Download

1 / 10

100 likes | 243 Views

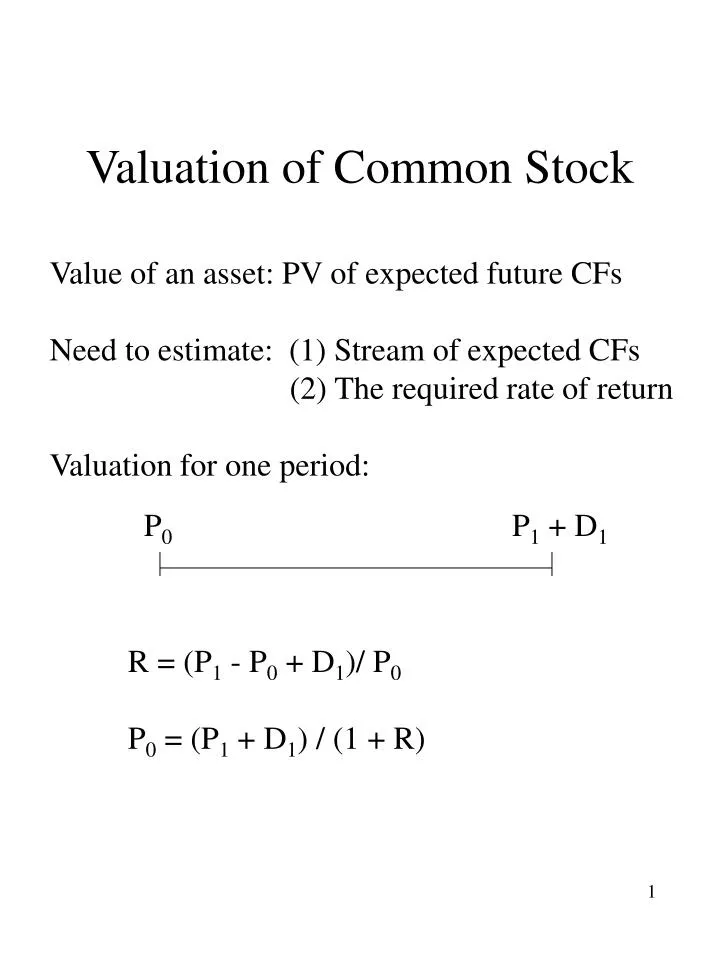

Valuation of Common Stock. Value of an asset: PV of expected future CFs Need to estimate: (1) Stream of expected CFs (2) The required rate of return Valuation for one period:. P 0. P 1 + D 1. R = (P 1 - P 0 + D 1 )/ P 0 P 0 = (P 1 + D 1 ) / (1 + R). Multi-period Valuation

E N D

Valuation of Common Stock Value of an asset: PV of expected future CFs Need to estimate: (1) Stream of expected CFs (2) The required rate of return Valuation for one period: P0 P1 + D1 R = (P1 - P0 + D1)/ P0 P0 = (P1 + D1) / (1 + R)

Multi-period Valuation P1 = (P2 + D2) / (1 + R) after successive substitutions, P0 = Dt / (1 + R)t Dividend Payment Patterns $ time

Constant Dividends P0 = D / R Constant Growth Dt = Dt-1(1 + g) P0 = D1 / (R - g) Supernormal growth P0 = Dt (1+G)/ (1 + R)t + Dm+1/(R-g)(1+R)m where G = growth rate during non normal growth period m = non normal growth period

FUTURES • The Futures contract • Futures Markets • CBT • Chicago Mercantile Exchange • CMX • The Clearinghouse • Initial margin • marking to market • Maintenance margin • Reversing trades • Open interest • Basis = spot price - futures price

FINANCIAL FUTURES • FX futures • Interest rate futures • Index futures • Spot and future prices F ---------- = S - PV of dividends, interest (1 + Rf) where F is the futures price, S is the spot price, Rf is the risk free rate

Creating an Index Portfolio Today At Delivery Buy t-bills -S0 S0(1 + Rf) Buy Futures Sd=S0(1+Rf) -D Net CF -S0 Sd + D You have replicated the return on an index.

Index Arbitrage F ---------- = S - PV of dividends, interest (1 + Rf) Suppose Rf = 4%, Dividend yield = 2% F = 5500 S= 5000 5500 5000x0.02 ------------ = 5288.46 5000 - ------------ = 4903.85 (1 = 0.04) (1 = 0.04) Purchase index at 5000 and sell them at delivery. Sell index at F, and sell T bills for 5000 that mature on the delivery date. Net cash flow is 0. At delivery date: Sd + 0.02x(5000) + (5500 - Sd) - 1.04(5000) 100 + 5500 - 5200 = 400 profit F must be 4903.85

FX and Commodity Futures FX Futures F RfFS ----------- = S - ----------- (1 + Rfd) (1 + RfF) rearranging: F (1 + Rfd) --- = ----------- S (1 + RfF) Commodity Futures F --------- = S + PV of storage costs - PV of conv. (1 + Rf) yield

Synthetic Futures 1. Interest Rate Futures: borrow for 1 yr, lend for two years Borrow $90.91 @ 10% for 1 year Lend $90.91 @8% for 2 years Borrow @10% +$90.91 -$100.00 Lend @ 8% -$90.91 $106.04 0 -$100.00 $106.04 Forward rate = (1.08)2/(1.10) - 1 = 0.0604

2. FX Futures Borrow $ today, change into FX and deposit. Equivalent to buying a forward contract S = DM 2 / $ R$ = 8% RDM = 6% Borrow $100 @ 8%, Convert into DM 200, Deposit DM 200 @ 6% and a year later withdraw your DM, pay your $ debt Now 1 year later $ DM $ DM Borrow 100.00 -108.00 Change -100.00 200.00 Lend -200.00 212.00 NCF 0 0 -108.00 212.00 Forward rate = 212 / 108 = DM 1.96 / $