Download

1 / 22

230 likes | 481 Views

Zero Tolerance Against Delinquency Alarm Signal System What to do at the Onset of Delinquency. Session Objective. Discuss indicators or “alarm signals” of delinquency Review strategies to respond timely and effectively to these alarm signals to prevent delinquency from escalating

E N D

Zero Tolerance Against DelinquencyAlarm Signal SystemWhat to do at the Onset of Delinquency

Session Objective • Discuss indicators or “alarm signals” of delinquency • Review strategies to respond timely and effectively to these alarm signals to prevent delinquency from escalating At the end of the session, account officers should be able to better detect causes of delinquency and have a “toolkit” of measures to apply to respond to and address delinquency

Zero Tolerance against Delinquency • Zero tolerance means NO LEVEL OF DELINQUENCY IS ACCEPTABLE! • It is the attitude of the bank management & staff towards loan delinquency – no level of late payment is acceptable. It is an institutionalculturein which late payments are totally unacceptable • The bank will aggressively pursue past due clients, whatever the cost, to establish and maintain zero loan delinquency.

Remedial Management Tools • Alarm Signals • Legal Processes

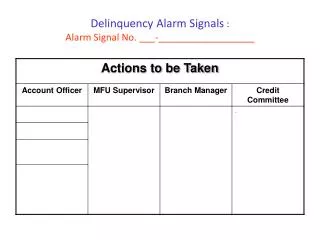

Delinquency Alarm Signals : Alarm Signal No. 1 - Payment is delayed one (1) day

Delinquency Alarm Signals : Alarm Signal No. 2 - Payment is delayed three (3) days

Delinquency Alarm Signals : Alarm Signal No. 3 - Payment is delayed one (1) week

Delinquency Alarm Signals : Alarm Signal No. 4 - Payment is delayed two (2) weeks

Delinquency Alarm Signals : Alarm Signal No. 5 - Payment is delayed three (3) weeks

Steps in enforcing Legal Action • Ensure that the borrower has received all three (3) demand/warning letters. Loan documents should be complete and in order in assuring a successful legal action and recovery. • File complaint in the Barangay Court • Letter of Complaint • Be ready with loan repayment scheme or program to be signed by the borrower • File complaint with the Local Court

NOTE :What is a Voluntary Offer to Surrender? • A document signifying the intent of the borrower to surrender any of his/her valuable item(s) on a specified period in case he/she fails to forward the full payment of the loan on an agreed date. The bank can sell the item(s) in case the borrower fails to pay the loan 5-10 days after surrendering the item(s). • Not a legal document, but binding. The ACT only becomes legal once the borrower signs an Authority to Sell; • Surrendering the item(s) does not extinguish the loan; loan is considered paid once the bank receives cash in payment for the loan

Delinquent Borrowers can be Classified into 3 Categories: • Borrower forgot to pay • Borrower not able to pay • Borrower not willing to pay

REMEMBER: Constant follow-up is one of the keys to preventing and remedying delinquency.

TDK Tutok, Dikit, Kulit