Download

1 / 50

530 likes | 690 Views

11. MONEY, INTEREST, REAL GDP, AND THE PRICE LEVEL. CHAPTER. Objectives. After studying this chapter, you will able to Explain what determines the demand for money Explain how the Fed influences interest rates

E N D

11 MONEY, INTEREST, REAL GDP, AND THE PRICE LEVEL CHAPTER

Objectives • After studying this chapter, you will able to • Explain what determines the demand for money • Explain how the Fed influences interest rates • Explain how the Fed’s actions influence spending plans, real GDP, and the price level in the short run • Explain how the Fed’s actions influence real GDP and the price level in the long run and explain the quantity theory of money

Ripple Effects of Money • There is enough money in the United States today for everyone to have a wallet stuffed with $2,300 in notes and coins and another $19,000 in the bank. • Why do we hold so much money? • Through 2001, as the economy slowed, the Fed cut interest rates 11 times. • In 2002 and 2003, the Fed cut the interest rate even further to historically low levels. • How does the Fed change the interest rate and with what effects?

The Demand for Money • The Influences on Money Holding • The quantity of money that people plan to hold depends on four main factors • The price level • The interest rate • Real GDP • Financial innovation

The Demand for Money • The price level • A rise in the price level increases the nominal quantity of money but doesn’t change the real quantity of money that people plan to hold. • Nominal money is the amount of money measured in dollars. • The quantity of nominal money demanded is proportional to the price level — a 10 percent rise in the price level increases the quantity of nominal money demanded by 10 percent.

The Demand for Money • The interest rate • The interest rate is the opportunity cost of holding wealth in the form of money rather than an interest-bearing asset. • A rise in the interest rate decreases the quantity of money that people plan to hold. • Real GDP • An increase in real GDP increases the volume of expenditure, which increases the quantity of real money that people plan to hold.

The Demand for Money • Financial innovation • Financial innovation that lowers the cost of switching between money and interest-bearing assets decreases the quantity of money that people plan to hold.

The Demand for Money • The Demand for Money Curve • The demand for money curve is the relationship between the quantity of real money demanded (M/P) and the interest rate when all other influences on the amount of money that people wish to hold remain the same.

The Demand for Money • Figure 27.1 illustrates the demand for money curve. • The demand for money curve slopes downward • A fall in the interest rate lowers the opportunity cost of holding money and brings an increase in the quantity of money demanded--a movement downward along the demand for money curve.

The Demand for Money • A rise in the interest rate increases the opportunity cost of holding money and brings an decrease in the quantity of money demanded--a movement upward along the demand for money curve.

The Demand for Money • Shifts in the Demand for Money Curve • The demand for money changes and the demand for money curve shifts if real GDP changes or if financial innovation occurs.

The Demand for Money • Figure 27.2 illustrates an increase and a decrease in the demand for money. • A decrease in real GDP or a financial innovation decreases the demand for money and shifts the demand curve leftward. • An increase in real GDP increases the demand for money and shifts the demand curve rightward.

The Demand for Money • The Demand for Money in the United States • Figure 27.3 shows scatter diagrams of the interest rate against real M1 and real M2 from 1970 through 2003 and interprets the data in terms of movements along and shifts in the demand for money curves.

The Demand for Money • The Demand for Money in the United States • Figure 27.3 shows scatter diagrams of the interest rate against real M1 and real M2 from 1970 through 2003 and interprets the data in terms of movements along and shifts in the demand for money curves.

Interest Rate Determination • An interest rate is the percentage yield on a financial security such as a bond or a stock. • The price of a bond and the interest rate are inversely related. • If the price of a bond falls, the interest rate on the bond rises. • If the price of a bond rises, the interest rate on the bond falls. • We can study the forces that determine the interest rate in the market for money.

Interest Rate Determination • Money Market Equilibrium • The Fed determines the quantity of money supplied and on any given day, that quantity is fixed. • The supply of money curve is vertical at the given quantity of money supplied. • Money market equilibrium determines the interest rate.

Interest Rate Determination • Figure 27.4 illustrates the equilibrium interest rate.

Interest Rate Determination • If the interest rate is above the equilibrium interest rate, the quantity of money that people are willing to hold is less than the quantity supplied. • They try to get rid of their “excess” money by buying financial assets. • This action raises the price of these assets and lowers the interest rate.

Interest Rate Determination • If the interest rate is below the equilibrium interest rate, the quantity of money that people want to hold exceeds the quantity supplied. • They try to get more money by selling financial assets. • This action lowers the price of these assets and raises the interest rate.

Interest Rate Determination • Changing the Interest Rate • Figure 27.5 shows how the Fed changes the interest rate. • If the Fed conducts an open market sale, the money supply decreases, the money supply curve shifts leftward, and the interest rate rises.

Interest Rate Determination • If the Fed conducts an open market purchase, the money supply increases, the money supply curve shifts rightward, and the interest rate falls.

Short-Run Effects of Money onReal GDP, and the Price Level • Ripple Effects of Monetary Policy • If the Fed increases the interest rate, three events follow: • Investment and consumption expenditures decrease. • The dollar rises and next exports decrease. • A multiplier process unfolds.

Short-Run Effects of Money onReal GDP, and the Price Level • Figure 27.6 summarizes these ripple effects.

Short-Run Effects of Money onReal GDP, and the Price Level • The Fed Tightens to Avoid Inflation • Figure 27.7 illustrates the attempt to avoid inflation.

