Download

1 / 0

0 likes | 241 Views

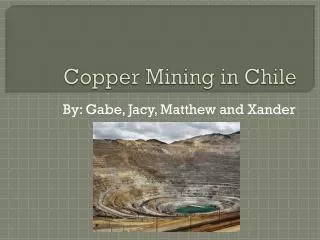

Mining in Chile. Latam is a major supplier of metals worldwide. Chile accounts for: 33 % of world Copper Production, and +30%of world copper reserves. # 1 world producer of molybdenus , Lodine , Lithium, and natural nitrates; 15 % of gold and 3% of silver . Chilean Market.

E N D