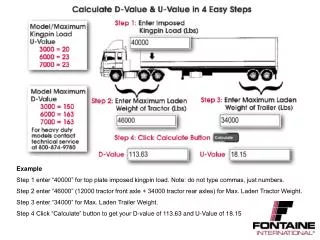

Download

1 / 75

750 likes | 908 Views

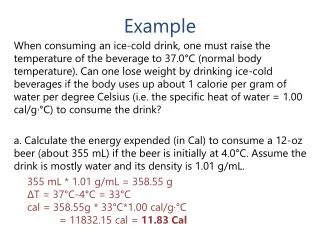

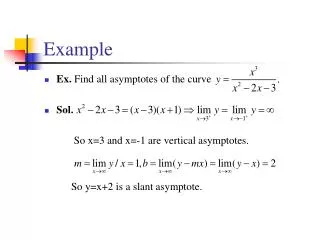

Example (cont'd). Dr.Import duties1 000 Cr. Bank1 000NO VAT is charged on import duties as import duties is a tax on its own. Example

E N D

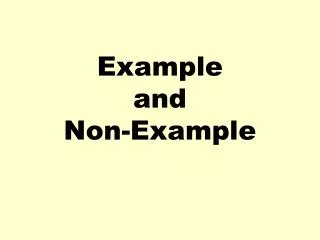

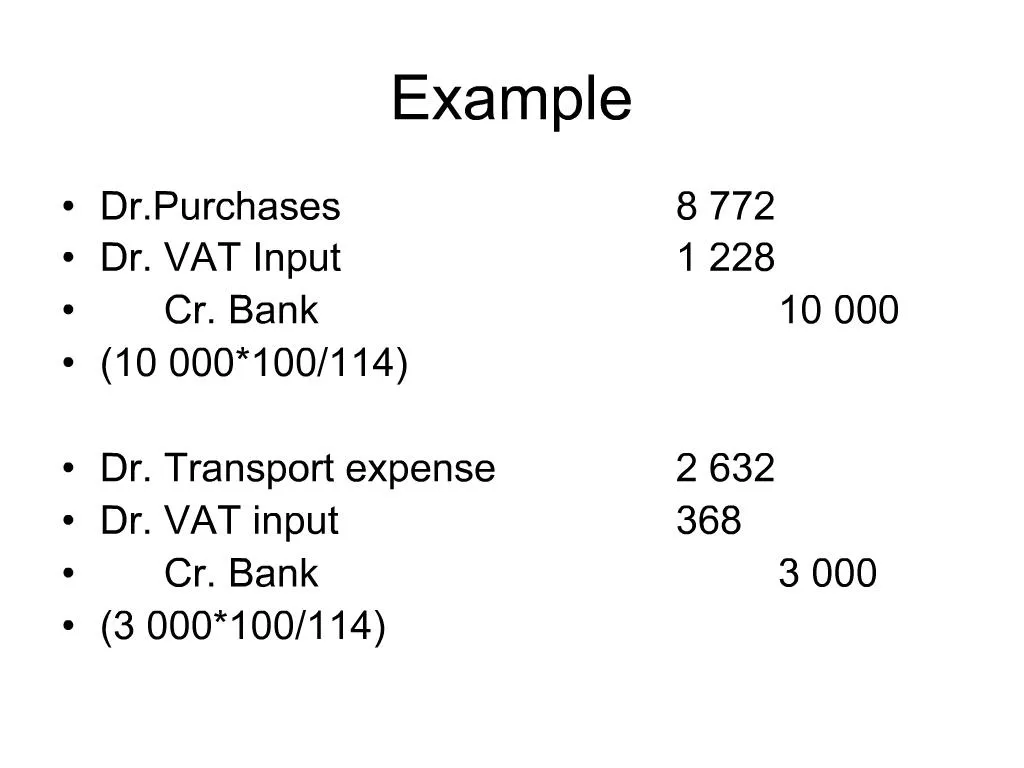

1. Example Dr.Purchases 8 772

Dr. VAT Input 1 228

Cr. Bank 10 000

(10 000*100/114)

Dr. Transport expense 2 632

Dr. VAT input 368

Cr. Bank 3 000

(3 000*100/114)

2. Example (cont�d) Dr. Import duties 1 000

Cr. Bank 1 000

NO VAT is charged on import duties as import duties is a tax on its own

3. Example � Total cost of inventory Purchases 2 000

Transport inwards 500

Transport outwards 400

Import duties on bags 100

Wages of staff to unpack

bags on delivery at stall 200

Wages of delivery staff that

Delivers bags to customers 300

4. Solution Purchases 2 000

Transport inwards 500

Import duties on bags 100

Wages�delivery at stall 200

2 800

Assuming a 50% mark-up on cost, calculate the selling price

Selling price = cost + mark-up

= 2 800 + 1400 (50%*2800)

= 4 200

5. Purchases returns Example

Returned 10 of the 50 bags bought in Lesotho.

Value of the closing stock is R11 200

Periodic method

Dr. Bank 2 000

Cr. Purchases 2 000

6. Example (cont�d) At the end of the accounting period:

Dr. Cost of Sales (10 000-2 000) 8 000

Cr. Purchases 8 000

Dr. Cost of Sales 4 000

Cr.Transport expense 3 000

Cr. Import duties 1 000

7. Example (cont�d) Dr. Inventory 11 200 Cr. Cost of Sales 11 200 Dr. Cost of Sales Cr Purchases 8 000 Inventory 11 200 Transport 3 000 Balance c/d 800 Import duties 1 000 12 000 12 000