Download

1 / 9

90 likes | 213 Views

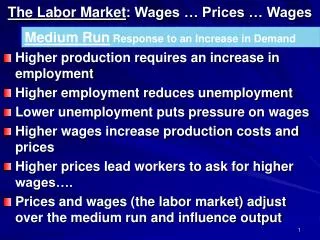

Higher Oil Prices and Africa’s Growth Prospects. John Page The World Bank January 2006. Crude oil price 1970-November 2005. 80. 70. Current price. 60. Price in 2000$ by US GDP. 50. deflator. 40. price /bbl. 30. 20. 10. 0. 1970. 1971. 1972. 1974. 1975. 1976. 1977. 1979.

E N D

Higher Oil Prices and Africa’s Growth Prospects John Page The World Bank January 2006

Crude oil price 1970-November 2005 80 70 Current price 60 Price in 2000$ by US GDP 50 deflator 40 price /bbl 30 20 10 0 1970 1971 1972 1974 1975 1976 1977 1979 1980 1981 1982 1983 1984 1985 1986 1987 1989 1990 1991 1992 1993 1994 1995 1996 1998 1999 2000 2001 2002 2003 1973 1978 1988 1997 2004 Jul-05 Jan-05 Feb-05 Apr-05 Jun-05 2005-08 2005-09 2005-10 2005-11 Mar-05 May-05 The current oil shock – a cyclical upturn • The current rise in oil prices started in 1999 • In real terms, its magnitude is now approaching the previous peak in 1979-80 Data sources: World Bank DECPG Price data.

Offsetting factors (1) – currency appreciation • Relative to a basket of currencies (and except recently), the dollar has depreciated by 15 to 18% since 2002 • CFAF, rand have been appreciating. The US dollar exchange rate

Offsetting factors (2) – favorable terms of trade • The index of oil to non-oil commodity prices has been favorable from 2001 to early 2004. • The current increase in the relative price index is still about half of the oil shock in 1999-2000 Data sources: World Bank DECPG commodity price data.

The overall terms of trade impact… Terms-of-Trade Impacts of Commodity Price Changes • The income impact in 2004-05 is half of the 1999 shock • But cumulatively, the total effect on income is -2.3% of GDP • Still a real and permanent shock

Growth has been more robust • Growth in SSA during 2003-04 was 4.4% p.a. (versus 3% in 1999-2000) • 13 countries grew strongly (greater than 6% p.a.), averaging 9.2% (versus 4.1% in 1999-2000) • 16 countries grew moderately (between 3 to 6% p.a.), averaging 4.3% (4.0% in 1999-2000) • 11 countries grew slowly (less than 3% p.a.), averaging 2.2% (1.5% in 1999-2000) • The 4 countries whose economies shrank in 2003-04 (Cote D’Ivoire, Seychelles, CAR, Zimbabwe) averaged -4.7 p.a. (versus 0.1% growth in 1999-2000). However, their poor performance was attributable to non-oil related problems.

Outlook for Sub-Saharan Africa • To date, the economic impact of oil prices has been muted… • Growth will only decline slightly in 2005 and will recover in 2006 • Inflation (lowest in 2 decades in 2004) has increased in 2005 but is expected to decline in 2006 • The concern is that TOT may deteriorate further if non-oil commodity prices ease Data sources: WB Africa region SPA country datasheets. Averages are unweighted.

Policy options for oil importing countries • Combination of adjustment and additional financing • The shock is viewed as permanent and many SSA countries already adjusting to higher oil prices, • Macroeconomic adjustments • Combination of macro adjustments • exchange rate policies to facilitate expenditure switching • absorption reduction through domestic demand management • Microeconomic adjustment -- energy pricing policies: • For African countries – adjustment has been mainly through prices rather than quantities • Out of 44 countries, 24 fully or extensively passed through prices • Partial adjustment in prices in 15 countries • No adjustment of prices in 5 countries

Policy options for oil importing countries (contd.) • Composition of public expenditures • Implications for budget allocations as macro. and micro. adjustments are undertaken • Key questions • Should the budget subsidize energy prices for the poor? What mechanisms should be used and how should it be financed? • What should be the government’s priorities, across programs and within each priority program? What programs should be maintained and which should be cut?