Download

1 / 11

110 likes | 252 Views

Risk Pricing Linkages between Financial and Insurance Markets. John Daniel Pollner, World Bank Presented at World Bank conference on “Financing the Risks of Natural Disasters,” Washington, DC, June 2-3 2003. Volatility, Variance & Risk.

E N D

Risk Pricing Linkages between Financial and Insurance Markets John Daniel Pollner, World Bank Presented at World Bank conference on “Financing the Risks of Natural Disasters,” Washington, DC, June 2-3 2003

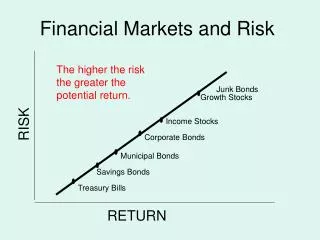

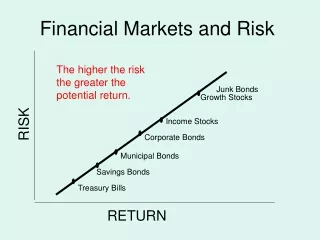

Volatility, Variance & Risk • Risk in Securities is measured as volatility in terms of variance or standard deviation of the price: σ

Variance and Pricing High Variance in a Price Series adds a Premium To the Expected Value

σ (sigma) reflects uncertainty • For financial markets, the sigma of a security therefore, reflects its riskiness and thus price

Bond Market Risk Another Measure of Risk is the probability of default based on a historical record of experience • Risk = Default Probability, p(D) • Bond yield = risk free rate (eg. 5%) + p(D) (eg. 4% or spread over risk free rate) = 5% + 4% = 9% bond yield

Pricing Natural Disaster Risk • Using probability: • Example: annual probability of a Class 4 Hurricane: • p (Class 4) = 1%

Uncertainty of the Probability • Since Natural Disasters are rare, the sigma (σ) of the statistical distribution is much higher. • Therefore the uncertainty premium will also be high. • If the probability was 1%, the sigma might be as high as 3% around the 1% probability mean.

Pricing a Catastrophe Bond • A bond based on a catastrophe event would thus be priced: • Prob. = 1% + sigma = 3% • Plus risk free rate = 5% • = Bond rate = 9% • 9% earned if no disaster. • Bond principal goes to holder if a disaster occurs (default)

Insurance & Reinsurance Pricing • Criteria 1: ROE (20%) • Criteria 2: actuarial pricing + admin. costs + brokerage costs + reinsurance costs + profit margin = p(D) + σ + A + B + R + P • Criteria 3: XL Layer: p(D) + σ + profit

Structures for Government Risk Loss Coverage Structure • Cat bond for creditworthy governments, reinsurance for others using parametric triggers • Credit can reduce cost Contingent Credit Layer Reinsurance Layer or Catastrophe Bond Layer Retention Layer $ Loss

Credit As a Form of Insurance? • Credit: P + I annuitized, e.g.: 20% • Reinsurance: 4% prem • Probability: 1% • E(C) = 1% x (20%) + 99%(0) = 0.2% < 4% • Even adding sigma factor, l.t. cost still less