Download

1 / 21

210 likes | 335 Views

Asymmetric Information and Bubbles: An Experiment. Michael Brandner Jürgen Huber Michael Kirchler Matthias Sutter all University of Innsbruck. Outline. Introduction Model description Experimental implementation Hypotheses Results and interpretation Concluding remarks. Introduction.

E N D

Asymmetric Information and Bubbles: An Experiment Michael Brandner Jürgen Huber Michael Kirchler Matthias Sutter all University of Innsbruck

Outline • Introduction • Model description • Experimental implementation • Hypotheses • Results and interpretation • Concluding remarks

Introduction • Starting point is the well-known basic setup of Smith, Suchanek and Williams (1988) – subsequently SSW • Outstanding characteristic: declining fundamental value in the course of a market • Typically, bubbles can be observed in this setting • Related literature, revealing determinants for bubble reduction: • Less frequent dividend payments (Smith et al. 2000) • Constant fundamental value (Noussair et al. 2001) • Detailed instructions (Lei et al. 2001) • Futures markets (Noussair and Tucker 2004) • Experience (Dufwenberg et al. 2005) • Short selling (Haruvy and Noussair 2006)

Model description • Basic features: • Assets of a virtual enterprise are traded - after every trading period the stock pays a dividend amounting to either zero or 20 MU (given equal probability) • All traders know the dividend generating process, but nobody exhibits information about the actual dividend realizations before a period’s termination • No “buy-out” option is introduced so that assets are worthless after a round’s termination (one round being 10 successive periods), implying declining fundamental values

Model description • We test for the impact of different information structures on bubble formation – public information and asymmetric information • Reference treatment (T1): symmetric (non-) information about future dividends (comparable e.g. to SSW (1988), Dufwenberg et. al (2005)) – all traders are of type I0 (just knowing the dividend generating process) • Public information (T2): each trader is informed about the dividend realization of the current period from the outset – all traders are type I1 • Asymmetric information (T3): on average, traders also know one future dividend, but this information is asymmetrically distributed – two traders are of type I0, two of I1, and two are allocated to type I2 (so-called insiders, knowing the current and next period’s dividend realizations)

Experimental implementation • One market is populated by six traders - distribution of information levels in the three treatments: • We replicate three rounds in a market – one round consisting of 10 periods (lasting for 120 seconds each) • Initial endowments: 3,000 MU and 10 assets/1,000 MU and 30 assets (expected final profit is equal) • Money and asset holdings are carried over from period to period, but reset to the respective starting levels after a round’s termination (no “buy-out” option, assets‘ life-span is ten periods)

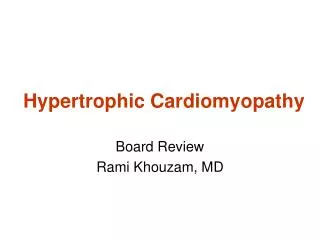

Experimental implementation • The market is a continuous double auction with open order book, implemented with z-Tree (Fischbacher, 2007) • Subjects can trade any quantity of assets, given the limitations of their asset inventory and cash endowment (neither loans are provided nor is short selling allowed) • We conduct six markets per treatment for a total of 18 markets (at the University of Innsbruck) • Participants have been business students with no previous experience in similar experiments

Trading screen Information about future dividend(s)

Hypotheses • H1: Public information (T2) about current period‘s dividend decreases bubble-size (compared to T1) • H2: Asymmetric information (T3) about future dividends decreases bubble-size (compared to T1) • H3: Informed traders will use the fundamental information provided so that prices increase when they see high dividends and fall when they see low dividends • H4: Subjects in T3 have an increased incentive to trade across information levels

Results Average price departures: T1: 40.6 MU T2: 25.3 MU T3: 18.4 MU

Results – impact on bubble-size • Comparing bubbles (overvaluation = trading price minus corresponding fundamental value) in the three treatments pairwise (two-sided Mann-Whitney U-tests): H1 and H2 cannot be rejected: bubbles are significantly smaller in markets with knowledge about the current dividend (T2– public information), and smaller again when dividend information is asymmetrically distributed (T3)

Explaining bubble-size reduction in T2 and T3 • H3: Informed traders will use the fundamental information provided so that prices increase when they see high dividends and fall when they see low dividends • We examine the relationship between known positive/negative dividend realizations and the extent of overvaluation (trading price minus the corresponding fundamental value) – correlation implies prices closer to fundamentals • H3 cannot be rejected: informed trader obviously concentrate more on the fundamentals of the stock (than on the hope for capital gains) with the consequence that prices track fundamentals closer

Trade activities within and across information levels in T3 • H4: Subjects in T3 have an increased incentive to trade across information levels • If subjects in T3 do indeed base their trading decision on their given dividend information, traders within any given information level should be rather homogeneous in their trading decisions • The following matrix reveals pro-rata transactions, measured by the total amount of accomplished trades in T3 (n=1334)

Trade activities within and across information levels in T3 • Trading frequency is significantly lower between information levels than across • A possible explanation is that traders within each information level form similar beliefs based on the information they get and trade on these beliefs • H4 cannot be rejected: additional support that traders in T3 increasingly focus on fundamentals (thus implying that prices track fundamentals closer)

Concluding remarks • Both changes to the standard setup – public and asymmetric information – reduce bubbles significantly (more pronounced effect in the latter treatment) • Informed subjects in T2 and T3 base trading decisions on the information they receive, thus prices track fundamentals closer, making speculation less likely to occur • Implication: Real financial markets are undoubtedly characterized by mixed-experienced traders (recall Dufwenberg et. al (2005)) with asymmetric information about future cash flows, so that it should not be surprising that bubbles are indeed rare. The spectacular ones are less than five in a century (e.g. 1929, 1987 and the late 1990ies)!

![Asymmetric Tandem Epoxidation – [4+3] Cycloaddition of Allenamides](https://cdn1.slideserve.com/1702350/asymmetric-tandem-epoxidation-4-3-cycloaddition-of-allenamides-dt.jpg)