, Etranzact] • 7. POS Terminal Owners • 8. Payments Terminal Service Aggregator (PTSA) [ITEX] • 9. Payments Terminal Service Providers (PTSP) [Paymaster, Etop, Citiserve, Valucard, EasyFuel and ITEX] • 10. Processors [NIBSS] • 11. Independent System Operators (ISO) [Systemspec, Parkway, Upperlink]

Cashless (Cashlite) Regime: Enablers Enablers are firms who on the face-value capabilities of the Cashless PLATFORMS build several solutions for organizations to manage outflow and inflow of Money through these gateways. Specific examples are: -Payment Suites [eg. PayChoice, Remita] -Collection Suites [BranchCollect, Remita, PayChoice, BankCollect] -Payroll Application -E-Commerce Solutions -E-Wallet Products -

Cashless (Cashlite) Regime: Challenges Some are rather best described as ‘Teething Problems,’ Others are systemic and require conscientious consideration: Poor communications network Limited POS deployed Interoperability of Cards on the platforms Poor response time to customer complaints User apathy Vulnerability to fraud Insufficient sensitization

Cashless (Cashlite) Regime: The Gaps In the face of all these Nigeria still lags behind many nations in the use of ATMs and PoS terminals. ATM per individual is very low in Nigeria and calls for immediate actions as shown: 80 % of the cash in Nigeria’s economy is still locked up in the hands of the economic participants in the informal sector.

Cashless (Cashlite) Regime: Opportunities It is estimated that cashless transactions in Nigeria is expected to grow at an annual rate of 85% in the next 5 years. Forecast has it that overall transaction processing for banks and other financial services would surpass $15bn (N2.4trn) by the end of 2012. Many more levels are expected to be created in the E- Business Value Chain that will open up our economy. It is hoped that, if the immediate challenges are adressed, the objectives of CBN would have been met on the one hand and Nigeria will be on her way to be among the top 20 economies in the world by 2020 as envisioned by the present political administration.