Download

1 / 8

80 likes | 296 Views

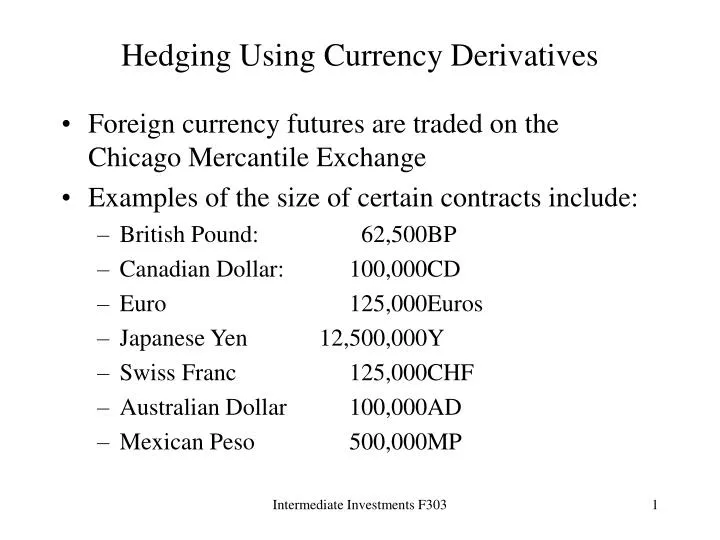

Hedging Using Currency Derivatives. Foreign currency futures are traded on the Chicago Mercantile Exchange Examples of the size of certain contracts include: British Pound: 62,500BP Canadian Dollar: 100,000CD Euro 125,000Euros Japanese Yen 12,500,000Y Swiss Franc 125,000CHF

E N D

Hedging Using Currency Derivatives • Foreign currency futures are traded on the Chicago Mercantile Exchange • Examples of the size of certain contracts include: • British Pound: 62,500BP • Canadian Dollar: 100,000CD • Euro 125,000Euros • Japanese Yen 12,500,000Y • Swiss Franc 125,000CHF • Australian Dollar 100,000AD • Mexican Peso 500,000MP Intermediate Investments F303

Hedging Using Currency Derivatives • Contract delivery months are: • March • June • September • December • Prices are normally quoted as USD per unit of foreign currency. So, for example: • USD/CHF = 0.60053 or 1.66 CHF = 1 USD • USD/Y = 0.007592 or 131.72 JPY = 1 USD • USD/BP = 1.43160 or .699 BP = 1 USD • USD/Euro 0.9062 or 1.104 Euro = 1 USD Intermediate Investments F303

When Might You Hedge a Foreign Currency Transaction? • Anytime your assets and liabilities are in different currencies • Let’s say your accounts receivable are in a foreign currency, but your accounts payable are in the domestic currency • Consequently, you are expecting receipts in one currency, but expect to make your payments in another • Use a Futures contract to lock in a rate. Remember: you are locking in an effective rate. You now have 2 distinct transactions which will offset each other to provide the effective rate you’ve locked in! Intermediate Investments F303

Example of a Foreign Currency Hedge • Make the following assumptions: • It is December 31 and your company has just signed a contract to sell 25 large earthmovers to a German mining company with delivery in exactly 6 months • Delivery price is EUR 25.0M • Delivery and payment of the earthmovers will be the end of June • Current USD/EUR exchange rate is 0.87936 • Price of a June contract for EUR is .8767 • In this particular case, You must make an initial outlay of USD $21M which you can borrow at 7.1225% • Should you undertake the project? Intermediate Investments F303

Example of a Foreign Currency Hedge (cont) • You borrowed USD $21M to get the project started. How much must you repay in 6 months if the annual interest rate is 7.1225%? • In order to break even, what must the Spot exchange rate be in June? • If you want to hedge, how do you decide if you buy or sell a contract? • If you’ll be receiving foreign currency you enter into a contract to deliver that currency • If you’ll be paying in a foreign currency, you enter into a contract to receive that currency Intermediate Investments F303

Example of a Foreign Currency Hedge (cont) • How many contracts do you have to sell? • You will deliver foreign currency in June at an exchange rate of .8767 • This will give you an “effective” exchange rate. What is the price you will receive in USD? • How does the hedge work if the exchange rate at maturity: • Falls to .8700 • Rises to .8900 • Remember: you have 2 distinct transactions that offset each other to achieve the effective rate! Intermediate Investments F303

Spot Futures Parity • If Spot Futures parity states that the Futures rate is equal to the current price plus a carrying cost, how can the futures rate on foreign currency exchange be less than the current spot rate? • Although risk free interest rates vary from currency to currency, you should not be able to make risk free profits simply through foreign currency trading • Interest rates should reflect the differences in exchange rates to prohibit arbitrage profits • So, just how does this work?? Intermediate Investments F303

Interest Rate Parity(cont) Intermediate Investments F303