Short-Run Effects of Money onReal GDP, and the Price Level • A decrease in the money supply in part (a) raises the interest rate.

Short-Run Effects of Money onReal GDP, and the Price Level • The rise in the interest rate decreases investment in part (b).

Short-Run Effects of Money onReal GDP, and the Price Level • The decrease in investment shifts the AD curve leftward with a multiplier effect in part (c).

Short-Run Effects of Money onReal GDP, and the Price Level • Real GDP decreases and the price level falls.

Short-Run Effects of Money onReal GDP, and the Price Level • The Fed Eases to Avoid Recession • Figure 27.8 illustrates the attempt to avoid recession.

Short-Run Effects of Money onReal GDP, and the Price Level • An increase in the money supply in part (a) lowers the interest rate.

Short-Run Effects of Money onReal GDP, and the Price Level • The fall in the interest rate increases investment in part (b).

Short-Run Effects of Money onReal GDP, and the Price Level • The increase in investment shifts the AD curve rightward with a multiplier effect in part (c).

Short-Run Effects of Money onReal GDP, and the Price Level • Real GDP increases and the price level rises.

Short-Run Effects of Money onReal GDP, and the Price Level • The size of the multiplier effect of monetary policy depends on the sensitivity of expenditure plans to the interest rate. • Limitations of Monetary Stabilization Policy • Monetary policy shares the limitations of fiscal policy, except that there is no law-making time lag or uncertainty. • It also has the additional limitation that the effects of monetary policy are long drawn out, indirect, and depend on responsiveness of spending to interest rates. • These effects are all variable and hard to predict.

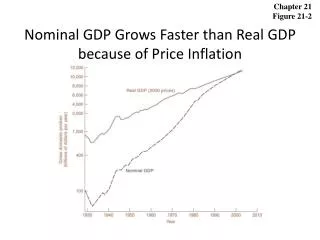

Long-Run Effects of Money onReal GDP and the Price Level • In the long run, real GDP equals potential GDP. • An increase in the quantity of money at full employment increases real GDP and raises the price level. • The money wage rate rises, which decreases short-run aggregate supply and decreases real GDP but raises the price level. • In the long run, an increase in the quantity of money leaves real GDP unchanged but raises the price level.

Long-Run Effects of Money onReal GDP and the Price Level • Figure 27.9 illustrates the effects of an increase in the quantity of money starting from potential GDP. • In part (a), the Fed increases the quantity of money and lowers the interest rate.

Long-Run Effects of Money onReal GDP and the Price Level • In part (b), aggregate demand increases • Real GDP increases to $10.2 trillion and the price level rises to 105.

Long-Run Effects of Money onReal GDP and the Price Level • With an inflationary gap, the money wage rate rises and short-run aggregate supply decreases. • The SAS curve shifts leftward, real GDP decreases to $10 trillion and the price level rises to 110.

Long-Run Effects of Money onReal GDP and the Price Level • Back in the money market, the rise in the price level decreases the quantity of real money. • The interest rate rises to 6 percent.

Long-Run Effects of Money onReal GDP and the Price Level • The Quantity Theory of Money • The quantity theory of money is the proposition that, in the long run, an increase in the quantity of money brings an equal percentage increase in the price level. • The quantity theory of money is based on the velocity of circulation and the equation of exchange. • The velocity of circulation is the average number of times in a year a dollar is used to purchase goods and services in GDP.

Long-Run Effects of Money onReal GDP and the Price Level • Calling the velocity of circulation V, the price level P, real GDP Y, and the quantity of money M • V = PY/M. • Figure 27.10 on the next slide graphs the velocity of circulation for M1 and M2 for 1963–2003.

Long-Run Effects of Money onReal GDP and the Price Level • The equation of exchange states that • MV = PY • The quantity theory assumes that velocity and potential GDP are not affected by the quantity of money. • So • P = (V/Y)M • Because (V/Y) does not change when M changes, a change in M brings a proportionate change in P.

Long-Run Effects of Money onReal GDP and the Price Level • That is, the change in P, P, is related to the change in M, M, by the equation: • P = (V/Y)M • Divide this equation by • P = (V/Y)M • and the term (V/Y) cancels to give • P/P = M/M • P/P is the inflation rate and = M/M is the growth rate of the quantity of money.

Long-Run Effects of Money onReal GDP and the Price Level • Historical Evidence on the Quantity Theory of Money • Historical evidence shows that U.S. money growth and inflation are correlated, more so in the long run than the short run, which is broadly consistent with the quantity theory.

Long-Run Effects of Money onReal GDP and the Price Level • Figure 27.11 graphs money growth and inflation in the United States from 1963 to 2003. • Part (a) shows year-to-year changes.

Long-Run Effects of Money onReal GDP and the Price Level • Part (b) shows decade average changes.

Long-Run Effects of Money onReal GDP and the Price Level • International Evidence on the Quantity Theory of Money • International evidence shows a marked tendency for high money growth rates to be associated with high inflation rates. • Figure 27.12 shows the evidence.

Long-Run Effects of Money onReal GDP and the Price Level • Correlation, Causation, and Other Influences • Correlation is not causation; money growth and inflation could be correlated because money growth causes inflation, or because inflation causes money growth, or because a third factor caused both. • But the combination of historical, international, and other independent evidence gives us confidence that in the long run, money growth causes inflation. • In the short run, the quantity theory is not correct; we need the AS-AD model.