Download

1 / 19

190 likes | 381 Views

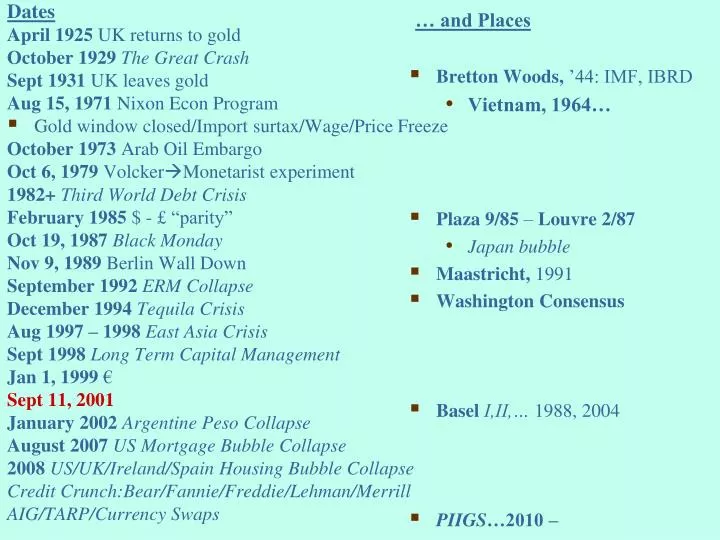

Dates April 1925 UK returns to gold October 1929 The Great Crash Sept 1931 UK leaves gold Aug 15, 1971 Nixon Econ Program Gold window closed/Import surtax/Wage/Price Freeze October 1973 Arab Oil Embargo Oct 6, 1979 Volcker Monetarist experiment 1982+ Third World Debt Crisis

E N D

Dates April 1925 UK returns to gold October 1929The Great Crash Sept 1931 UK leaves gold Aug 15, 1971 Nixon Econ Program Gold window closed/Import surtax/Wage/Price Freeze October 1973 Arab Oil Embargo Oct 6, 1979 VolckerMonetarist experiment 1982+Third World Debt Crisis February 1985 $ - £ “parity” Oct 19, 1987Black Monday Nov 9, 1989 Berlin Wall Down September 1992ERM Collapse December 1994Tequila Crisis Aug 1997 – 1998East Asia Crisis Sept 1998Long Term Capital Management Jan 1, 1999 € Sept 11, 2001 January 2002Argentine Peso Collapse August 2007 US Mortgage Bubble Collapse 2008 US/UK/Ireland/Spain Housing Bubble Collapse Credit Crunch:Bear/Fannie/Freddie/Lehman/Merrill AIG/TARP/Currency Swaps … and Places Bretton Woods, ’44: IMF, IBRD Vietnam, 1964… Plaza 9/85 – Louvre 2/87 Japan bubble Maastricht, 1991 Washington Consensus BaselI,II,… 1988, 2004 PIIGS…2010 –

Expenditure by domestic individuals and institutions The National Income Accounts • Gross national product (GNP) • The market value of all final goods and services produced by a country’s factors of production in a year, whether in the country or abroad. Y = C + I + G + EX – IM Y = C + I + G + CA

National Income Accounting for an Open Economy • Consumption (C) = 70.6 % of 2010 GDP • The portion of GNP purchased by the private sector to fulfill current wants • Investment (I) = 12.0 % of 2010 GDP • The part of output used by private firms to produce future output • Government Purchases (G) = 20.5 % of 2010 GDP • Any goods and services purchased by federal, state, or local governments • Current Account (CA = “EX – IM”) = 12.5 – 16.1 = - 3.6 % • Goods and services, including factor service, purchased by foreigners net of foreign g&s purchased by residents

U.S. GNP and Its Components Source: U.S. Department of Commerce, Bureau of Economic Analysis.

