Download

1 / 5

60 likes | 180 Views

5. Time series 5.1 Nature of the data Now temporal order , past data can affect future data (but not inversely) Randomness in C.S.: ≠ samples ≠ estimations/LS r.v. Randomness in T.S.: succession of indexed r.v. (t) stochastic process

E N D

5. Time series 5.1 Nature of the data Now temporal order, past data can affect future data (but not inversely) Randomness in C.S.: ≠ samples ≠ estimations/LS r.v. Randomness in T.S.: succession of indexed r.v. (t) stochastic process We can only see one “realization” of the r.v. since we cannot go back in t other conditions ≠ realizations Population: the collection of all possible realizations Sample: no. of periods considered

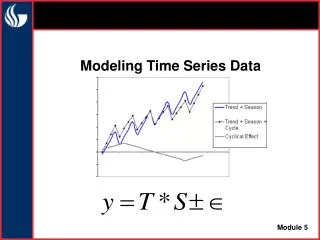

Examples: • Static model • Finite distributed lag model • Autoregressive model AR(p) 5.2 Trends and seasonality Trends Most of the series present a trend in t Sometimes we can conclude that two variables are related but in reality the two have a trend (spurious regression) A trend represents unobserved factors, and the associated coefficient represents the change in Y from one period to another

Seasonality When a variable is observed frequently take the season out (dummy) 5.3 Stationarity A definition of “weak” stationarity stems from: • A constant expected value • A constant variance • Autocovariance depends on lags and not on t • More, ergodicity (“to forget”) the more the variables are separated in t their correlation becomes smaller Ergodicity replaces the assumption of random sample, thus securing the law of the big numbers and the CLT

Some examples (stochastic processes) • White noise: succession of r.v., E(y)=0 & Var(y)= ct. indep. in t • Random walk: 1º differences are white noise • Mobil average (MA,q): weighted average of “noises” • Autoregressive (AR,p): lags of same series • ARMA(p,q): AR(p)+MA(q) • ARIMA (p,d,q): NON stationary (d: no. of times we differentiate) 5.4 Box-Jenkins methodology Parsimony: to predict an univariate TS, simpler models produce best predictions. The methodology has 3 steps: • Identification (SAF & PAF) • Estimation (Akaike & Schwarz) • Diagnosis (what to do now?)

In an stationary process the SAF & SAP are indep. in t, and decline rapidly towards 0 Box-Jenkins step-by-step • Calculate SAF & PAF of series and see their stationarity (if they are we move down to step 3, not 2) • Transform series (log&dif) and re-calculate SAF & SAP • Examine SAF & SAP and determine a starting point • Estimate the alternative (univariate) models • For each of the estimated models: • See if longest lag is significant (if not, reduce the order) • See SAF & SAP of errors • See Akaike, Schwarz, & adj-r2 of models (recall parsimony) • If we change our model move back to step 4