Download

1 / 52

520 likes | 719 Views

COMMON PROVISIONS. 2. FINANCIAL ASPECTS. CONGRATULATIONS. GRANT The EU contributes to the costs The EU does not pay for a service/deliverable/product Successful utilisation of the grant depends on: Successful implementation of the project, AND

E N D

COMMON PROVISIONS 2. FINANCIAL ASPECTS

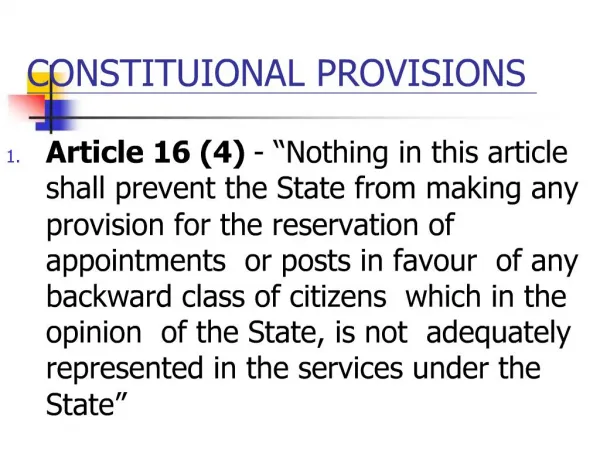

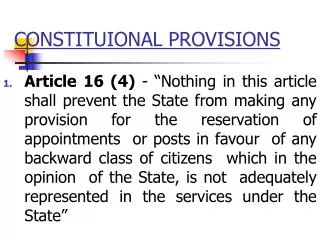

CONGRATULATIONS • GRANT • The EU contributes to the costs • The EU does not pay for a service/deliverable/product • Successful utilisation of the grant depends on: • Successful implementation of the project, AND • The quality of the project accounts/financial report • If the the financial rules are not followed to costs may be declared ineligible – as a result the final grant may be reduced.

Reference documents • Grant Agreement (Art 1 & 2) • Common Provisions (CP) (Art 15.2, 24, 25 and 26) • Application guide (Env p 42-52, Inf p 45-54 , Nat p 60-70) • Financial Forms • Guidelines to forms, • http://ec.europa.eu/environment/life/toolkit/pmtools/lifeplus/financial_reporting.htm or /timesheets

CONTRIBUTION PRINCIPLES • The grant agreement sets the contribution as a fixed percentage of total eligible costs and a maximum contribution amount.(art. 24.1) • It may not exceed the amount necessary to balance project expenses and revenues. • All revenues generated by the project must be declared.(art. 24.4) • If an associated beneficiary reduces its contribution, the coordinating beneficiary must find additional resources.(art. 4.5)The Life contribution will not be increased ! • Commission may proportionally reduce the Community contribution.(art. 18 and 24.5) • Eligible expenses are limited to the amounts foreseen by cost categories. (30 000 € and 10% overspending rule) (art 15.2) LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

METHODS OF PAYMENT OF THE CONTRIBUTION (art. 28) • General rule : 3 instalments : • 1st pre-financing = 40 % of contribution max. amount • Mid-term pre-financing = 30 % of contribution max. amount • Final payment = Balance (maximum 30 %) • Small projects with an implementation period ≤ 24 months or a Community contribution ≤ 300 000 € : • 1st pre-financing increased to 50 % of contribution max. amount • Final payment = Balance (maximum 50 %) LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

THE 1st PRE-FINANCING (art. 28.2) • Grant agreement is signed by both parties • Payment request states coordinating beneficiary and bank data details • A guarantee issued by a bank or an insurance company may be requested by the Commission during the revision phase: • equals the amount of the 1st pre-financing • covers the duration of the project + 6 months

INTERESTS ON PRE-FINANCING (art 24.7) • The coordinating beneficiary shall inform the Commission of the amount of any interest or equivalent benefits yielded by the 1st pre-financing amount. • Interest will be deducted from the final payment. • Exceptions : • When 1st pre-financing ≥ 750.000 € : beneficiary informs the Commission every January how much interest has been earned – Commission sends a Recovery Order. • When 1st pre-financing ≤ 50.000 € : interest not due

Member States and interest on pre-financing For Coordinating Beneficiaries registered as public law bodies by the Commission: • Ministries, regions; departments, länder, provinces etc. • Cities, municipalities, communes • Research centres, universities • Interest on pre-financing will not be recovered by the Commission. • However, it must be reported in the financial statement as income to the project. • These beneficiaries are not entitled to interest in case of late payment of the grant by the Commission . LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

THE MID-TERM PRE-FINANCING (art. 28.3) • After at least 150 % of 1st pre-financing has been used • Exception : Mid-term payment possible even if the 1st pre-financing payment has not been paid : • when at least 60 % of max. contribution has been spent • amount = % set in grant agreement x eligible costs to date • Paid upon approval by the Commission of : • a request for payment • a mid-term technical report + statement of expenditure • auditor’s details • Mid-term reports must be submitted no later than 9 months before the end of the project

