Download

1 / 32

320 likes | 465 Views

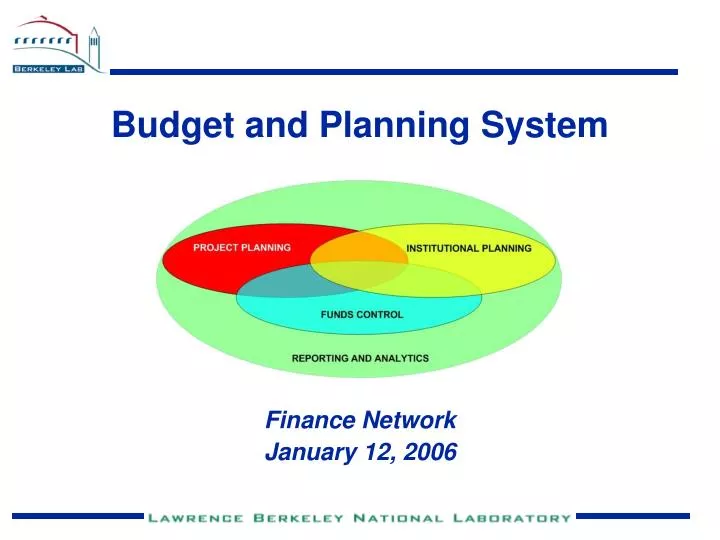

Budget and Planning System. Finance Network January 12, 2006. Topics. Background – Budget System Assessment and recommendations Budgeting overview Recent progress Timeline Funding information and process flow Funding, planning, and costing integration

E N D

Budget and Planning System Finance Network January 12, 2006

Topics • Background – Budget System Assessment and recommendations • Budgeting overview • Recent progress • Timeline • Funding information and process flow • Funding, planning, and costing integration • Communication, challenges, and collaboration

Budget System Assessment • In 2003-2004, a Budget System Assessment was performed to: • Reexamine the Laboratory’s multifaceted business requirements in the budgeting area; • Study the available solutions; and • Make recommendations regarding the best course of action for providing the Laboratory with a comprehensive, integrated budget system. • The ultimate goal will be to implement a comprehensive, integrated budget system which standardizes Lab-wide budgeting processes, improves reporting and controls, and reduces the use of redundant systems.

Web Navigation: OCFO Budget Office Budget System Assessment Report Budget System Assessment Report

Recommendation Implement Brookhaven National Laboratory’s Budget System at LBNL. Advantages: • Best fit to LBNL requirements. • Encompasses funds control and institutional planning functionalities. • Easily integrated with our PeopleSoft FMS. • Familiar look and feel. • Easily supportable technology. • It’s “free”.

Budget System Evaluation (Early 2005) • Added Division representatives to the Budget System core team. • Obtained access to a copy of the Brookhaven system for demonstration purposes. • Refined and prioritized the desired system functionality. • Conducted a fit-gap analysis of the Brookhaven software.

Fit-Gap Results Fit of the Brookhaven system to LBNL’s mandatory requirements: • Architecture and operational characteristics: 88% fit • Project and institutional planning: 68% fit • Funds control: 91% fit • Overall: 85% fit All of the gaps can be addressed through enhancements, interfaces, reporting, and procedures.

Recent Progress • Based on the fit-gap results, OCFO agreed to a “go” decision. • Received and installed the BNL budget system in the LBNL environment. • Have begun analysis of the system’s funds management processes and data architecture. • Completed an initial prioritization of the funds management reporting needs. • Have begun detailed analyses of the highest priority funds management reports.

Funding Chart of Accounts • Fund Type – identifies the Congressional appropriation. • B&R Classification – identifies the DOE program funding source. • Budget Reference Number – identifies the “color of money”. • BRN Sub – additional detail for capital funds. • Program Task Number – identifies funds in the ES&H five-year plan. • Reimbursable Work Order Number – assigned for tracking Work For Others activities. • Institutional Budget Activity Number – (proposed); to be assigned for tracking LBNL overhead funded activities.

Funding – DOE Projects • Fund Type – identifies the Congressional appropriation. • B&R Classification – identifies the DOE program funding source. • Budget Reference Number – identifies the “color of money”. • BRN Sub – additional detail for capital funds. • Program Task Number – identifies funds in the ES&H five-year plan. • Reimbursable Work Order Number – not used. • Institutional Budget Activity Number – not used.

Funding – Sponsored Projects • Fund Type – values ‘1Y’, ‘2Y’, ‘3T’, ‘3Y’. • B&R Classification – Codes begin with ’40’, ’60’, and ’65’. • Budget Reference Number – not used. • BRN Sub – not used. • Program Task Number – not used. • Reimbursable Work Order Number – assigned for tracking Work For Others activities. • Institutional Budget Activity Number – not used.

Funding – Overhead Projects • Fund Type – always ‘WA’. • B&R Classification – always ‘YN0100000’. • Budget Reference Number – not used. • BRN Sub – not used. • Program Task Number – not used. • Reimbursable Work Order Number – not used. • Institutional Budget Activity Number – (proposed); to be assigned for tracking LBNL overhead funded activities.

Currently Available Budgeting Information • PC: Planned (Forecast) Costs -- via Janus • AC: Actual Costs

New Funding Information • PC: Planned (Forecast) Costs -- via Janus • AC: Actual Costs • PF: Planned (Forecast) Funds or Revenue • AF: Actual Funds or Revenue

Currently Available Analysis • PC vs. AC: Is our spending consistent with our plan?

New Analytical Capabilities • PC vs. AC: Is our spending consistent with our plan? • AF vs. AC: Is our spending within our available funding? Are we breaking the law? • PF vs. AC: Is our spending within our planned funding? • AF vs. PC: Is our planned spending within our available funds? • PF vs. PC: Is our planned spending within our planned funding? • PF vs. AF: Has the funding been made available by the DOE? What planned funding has not come in yet?

Communication • The Budget System Assessment process involved over 50 participants from every Division and major operational Department. • The Budget System Evaluation process (including the requirements analysis and fit-gap) included six Division representatives. Working teams will continue to have cross-functional representation. • Division participation will be vital to this project’s success. We plan to engage each Division and operational Department directly at both the executive and end-user level. • In addition, we will reach out to the Laboratory’s administrative and business channels, including the Division Business Managers, Finance Network, etc.

Some Challenges • Sufficient technical, functional, and Division staff must be available to participate. • This system’s implementation will require changes to Laboratory business practices, including new kinds of systematic and procedural collaboration between the Divisions and the central Budget Office. • Laboratory participants must be willing to invest in changes to their local budgeting practices that will lead to a common benefit for the entire Laboratory.

Collaborative Implementation Activities • Ongoing two-way communication with the Laboratory’s business units. • Detailed design of screens and reports. • Reengineering of institutional processes and information flows. • End-user acceptance testing. • Training.

How You Can Help • Contribute your knowledge of budgeting at Berkeley Lab. • Represent your local business needs. • Take an institutional view. • Work toward the best possible and most cost-effective solution. • Provide a communication channel between the project and your Division or operational department. • Help to make the project a success.