Download

1 / 24

240 likes | 258 Views

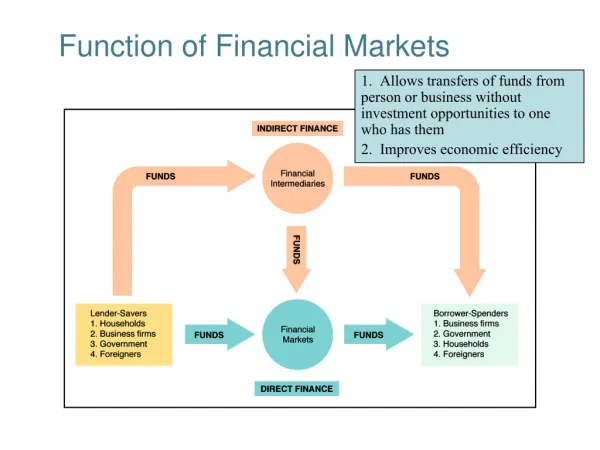

This paper explores the use of indirect estimation methods for determining the parameters of agent-based models in financial markets. It discusses the assumptions and rational behavior of agents, efficient market hypothesis, and introduces agent-based models with heterogeneity and limited rational behavior. The paper then presents the characteristics of the DM/US-$ exchange rate and discusses the Kirman (1990) model. The advantages of fundamentalist/chartist agents are discussed, followed by a simulation and Monte Carlo analysis. The paper concludes that agent-based models can replicate empirical data and suggests further improvements in parameter estimation.

E N D

Indirect Estimation of the Parameters of Agent Based Models of Financial Markets Peter Winker Manfred Gilli

Outline • Background Information. • Introduction. • Method. • Result. • Conclusion of the Paper. • Further Improvement.

Standard Models • Assumptions • Agents are fully rational. • Markets are efficient.

Rational Behaviour • Agent is rational if • He is aware of his alternatives. • Form expectations about any unknowns. • Has clear preferences. • Chooses his action deliberately after some process of optimization. • Taking into account their knowledge or expectations of other decision makers’ behaviour.

Efficient Market Hypothesis • All market participants receive and act on all relevant information as soon as it is available. • Perfect information within the market. • Cannot “beat the market”.

Agent Based Models • Agents to be heterogenous. • Agents with limited rational behaviour. • Market does not need to be efficient. • Interaction between agents.

Parameters • Not directly observable. • Compare with empirical data. • DM/US-$ exchange rate.

Characteristic of DM/US-$ Daily Returns DM/US-$

Characteristic of DM/US-$ • Excess kurtosis. • Volatility varies over time. • AR(1) process with ARCH(1) effect. • where

Model (Kirman 1990) • Two prevalent views of the world. • Each agent holds one view. • N agents. • State: number of agents, k, for first view. • Two agents, A and B, meet at random. • P(A’s view → B’s view) = . • P(A changed his view independently) = .

Model (Kirman 1990) • If , large shares of first type of agents and second type of agents, respectively, with high probability.

Fundamentalist / Chartists • There are two types of agents: • Fundamentalist: • Chartist:

Advantages • Complicated non-stationary dynamics. • Non-fundamentalist behaviour.

Simulation • Objective function. • estimated ARCH(1)-effect. • empirical kurtosis. • and mean values from 1000 simulations. • First and last 10% results deleted.

Monte Carlo Simulation 200 Monte Carlo simulation

Monte Carlo Simulation 10000 Monte Carlo simulation

Monte Carlo Simulation 10000 Monte Carlo simulation

Threshold Accepting • Initial: Choose threshold sequence , set and generate an initial . • Step 1: Choose some . • Step 2: Calculate . • Step 3: If , set . • Step 4: If , set and go to 1. Otherwise, output .

Result • Optimal values are and • , market is better characterized by switching moods of the investors than by assuming that the mix of fundamentalists and chartists remains rather stable over time.

Conclusion • Agent based models can replicate empirical data of the financial markets. • Parameters may be difficult to estimate. • Indirect method can be used. • Optimization heuristic may need to be used.

Further Improvement • First and last 10% simulation results removed. Too much? • Number of parameters to be estimated. • Only two types of agents?

Reference • Fama, E.F. 1970, “Efficient capital markets: a review of theory and empirical work”, Journal of Finance, V25, Issue 2, p383-417. • Gilli, M., Winker, P. 2003, “A global optimization heuristic for estimating agent based models”, Computational Statistics & Data Analysis, 42, p299-312. • Kirman, A. 1990, “Epidemics of opinion and speculative bubbles in financial markets”, in Taylor M.P.(eds), Money and financial markets, Basil Blackwell Ltd, Oxford, p354-368. • Tsay, R.S. 2002, Analysis of financial time series, John Wiley & Sons, Inc. • Winker, P. 2001, “Application of the optimization heuristic threshold accepting in statistics”.