THE BALANCE (FINAL PAYMENT) (art. 28.4) • Upon approval, by the Commission, of : • the final technical report • the final statement of expenditure and income • the audit report if required (cf. art. 31) • Final reports must be submitted no later than 3 months after the end of the project

Independent Financial Audit (art. 31) • An independent auditor, nominated by the coordinating beneficiary, shall verify the final statement of expenditure and income • for all projects with a max. Community contribution ≥ 300 000 € • following the format provided on the Life website / toolkit • The auditor will verify : • the implementation of the project • the eligibility of declared costs + compliance with CP • compliance of costs with national legislation and accounting rules • the declaration of all project income (including interests on pre-financing) • compliance with rules for public and/or competitive tender (art 8.4) • the origin of beneficiaries’ own contribution

REPORTING REQUIREMENTS (art. 29) • Financial report covers the same period as the technical report • Reports follow the guidelines & templates cf. Life website / toolkit • In € • When beneficiary’s accounting is not in €: exchange rate of the 1st working day of the year in which the expenditure is paid (cf. E C B website http://www.ecb.int/stats/exchange/eurofxref/html/index.en.html) • The coordinating beneficiary certifies that the submitted information is full, reliable, true and complies with the CP, that costs are actual, that all income has been declared • Financial supporting documents are not attached but may be requested later. Retained by coordinating beneficiary (art 6.1)

ELIGIBLE COSTS (art. 25) • Provided for in the budget of the project or have been authorized through an amendment to the grant agreement • Directly linked to, and necessary for, carrying out the project • Reasonable and comply with the principles of sound financial management • Compliant with applicable tax and social legislation • Incurred and recorded in the beneficiaries’ accounts during the lifetime of the project: • legal obligation to pay contracted after the signature of the grant agreement • corresponding action implemented after start date and before end date of the project • fully paid before the submission of the final report LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

PERSONNEL COSTS(art. 25.2) • Related to employees salaries (no external assistance) • Service contracts : mandatory condition : work in the beneficiary’s premises and under its supervision (timesheets) • NB : civil servants salary costs: sum of public bodies’ contributions must exceed by at least 2 % the sum of civil servants’ costs Supporting Documents Principles • Based on actual time devoted to the project Timesheets • Based on actual gross salary / wages + obligatory social charges Pay slips

Example of budget: Personnel Civil servants 105 € Others 20 € External Assistance 50 € Equipment 25 € Total 200 € Life+ contribution = 50% but Minimum own contribution from public beneficiaries = 105 € + 2 % = 107,10 € Maximum Life+ contribution = 92,90 € CIVIL SERVANTS’ SALARY COSTS (art. 25.2)

Annual personnel costs • Annual gross salary actually paid – no estimates. • Obligatory social charges • Private Pension contributions are eligible if the employer is legally obliged to provide it. • Compensation received from insurance or other schemes in case of sickness, maternity leave, re-employment schemes to reactivate unemployed people etc. must be deducted from annual salary. • Not eligible: i.e. company car, bonuses, similar fringe benefits LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Productive time Time of actual work, including: • Overtime and Time worked during national holidays or week ends. • Meetings • Mandatory Training courses LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Non productive time • Holidays actually taken • National holidays • Flexitime compensation • Week ends • Sickness/other absences (including maternity leave etc) LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Calculation of personnel costs LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Recommendations for time sheets/time registration • Identify employee and LIFE project • Daily registration • Ideally detailed per action • Ideally document total hours worked to secure correct calculation of time unit rate • Signed and validated during the first week following the month of registration

Model time sheet LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Example 2 – a reliable time sheet LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Example of an unreliable time sheet – 29/31 February LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Example of an unreliable time sheet – monthly subtotals LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Example of an unreliable time sheet- generic time LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

TRAVEL COSTS(art. 25.3) Principles Supporting Documents Charged in accordance with internal rules of the beneficiary Flight tickets, hotel bills,…. Journeys by car : based on distance and internal rules • Internal rules for re-imbursement of travel expenses • Detailed specification of travel expenses, two lines if necessary, i.e. destination, # of persons, # km, # nights etc. • Group low value travel expenses (supported by accounting documents offering same level of detail, eg. driving log-book). • Excluding costs incurred by external consultants, journeys between home and work place. LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

EXTERNAL ASSISTANCE(art. 25.4 & application guide) • Tender procedures • must comply with Community and national legislation. • Naming the subcontractor in the revised budget does not exempt the beneficiary from applying the normal tendering procedure. • NEW for LIFE+ - competitive tenders for private beneficiaries – obligatory for orders over €125.000. • Project beneficiaries/co-financiers cannot act as subcontractors/suppliers.