The National Income Accounts • Gross Domestic Product (GDP) measures the volume of production within a country’s borders. • GDP equals GNP minus net factor income from the rest of the world. Income earned from production abroad doesn’t count in gross domestic product. GDP = GNP – Income earned abroad • National Income • Earned over a period by a nation’s factors of production. • NI = GNP – Depreciation – IBT + Unilateral Transfers For purposes of macro analysis, GNP = Y = NI

The Current Account and Foreign Indebtedness • Current account (CA) balance: CA = EX – IM • CA measures the size and direction of international lending. • If we import more than we export (CA<0), we must pay for the difference by borrowing from foreigners. • CA equals the change in a country’s net foreign wealth. • CA balance is equal to the difference between national income and domestic residents’ spending or absorption: • Y – (C+ I + G) = CA • CA balance is what we produce (Y) less domestic demand. • We can live “beyond our means” if we run a current account deficit, import more than we export, and borrow the difference from foreigners. • CA balance is the excess supply of domestic financing. • If we produce and earn more than domestic demand (CA>0), we lend our “excess” saving to foreigners

U.S. Current Account and Net Foreign Wealth, 1976–2009 Source: U.S. Department of Commerce, Bureau of Economic Analysis.

Saving and the Current Account • National saving (S) : The portion of output, Y, that is not devoted to household consumption, C, or government purchases, G. S = I in a closed economy. • A closed economy can save only by building up its capital stock • An open economy can save either by building up its capital stock or by acquiring foreign wealth S = I + CA • A country’s CA surplus is its net foreign investment: CA = NFI = Capital Outflows - CA = Capital Inflows

International Monetary Arithmetic Sources of Income = Uses of Income C + I + G + CA = T + Sp + C I = Sp + (T – G) – CA = Nat’l Saving+Capital Inflows • Domestic investment is financed by our own saving plus our net “borrowing” from foreigners Nat’l Borrowing = - CA = (I - Sp) + (G – T) The Twin Deficits • Private Saving (Sp) and Government Saving (Sg) • Sp= Y – T – C = I + CA – (T – G) = I + CA – Sg Sp= I + CA + (G – T) Private saving finances domestic investment, net foreign investment, and the government’s deficit

The Balance of Payments Accounts • Three types of international transactions • Payments for exports or imports of goods or services, including factor services Current Account • Purchases or sales of financialassets Financial Account • Transfers of wealth between countries • Capital Account • The Fundamental Balance of Payments Identity Current account + financial account + capital account = 0

U.S. Balance of Payments Accounts for 2006 (billions of dollars)

U.S. Balance of Payments Accounts for 2006 (billions of dollars, cont.)

Financial account has at least 3 subcategories: • Official (international) reserve assets • Foreign assets are held by central banks as a cushion against national economic misfortune. • Central banks often buy or sell international reserves in private asset markets to affect macroeconomic conditions in their economies. • Official reserve assets include government bonds, currency, gold and accounts at the International Monetary Fund. • All other assets • Statistical discrepancy…so the balance balances • The (negative) value of official reserve asset change is called the official settlements balance or “balance of payments.” A country with a negative balance of payments is running down its reserve assets or incurring debts to foreign monetary authorities. • In 2009, the Fed & Treasury increased their holdings of foreign assets by $52.3 billion and foreign central banks and government agencies increased their holdings of US assets by $450.0 billion. The $397.7 net inflow US “Balance of Payments” Deficit = $397.7 billion

U.S. Current Account and Net Foreign Wealth, 1976–2009 Source: U.S. Department of Commerce, Bureau of Economic Analysis.

U.S. Gross Foreign Assets and Liabilities, 1976-2009 Source: U.S. Department of Commerce, Bureau of Economic Analysis, June 2010.

International Investment Position of the United States at Year End, 2005 and 2006 (millions of dollars)

International Investment Position of the United States at Year End, 2005 and 2006 (millions of dollars)

Problems, Chapter 13 • Why might a government be concerned about a large CA deficit or surplus? Why might it be concerned about a large surplus or deficit in its official settlements account (i.e., its “balance of payments”)? • Can a country have a CA deficit at the same time it has a BoP surplus? Explain using hypothetical figures for the CA and the nonreserve financial account. Discuss implications for official international reserve flows. • In 2006, US income receipts on foreign assets were $647.6 billion while payments on liabilities (foreign owned assets in the US) were $604.4 billion. Yet the US is a substantial net debtor to foreigners. How then is it possible that the US received more foreign income than it paid out?