Download

1 / 15

150 likes | 153 Views

Discover the benefits of SEPA, the Single Euro Payments Area, which aims to create a common payments landscape in Europe, simplifying payments and card transactions.

E N D

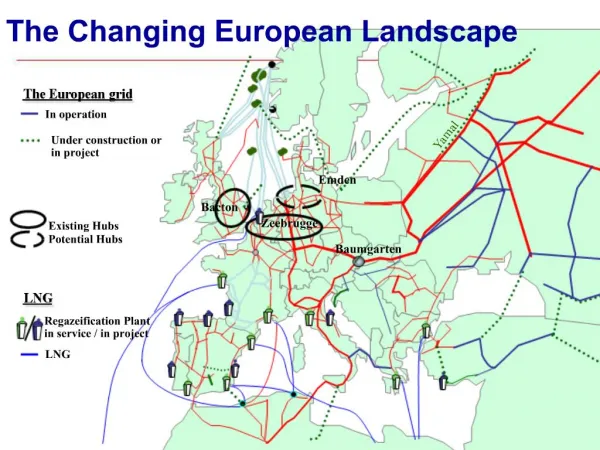

A common European payments landscape SEPASingle Euro Payments Area

What is SEPA? • Stands for a Single Euro Payments Area • Is about simple and efficient payments and card transactions • Will bring advantages to our customers, when they use their card in Europe as well as when they send or receive a payment.

A common payments landscape in Europe • Common schemes and transfer systems • The same instruments, terms and routes for Europe cross border and domestic euro transfers • Benefits for society as whole: • frees-up capital • reduces paper payments • reduces cash handling costs • A politically supported initiative 3

A fragmented payments landscape today • More than 27 different national payment infrastructures in Europe • Separate solutions for high and low value payments • Separate solutions for domestic card systems • Banks maintain different systems for domestic and cross border transfers Which implies: • Potential for rationalization • Possibility for customers to reduce number of accounts

13 EMU 14 remaining EU3 EEA + CH SEPA embraces more than the euro countries 5 5 5

Part of the vision of an internal market • Will increase cross-border mobility for goods, services, people and capital • Will serve as a catalyst formarket integration and increased competitiveness • Part of the European plan for a common market for financial services 6

SEPA – a multi year transformation SEPA Compliant Cards 1. Development phase 2. Migration 3. Phase-out 2007 2008 2009 2010 2011 SEPA Payment SEPA Direct Debit Harmonized legal framework 7 7 7

The future standard payment in Europe SEPA Payment: • European launch January 28, 2008 • Same conditions for domestic and cross border transfers • No amount limitations • IBAN and BIC are mandatory • More information can be sent with each payment (up to 140 characters) • Replaces current EU Regulated Payment

New technology for cards, ATMs and POS terminals Within the SEPA area: • EMV-chip on general purpose cards (VISA, MasterCard/Maestro) in place 2008–2011 • Cardholder should be able to use their chip cards in ATMs and POS terminals from January 1, 2008 • PIN (on the terminal side) should be in place before 2011 • No domestic card schemes designed only for use in a single country may exist after end of 2010

A Direct Debit with pan-European reach • European launch 2009 • For recurrent payments, e.g. electricity or rent • IBAN and BIC mandatory • The beneficiary is ensured a receipt within 3 days. • The payer does not need to keep track of payment days. • Easier for companies to forecast liquidity and less work with reminders and collections

Harmonized legal framework • Payment Services Directive, legal framework for payments in Europe • Implemented in national law by November 2009 • Stipulates customer rights and banks obligations • Increases requirements for transparency of conditions and information • Applies to • all EU currencies and countries • existing and new payment instruments including cards • domestic and cross-border payments within the EU 11

Moving To a Single Account for SEPA • Pay and receive to a single account • Better liquidity control • Fewer bank relations • Standard reconciliation procedures • Obstacles: • Tax reporting and tax payment and redemption requirements • Securities/Asset servicing requirements • National billing conventions & routines • Other local legal requirements 12

We bring our customers the benefits of SEPA We participate in building SEPA We realised early on that a common payments landscape would bring advantages to our our customers, but also for society as whole. That is why we are a part of building the SEPA, and have been from start. ”With SEPA inside” SEB’s offering and development of accounts, payment and card services will continuously be made SEPA ‘proof’. Where and when our customers need SEPA SEPA affects the cash flow structures of a growing number of companies, institutions, authorities and consumers. We have carefully looked at all these needs when designing the payment products, access means and the timing of launches to bring the benefits of SEPA to our customers, where and when they need them.

SEPA value for corporates • Euro payments are easier and more efficient as the cross border payments • More efficient business transactions within Europe • Increased competitiveness • Less need for collection accounts • Business cards for employees with a higher service level and increased accessibility within SEPA • Increased liquidity and better cash flow • Reduction of manual services (increased STP level) 14

Thank you for listening! Additional information: www.seb.ee cmsupport@seb.ee nostro@seb.ee