DURABLE GOODS(art. 25.5- 25.12 & Application guide) • For infrastructure and equipment (LIFE ENV, LIFE INF, LIFE BIO) - depreciation only is eligible. • Each beneficiary applies its internal accounting rules for depreciation charges. National accounting standards and the principle of consistency must be respected. • Only depreciation strictly related to the use for the project is eligible: the calculation must take into account the period and the rate of the actual use for the project. • Durable goods which must be depreciated: • placed on the beneficiary's inventory of durable goods • treated as capital expenditure

DURABLE GOODS(art. 25.5- 25.12 & Application guide) • The Maximum Eligible depreciation charges: • Infrastructure costs: 25% of the total purchase cost • Equipment costs: 50% of the total purchase cost • Depreciation of durable goods purchased before the start of the project is not eligible for LIFE+ funding. It is covered by Overheads. LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

DURABLE GOODS (art. 25.5- 25.12 & Application guide) • PROTOTYPE – 100% eligible • (Only for Life+ Env and Life+ Bio) • Has never been commercialised • Not available as a serial product • Can not be used for commercial activities or sold during 5 years after the project end date LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

DURABLE GOODS (art. 25.5- 25.12 & Application guide) • Life+ NAT projects • If the beneficiary is a public body or a non-governmental / private non-commercial organisation: • 100% eligible for infrastructure and equipment used extensively in project implementation and assigned to nature conservation after the end of the project. • If the beneficiary if a commercial organisation: • Durable goods must be depreciated. LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

LAND PURCHASE LIFE+ Nature:“Environmental clause” (art. 35.1) • Costs of land purchase or long-term lease of land/use rights are only eligible for Life+ Nature projects • Purchase prices are based on market terms • Assign the purchased assets definitively to nature conservation activities beyond the end of the project • Coordinating beneficiary ensures that the entry in the land register includes a guarantee that the land will be assigned definitively to nature conservation • Land purchased by private organizations: guarantee that the land property will be transferred to a legal body primarily active in the field of nature protection (if the beneficiary ceases to exist)

OTHER BUDGET POSTS Budget Posts Supporting Documents • CONSUMABLE MATERIAL(art. 25.11) • General office supplies are covered by Overheads Detailed invoices • OTHER COSTS(art. 25.12) • Costs necessary for the project, not falling within a defined category Detailed invoices • OVERHEADS(art. 25.13) • maximum 7 % of the total amount of eligible direct costs, excluding land purchase costs Invoices notneeded • Income(art. 24.4) • Associated beneficiaries, co-financiers and direct revenues Receipts etc

Income LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

INELIGIBLE COSTS Non exhaustive list. See art. 26 of Common Provisions • Costs in any category of expenditure over and above that foreseen in the budget plus 10% and 30 000 € (as referred to in art. 15.2) • VAT (see art. 30) • Costs incurred in relation to activities not foreseen in the project • Costs incurred for the purchase of durable goods or communication material not bearing theLIFE logo (and the Natura 2000 logo, when applicable) • Cost incurred for an action which benefits from aid under other Community financial instruments • Costs for which a beneficiary already receives an operating grant from the Commission during the period in question • Costs related to any action considered as a compensatorymeasure • Costs relating to management plans, action plans and similar plans, drafted or modified in the context of a LIFE+ project, if the related plan is not legally operational before the project end date LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Partnership agreements art. 4.8 of Common Provisions • The Commission does not accept or reject partnership agreements - the Commission only highlights possible problems. • To ensure that the participants have the tools to solve their problems. • Not sufficient to refer to the Common Provisions, i.e. liabilities between participants, member states laws in case of dispute, payments from CB to AB. LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Specific instructions for Financial Reporting • Do not wait until the mid-term or the final report before preparing theStatement of Expenditures. It is required: • In all reports (Art. 12.2 CP) • At the occasion of all Monitoring Visits • Ensure that Coordinating Beneficiary receives data from Associated Benefifiaries on a regular basis. LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Specific instructions for Financial Reporting • Be careful:self-invoicingand invoicing among beneficiaries is not allowed. • Verify that all columns of the financial forms are properly filled-in • Send as soon as possibile the declaration for thenon-recoverability of VATby beneficiaries. LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

A FEW REMINDERS … (art. 6) • All beneficiaries • Must contribute financially to the project’s costs • Shall maintain up to date books of accounts • Shall keep all supporting documentation for all expenditure and income for at least 5 years after the final payment • Ensure that all invoices include a clear reference to the project and a link to the analytical accounting system • May not act as sub-contractor/supplier to each other (no invoicing among partners !!) LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw

Ineligible on formal grounds - difficult to rectify at a later stage • Register time worked for the project on a daily basis using time sheets. • Respect the public tender/competitive tender. • Provide all information asked for in the financial reporting. • Provide sufficiently detailed description (quantity where appropriate) to justify eligibility. • Costs incurred by non-beneficiaries (Company groups) – not eligible if separate legal entities. • Purchases from sister companies (separate legal entities) and sister departments (same legal entity) – best value and excluding profit, overheads etc (art 26 9th) LIFE09 Kick-off Meeting, 13 January, 2011, Warsaw