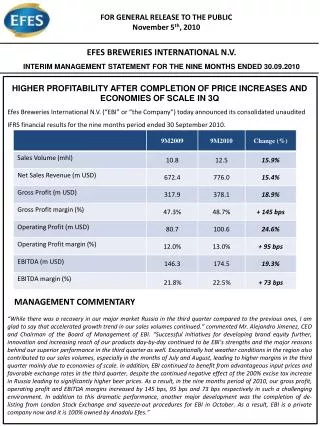

Download

1 / 32

320 likes | 445 Views

Crown Van Gelder N.V. Velsen. Annual results 2006. Presentation 9 February 2007. Agenda 9 February 2007. Opening Highlights 2006 Key figures Production volume and geographical spread of sales volume Pulp shipments, price and volume outlook Raw materials cost Finance

E N D

Crown Van Gelder N.V. Velsen Annual results 2006 Presentation 9 February 2007

Agenda 9 February 2007 • Opening • Highlights 2006 • Key figures • Production volume and geographical spread of sales volume • Pulp shipments, price and volume outlook • Raw materials cost • Finance • Results and outlook European paper companies • Outlook Deutsche Bank and Nordea • NBD • Outlook CVG for 2007 • Questions

Highlights 2006 • Net result EUR 2.2 million, down 75% on revised 2005 • Sales volume increase of 4.2% to 208,800 ton • Selling price up by 1% on 2005 • NBD in line with expectation (15,000 ton) • Dividend proposal of EUR 1.00 per share certificate (196% pay out) • Restructuring of paper industry making a good pace

Key figures 2002-2006 1) 2005 figure revised

WF Uncoated European order inflow total – 3 weeks average Bron: Cepifine

Production and sales volume CVG Geographical spread of sales volume CVG 15% 10% Netherlands Outside Europe 6% 19% Other Europe France 15% Belgium/Luxembourg 22% 13% Germany United Kingdom

Shipments of Market Pulp in million tons 2005 Bron: Das Papier

NBSK (benchmark pulp) Voorwaarden: termijncontracten CIF West-Europese havens Bron: FOEX/PIX-index

BHKP Voorwaarden: termijncontracten CIF West-Europese havens Bron: FOEX/PIX-index

Consolidated profit & loss account (EUR x 1,000) (unaudited)

Consolidated Balance Sheet (before profit appropriation) (EUR x 1,000) (unaudited)

Consolidated Cash Flow Statement (EUR x 1,000) (unaudited)

Pension accounting Comparison of differences in pension accounting (“corridor approach” versus “SoRIE approach”

StoraEnso results Sales EUR 14,6 billion; 43,900 employees • Net profit of EUR 589 mln (2005: EUR -107 mln revised) • Non-recurring items EUR -134 mln (2005: EUR -417 mln) • Operating profit Fine Paper division EUR 166 mln (2005: EUR 62 mln) • Sales volume up 9% to 3.8 mln ton (7 weeks strike in 2005) • Selling price Fine Paper up 1% • ROCE Fine Paper 7.1% (2005: 2.4%)

UPM-Kymmene results Sales EUR 10,022 mln; 28,704 employees • Net result increased from EUR 261 mln to EUR 338 mln in 2006 • Non-recurring items EUR -189 mln (2005: EUR -240 mln) • Operating profit Fine and Speciality Papers division increases from EUR 85 mln to EUR 108 in 2006 • Sales volume up 16% to 3,550 mln ton (2005: effect of Finnish strike and start-up papermachine in China) • Selling prices -1% (2005: -1%) • ROCE up to 5.4% (2005: 3.3%)

M-Real results Sales EUR 5,6 mln; 14,125 employees • Net result of EUR -399 mln (2005: EUR -80 mln) • Non-recurring items EUR -316 mln (2005: EUR 32 mln) • Operating profit Office Paper Division EUR 7 mln (2005: EUR 4 mln), excluding non-recurring items • Sales volume up by 0.5% to 1,039 mln ton • Selling prices +2.8% • ROCE Office Paper Division 1.0% (2005: 0.6%), including non-recurring items -2.3% (2005: -0.5%) • EUR 15 mln write down on Wifsta mill (closure June 2007)

Outlook • Board of Directors StoraEnso: “In Europe the outlook for fine paper remains healthy, with demand and shipments in the first quarter predicted to be up on a year ago and the previous quarter. Higher prices are anticipated in uncoated fine paper, and price increases have been announced in coated fine paper …..” • UPM-Kymmene: “Demand for printing papers is forecast to grow somewhat from last year. The strongest growth in demand will be in emerging markets. We expect paper deliveries to increase over last year. Average paper price is slightly higher in Q1 2007 than Q4 2006.”

