Download

1 / 8

80 likes | 82 Views

Jehan Divecha - Do you want to be a millionaire someday, or are you just trying to save for the future? In either case, having a plan in place is critical if you want to meet your financial objectives. In this blog, Jehan Divecha helps you to understand what makes our financial goals SMART and how it can help you achieve success with your finances.

E N D

Jehan Divecha - Do you want to be a millionaire someday, or are you just trying to save for the future? In either case, having a plan in place is critical if you want to meet your financial objectives. In this blog, Jehan Divecha helps you to understand what makes our financial goals SMART and how it can help you achieve success with your finances.

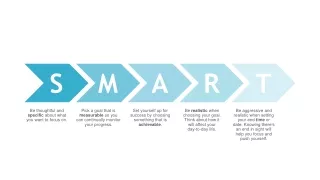

What are SMART Goals? According to Jehan Divecha, SMART Goals are a way to keep your goals focused and measurable. SMART Goals are Specific, Measurable, Attainable, Realistic, and Time-based.

When you use the SMART framework to set a goal, you increase your chances of success because you took the time to properly define it. A specific goal is one that is well- defined and clear. It answers the question of what you want to accomplish. A measurable goal is one that can be quantified so that your progress can be tracked. This could involve setting a target amount of money to save or investing a certain percentage of your income each month. A realistic goal is one that you can achieve given your current circumstances. This includes factors such as your income, debts, and other financial obligations. A realistic goal is one that you can achieve within the timeframe that you have set. This means setting a timeline for your goal and making sure that it is achievable within that time frame.A time-bound goal is one with a set deadline. This creates a sense of urgency and keeps you motivated to achieve your goal.

How to Set SMART Financial Goals Jehan Divecha says, When it comes to setting financial goals, it is important to make sure that they are specific, measurable, achievable, realistic and time-bound (SMART). This will help you to create a clear plan of action and increase the likelihood of achieving your goals.

1. Specific: Be as specific as possible when setting your goals. What exactly do you want to achieve? How much money do you want to save? What are your investment objectives? 2. Measurable: A measurable goal is one that can be measured and compared over time. This helps you keep track of where your progress is at the end of each period in achieving the goal. 3. Achievable: While it is important to set ambitious goals, make sure that they are achievable. There is no point in setting a goal that is impossible to reach. 4. Realistic: When setting a goal, consider the steps you intend to take to achieve it. Consider whether those steps are feasible in light of your current situation. Setting unattainable goals usually results in disappointment and surrender. 5. Time-bound: Set a timeframe for each goal so that you can keep yourself on track.

Tips for Sticking with Your SMART Financial Goals When it comes to financial goals, it is critical that they are SMART. SMART goals are those that are specific, measurable, attainable, realistic, and time-bound. This means that your goals should be specific, so that you know exactly what you are working towards; measurable, so that you can track your progress; attainable, so that you can actually achieve them; realistic, so that they are achievable within the timeframe that you have set; and time-bound towards.

1. Set a specific goal. This might be saving up for a down payment on a house or eliminating debt. Whatever it is, make sure it is something that you can realistically achieve. 2. Make a plan. Once you have set your goal, figure out how much you need to save each month or how much extra you need to pay towards your debt in order to achieve timeframe you have set. 3. Stay motivated. One of the most important things you can do to stick to your financial goals is stay motivated. It can be easy to get discouraged when things don't go as planned, but it's important to remember that you're on a journey and it will be perfect. Jehan Divecha has provided an effective framework for setting our financial goals, By using the SMART Goals. A good financial goal should be specific, measurable, attainable, relevant and timely in order to maximize success. These SMART Goals help to set your finances.