Download

1 / 13

130 likes | 232 Views

Competing Accountabilities: Reframing the Governance Challenge for Responsible Investment. Heather Hachigian DPhil. Candidate, School of Geography and the Environment University of Oxford RII Webinar, March 26, 2013. Sovereign Wealth Funds (SWFs).

E N D

Competing Accountabilities: Reframing the Governance Challenge for Responsible Investment Heather Hachigian DPhil. Candidate, School of Geography and the Environment University of Oxford RII Webinar, March 26, 2013

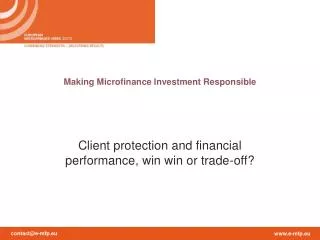

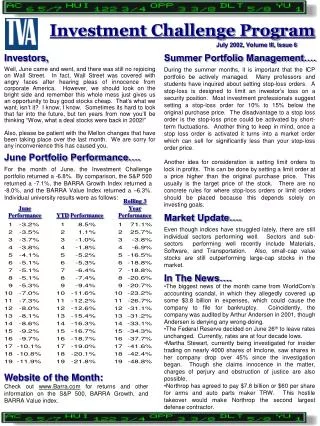

Sovereign Wealth Funds (SWFs) The term SWF was first used in 2005 to describe a class of institutional investors defined by their government ownership and lack of liabilities (outside of government) see Monk (2009). SWFs are not only features of autocratic countries; many democratic states have SWFs. SWFs are growing rapidly, from $1 trillion to over $4 trillion in 2012.

SWF Growth Assets under management $trillion USD Source: thecity UK Fund Management November 2012

The SWF Opportunity • For domestic constituents, well governed SWFs offer: • Relief from reliance on non-renewable resource revenue; • A mechanism for transferring wealth from current to future generations; and, • An opportunity to express national ethical values in global financial markets. • For the global economy, well governedSWFs offer: • Stabilization through their countercyclical investment tendencies; and, • More efficient global financial markets that incorporate ESG information.

Ambiguity, Uncertainty and Risk Risk and uncertainty are indeterminacies of the future. In contrast, ambiguity is an indeterminacy of the present (Best 2008). Uncertainty and risk can be reduced to subjective probabilities and calculable decision problems. Ambiguity, conversely, cannot be reduced, as the problem of communicating, interpreting and debating information remains, even after uncertainty is transformed to risk and risk is reduced to sophisticated decision problems.

The Relevance of Ambiguity SWF accountability relationships have greater scope for conflict than those of traditional fiduciary investors (e.g., public pension funds) Integrating extra-financial factors into investment decision-making depends on the ability to communicate, negotiate and interpret the valuation of intangible assets and discount rates for the future.

Norwegian Government Pension Fund- Global • One of the largest SWFs in the world, with $560 billion in AUM; • Invests entirely outside the Norwegian economy in public equities, fixed income and real estate; • Governed by three bodies: Ministry of Finance; Norwegian Central Bank; and Council on Ethics • Council on Ethics is responsible for screening criteria. • Norges Bank Investment Manager is responsible for ESG engagement.

Manifestation of Ambiguity in NGPF-G Socialised Ambiguity: Uncertainty that is a consequence of expectations and conventions that are irreducibly social and interactive, making it impossible to perceive probability relationships. To reduce uncertainty, governance frameworks are designed to encourage transparency (Norway is one of the most transparent SWFs in the world). But this ignores the second (socialised) source of uncertainty that cannot be resolved with more information. Flexibility embedded in institutional governance frameworks can help institutions to cope with the unknowable unknowns.

Manifestation of Ambiguity in NGPF-G Ambiguity of Conflict: The Principal-Agent problem in the context of investment manager and sponsor relationship. To reduce this form of ambiguity, governance frameworks appeal to asymmetric power relationships, either by delegating power to the investment manager or leaving it with the sponsor. But this raises other problems: For example, the Ministry sets the universe of investment, but this can undermine NBIM’s ability to change corporate behaviour through engagement. Negotiation can contribute to expanding the realm of what is possible.

Manifestation of Ambiguity in NGPF-G Ambiguity of meaning: An appeal to fiduciary duty seeks to eliminate intersubjective interpretations. In absence of a mechanism for addressing consequences of its entrenchment, fiduciary duty can contribute to inertia. By focusing on eliminating intersubjective forms of ambiguity, we have ignored the ambiguity manifesting in other forms (e.g., interests that are served by a particular interpretation of a rule). Reflexivity allows the Fund to see through the problems that it faces and allows new ideas to be integrated into the decision-making process.

Conclusion • Ambiguity differs from risk and uncertainty. • Investors must learn to manage ambiguitybecauseit is irreducible. • Managing ambiguity is particularly important for the effective implementation of RI programs. • Institutional investors must invest in their governance, embedding a degree of: • Flexibility • Negotiation • Reflexivity

Recommended Readings: Best, J. (2005). The limits of transparency: ambiguity and the history of internationalfinance. Cornell Univ Pr. Best, J. (2008), ‘Ambiguity, Uncertainty and Risk; Rethinking Indeterminacy’, International Political Sociology, 2(4), pp. 355-374. Clark, G. L., & Monk, A. (2010), ‘The Norwegian Government Pension Fund: Ethics over Efficiency’, Rotman International Journal of Pension Management, 3(1), 14-19. Crotty, J. 1994. Are Keynesian Uncertainty and Macro-theory Incompatible? Gelpern, A. (2011), ‘Sovereignty Accountability and the Wealth Fund Governance Conundrum’, Asian Journal of International Law 1(1) (January 2011). Preprint. Knight, F. H. (1921), Risk, Uncertainty, and Profit. Boston, MA: Hart, Schaffner & Marx; Houghton Mifflin Company. Mahoney, J. and Thelen, K. (2010). Explaining Institutional Change. Ambiguity; Agency and Power. New York, NY: Cambridge University Press Monk, A., (2009), Recasting the Sovereign Wealth Fund Debate: Trust, Legitimacy, and Governance 14(4), pp, 451-468. Contact Details: heather.hachigian@ouce.ox.ac.uk