Outlook • Mikko Helander (CEO M-Real): “In fine paper products, capacity utalization rates are very high at the beginning of the year. We have initiated measures to increase the prices of fine paper products and are currently confident that we will be able to push through these increases at least in part. Our result for 2007 will be burdened by an increase of production input costs, estimated at more than EUR 100 million. In order to achieve a positive result before taxes …. we must be able to raise the prices of our paper products.”

ROCE Comparison CVG and Peer Group

Pulp production to be modernised 1Q08 PM3 modernization 4Q07 PM4 to be converted 2Q07 Stora Enso Oulo Stora Enso Veitsuluoto PM6 to be closed 2Q07 PM2 limited 1Q07 IP Svetogorsk Pulpline to be closed 2Q07 Stora Enso Varkaus M-Real Husum ‘0606: - 700,000 t / -2,500 employees ‘0701: Investment in Jämsänkoski mill PM8 overhauled 1Q06 UPM Jämsänkoski M-Real Kangas UPM Tervasaari To be closed 1H07 ‘0606: - 370,000 t / - 2,500 employees M-Real Wifsta Warf Ahlstrom UPM Voikkaa ‘0701: - 235,000 t WFU / - 215,000 t SC UPM Kymi Sold to financial investor 1H06 SE Grycksbo ‘0606: - 120,000 t WFU / - 240 employees PM7 Closed 3Q06 ‘0701: - 175,000 t WFU / - 310,000 t WFC Klippan Bankrupt, sold to investor Closed down Mondi Syktyvhar Mill closed 3Q06 ‘0606: - 45,000 t WFU Cham Hunsfos IP Taite ‘0701: Future growth outside North America Coater shut down 2H06 A. Wiggins Question mark ‘0606: + 500,000 t WFU in 2009 ? PM1 modernization 4Q07 Stora Enso Nymölla ‘0701: Focus WFU A4 and sheets To be closed 2007/08 To be closed 2007 Under review 2007 IP Kwidzyn SE Uetersen UPM Nordland Arctic Kostryn M-Real UK Paper Drewsen SE BPF To be closed 2007 Closed down SE Reisholz Sappi Maastricht Sappi Nash PM6 & 7 to be closed Feb 2007 M-Real Zanders (Gohrsmühle) M-Real Alizey Reorganisation 2006 M-Real PWA (Stockstadt) Reorganisation 2006 SE Corbehem Köhler M-Real PSM Mondi Ruzomberok PM3 & PM4 closed 2Q06 Mondi Ybbstal/Kematen UPMDocelles IP Maresquel Mondi Szolnok Ziegler Mondi Dunaujvaros Cham Sold to investor 2Q06 Goricane Mill closed 3Q06 Ahlstrom Sibille Tenero IP USA sold coated and superc. business (2,000,000 tpa) 2Q06 Pap. de Cran IP Saillat Pont de Claix PM1 revamp 2Q06 Sold to Trierenberg 2006 Zicunaga IP USA will convert 350,000 t uncoated to 500.000 t liner board 2007 Start-up new 500K tpa WFU PM planned 1H09 ? Receivership Until July 07 Closed down 2006 Question mark Mill closed 2006 Soporcel IP China Studying uncoated freesheet machine IP Brazil expansion focus uncoated paper Mondi RSA PM31 switch to WFU office paper late 2005

Deutsche Bank Sector Outlook CAGR New estimates

Deutsche Bank Sector Outlook New estimates

World players of digital printers Xeikon 6000 Inkjet = contactloos & snel Versamark VT 3000 / VX 5000 NBD HP Indigo 3250 Xerox iGen3 Oce Variostream 9000

Development of printing presses Source: PIRA International

Development digital printing Source: PIRA International

Outlook for 2007 • Volume up to 217,000 ton • Positive effect of reduction in capacity will gain momentum • Gradual price increases • Cost pushes from pulp price and energy costs • Strict control on costs and investments • Outlook 2007 yet uncertain

Product portfolio Questions