Download

1 / 35

390 likes | 783 Views

Captive Insurance. CAGNY June 1, 2005 New York City. Derick A. White, CPA, CFE Director of Captive Insurance Vermont Department of Banking, Insurance, Securities and Health Care Administration. What is a Captive?. “formalized self-insurance” wholly owned subsidiary

E N D

Captive Insurance CAGNY June 1, 2005 New York City Derick A. White, CPA, CFE Director of Captive Insurance Vermont Department of Banking, Insurance, Securities and Health Care Administration

What is a Captive? • “formalized self-insurance” • wholly owned subsidiary • licensed in a state (or country) • a regulated insurance company with a limited license

Why form a Captive? • Obtain Coverage • Control Cost • Focus on Risk Management • Manuscript Policy • Pre-loss funding

History • Bermuda during the early 1970’s • Colorado, Georgia, Tennessee • Vermont in 1981 • Hawaii in 1986 • Recent States

Types of Captives • Pure • Industrial Insured • Association • Risk Retention Groups • Sponsored (Rent-A-Captives) • Reciprocal • Branch

General Liability Product Liability Workers Comp Auto Liability Auto Physical Damage Property Business Interruption Marine & Cargo Terrorism Environmental Impairment Credit Professional Liability Political/War Risk Aviation Strike Employee Benefits D&O Some Coverages Currently Written with Captives

Medical Malpractice Terrorism Redomestication Trends

Vermont’s Captive Industry Profile • numbers (over 700 licensed companies) • management firms (14 active) • service providers (CPA’s, banks, actuaries) • Vermont Captive Insurance Association

Role of the Actuary • Feasibility Study • Annual Opinion • Financial Projections • Actuarial Review of applications • Examinations

Current Events • Title/mortgage insurance • Risk transfer • GAO-risk retention groups • NAIC accreditation

Captive Insurance CompaniesWilliam D. MotherwayExecutive Vice President Tishman Realty & Construction Co., Inc.

A Brief History Historical Review • Most early captives were wholly-owned ‘50s. • By 1960 there were approx.. 100 captives in operation including some groups • 80’s-90’s – Rent-A-captives and Cells Critical factors for development of the industry • Availability of coverage problems • Pricing inequity - swings from soft to hard markets leaving good risks with “Hats in Hand” • Lack of flexibility with insurance coverage and wording • Regulatory Responsiveness by Domiciles • Changing Owner Needs

Current Trends & Key Opportunities • Property Programs Getting Fresh Look • Return to Deductible & Retention Captives • Hard Reinsurance Market – Lack of Support & Underwriting • Contractors • Nursing Homes • Medical Malpractice • D&O • Property • Many Others • Terrorism Risk Insurance Act of 2002 • Group Program Proliferation in Stressed Classes of Business

Controls and Flexibility “Reasons for a Captive: • Internalize insurance program underwriting profits • Unbundle insurance services, reduce insurance costs • Access to the reinsurance markets • Enhance premium funds, cash flow and investment income • Leverage markets, greater control, enhance strategic partnerships • Policy design flexibility, specific to insured’s risk profile

The Stage is Set All forms of Captives are subject common attributes: • Financial • Regulatory • Control • Flexibility

What is a Captive and Who Uses them? Single-Owner (Pure) Captives - insure only the risks of the owner or the owner’s subsidiary operations (Exception - controlled unaffiliated business) • Companies with predictable attritional losses (high frequency. low severity) • Companies with better than market average loss experience • Companies with poor loss experience but committed to improved risk management • Companies with uninsured risks • Companies that wish to consolidate global programs • Companies able to sell insurance products to their customers

Key Financial Considerations • Risk retained within the “economic” family • Program loss sensitivity • Additional fixed costs of captive operations • Investment and liquidity • Capital commitment (Cash , LOC’s, other) • Tax deductibility (paid losses vs. loss reserves) • Income and Local Taxes • Each Structure discussed contains some or all of these

Typical Design Structures • Direct Writing Captive • Retain all Risk or Cede Risk to a Reinsurance Partner • Reinsuring / Assuming Captive • Assumes risk from a fronting carrier or another ART vehicle • Retains or retro-cedes to a reinsurance carrier

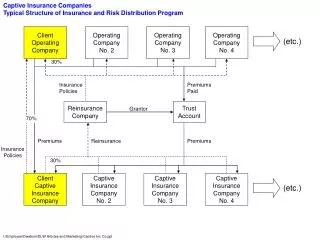

Captive - Operating as a Direct Writer Insured Shareholder Dividends Insurance Premiums Capitalization Captive Insurance Company (Owned by Insured) Claim Settlements Claimants

Captive - Operating as a Reinsurer Insured Insurance Premiums Capitalization Shareholder Dividends Policy Issuing Company Claimants Claim Settlements Security to Guarantee Reimbursement of Losses Reimbursement of Losses Premium Less Fronting Fee & Excess Insurance Captive Insurance Company (Owned by Insured)

An RRG is an insurance entity owned and controlled by two or more non-affiliated organizations insured by the RRG. Homogeneous and insure similar types of businesses risks or Heterogeneous and insure risks of several types of organizations. RRGs in the United States are licensed to issue policies and and operate under the Federal Risk Retention Act of 1986. They are stock, reciprocal or mutual in organizational form. Risk Retention Group

An Association Captive is an insurance company owned and controlled by two or more non-affiliated association insured by the captive. Homogeneous and insure similar types of businesses risks or Heterogeneous and insure risks of several types of organizations. Association Captives in the United States are licensed by a domiciliary state (VT for example) and use a fronting carrier. They are stock, reciprocal or mutual in organizational form. Association Captive

Ownership • Are insureds owners of the entity? In what way and how much? • Joint and Several liability? • Assessable policy? • Withdrawals? • Other?

Management and Governance • Board of Directors • Officers • Shareholders • Professional Managers • Investments Regulatory and Tax Issues • State insurance regulation • Possible use of a fronting carrier • Liability Risk Retention Act of 1986 • Financial responsibility laws • Tax treatment of group captives • Dividend distribution

Service Providers • Front carrier (if applicable) • Reinsurance (specific and aggregate) • Management • Underwriting • Claims and Loss Adjustment • Actuarial • Banking • Investment Management • Auditors • Legal Counsel

Benefits • Better member service • Lack of coverage and capacity fears eased • Price no longer total market driven • Long term relationship with knowledgeable partners • Protection against competition • Protection against market instability • Profit driven

Captive Forms - Rent-a-captive/ PCC • A non-owned facility • Clients do not contribute capital but instead rent it from the rent-a-captive sponsor • Usually located off shore, e.g. Bermuda, Barbados, Guernsey or Cayman • PCC law offers protection to rent-a-captive participants • Affordable and quick option for most smaller companies • Company selection criteria - cost of risk greater than $1m and net worth greater than $25m

TRIMCO Insurance Company Overview Parent Company - Tishman Realty & Construction Co., Inc. Industry: • Construction • Hotels and Realty • Real Estate

TRIMCO Insurance Company Overview Details of Vermont Captive • Licensed - December 2001 • Operational - January 1, 2002 Program Structure: • Direct Deductible Reimbursement - (Premium = $5.0M ) • Workers Compensation • General Liability • No Loss Portfolio Transfer

TRIMCO Insurance Company Overview Key Operational Components • Start-up costs $25k • Operational/Administrative Costs - $90k annually The Future • Program Changes