Download

1 / 15

150 likes | 429 Views

Pricing Concepts. Chapters 13. Price and Value. Value = perceived benefits/price Price = perception of quality Price = consumer perception of prestige Example : Swiss firm TAG HEUER Changed prices from $250 to $1000 Sales volume increased sevenfold. Step 1: Pricing Objectives. Survival

E N D

Pricing Concepts Chapters 13

Price and Value • Value = perceived benefits/price • Price = perception of quality • Price = consumer perception of prestige • Example: • Swiss firm TAG HEUER • Changed prices from $250 to $1000 • Sales volume increased sevenfold

Step 1: Pricing Objectives • Survival • Maximum current profit/profit oriented pricing • Maximum market share/sales oriented pricing • Maximum market skimming • Product quality leadership

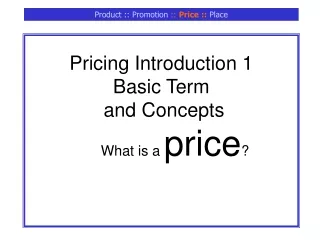

S 2.50 Surplus D 2.00 PriceEquilibrium Price 1.50 1.00 Shortage S D .50 0 20 40 60 80 100 120 Quantity demanded Step 2: Determining Demand

Price Goes... Revenue Goes... Demand is... Down Up Elastic Down Down Inelastic Up Up Inelastic Up Down Elastic Up or Down Stays the Same Unitary Elasticity Elasticity of DemandConsumers sensitivity to price changes

Factors that Affect Elasticity • DEMAND LESS ELASTIC IF: • Few or no substitutes • Buyers don’t notice higher price • Buyers are slow to change habits • Buyers think higher prices are justified

Step 3: Estimating Cost • Variable costs – changes with level of output • Fixed costs – no change with output level • Marginal costs – the change in total costs associated with a 1 unit change in output • Average variable costs – total variable costs divided by quantity of output • Average total costs – total costs divided by quantity of output

Step 4: Analyzing Competition • Analyze competitors costs, prices and offers

Step 5: Methods of Setting Prices • Markup pricing • Keystoning • Target return pricing • Perceived value pricing • Value pricing • Going Rate pricing • Auction type pricing • Group pricing

Step 6: Selecting Final Price • Psychological pricing • Marketing mix • Company policies

Fine Tuning the Base Price • Geographical pricing • Quantity discounts • Cash discounts • Functional discounts • Seasonal discounts • Promotional discounts • Rebates

Single-Price Tactic All goods offered at the same price Flexible Pricing Different customers pay different price Professional Services Pricing Used by professionals with experience, training or certification Price Lining Several line items at specific price points Leader Pricing Sell product at near or below cost Bait Pricing Lure customers through false or misleading price advertising Odd-Even Pricing Odd-number prices imply bargain Even-number prices imply quality Price Bundling Combining two or more products in a single package Two-Part Pricing Two separate charges to consume a single good Special Pricing Tactics