Download

1 / 67

670 likes | 754 Views

CHAPTER 7 Time Value of Money. Future value Present value Rates of return Amortization. Time lines show timing of cash flows. 0. 1. 2. 3. i%. CF 0. CF 1. CF 2. CF 3. Tick marks at ends of periods, so Time 0 is today; Time 1 is the end of Period 1; or the beginning of Period 2.

E N D

CHAPTER 7Time Value of Money • Future value • Present value • Rates of return • Amortization

Time lines show timing of cash flows. 0 1 2 3 i% CF0 CF1 CF2 CF3 Tick marksat ends of periods, so Time 0 is today; Time 1 is the end of Period 1; or the beginning of Period 2.

Time line for a $100 lump sum due at the end of Year 2. 0 1 2 Year i% 100

Time line for an ordinary annuity of $100 for 3 years. 0 1 2 3 i% 100 100 100

Time line for uneven CFs -$50 at t = 0 and $100, $75, and $50 at the end of Years 1 through 3. 0 1 2 3 i% -50 100 75 50

What’s the FV of an initial $100 after 3 years if i = 10%? 0 1 2 3 10% 100 FV = ? Finding FVs is compounding.

After 1 year: FV1 = PV + INT1 = PV + PV(i) = PV(1 + i) = $100(1.10) = $110.00. After 2 years: FV2 = PV(1 + i)2 = $100(1.10)2 = $121.00.

After 3 years: FV3 = PV(1 + i)3 = $100(1.10)3 = $133.10. In general, FVn = PV(1 + i)n.

Four Ways to Find FVs • Solve the equation with a regular calculator. • Use tables. • Use a financial calculator. • Use a spreadsheet.

Algebraic Solution FVn = PV(1 + i)n. FV3 = 100(1 + .10) 3 FV3 = 100(1.331) = 133.10

Solution Using Tables FVn = PV(FVIF i,n). FV3 = 100(FVIF 10%, 3) Use FVIF table from pages A-6 & 7, Table A3 FV3 = 100(1.331) = 133.10

Financial Calculator Solution Financial calculators solve this equation: There are 4 variables. If 3 are known, the calculator will solve for the 4th. FVn = PV(1 + i)n.

Here’s the setup to find FV: INPUTS 3 10 -100 0 N I/YR PV PMT FV 133.10 OUTPUT Clearing automatically sets everything to 0, but for safety enter PMT = 0. Set: P/YR = 1, END

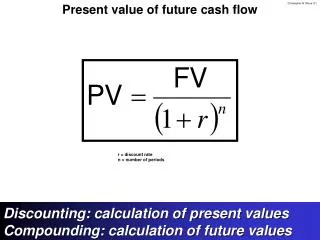

What’s the PV of $100 due in 3 years if i = 10%? Finding PVs is discounting, and it’s the reverse of compounding. 0 1 2 3 10% 100 PV = ?

( ) 1 1 + i FVn (1 + i)n PV = = FVn . ( ) 1 1.10 Solve FVn = PV(1 + i )n for PV: n PV = $100 = $100(PVIFi,n) Table A1 = $100(0.7513) = $75.13. So the (PVIF 10%,3) = .7513 3

Financial Calculator Solution INPUTS 3 10 0 100 N I/YR PV PMT FV -75.13 OUTPUT Either PV or FV must be negative. Here PV = -75.13. Put in $75.13 today, take out $100 after 3 years.

If sales grow at 20% per year, how long before sales double? Solve for n: FVn = $1(1 + i)n; $2 = $1(1.20)n ln 2 = ln 1.2n .693147=.18232n 3.801 = n Use calculator to solve, see next slide.

If sales grow at 20% per year, how long before sales double? Solve for n: FVn = PV(FVIF i,n); $2 = $1(FVIF 20,n) 2.00 = (FVIF 20,n) n between 3 and 4 years 1.728 and 2.0736 Use calculator to solve, see next slide.

INPUTS 20 -1 0 2 N I/YR PV PMT FV 3.8 OUTPUT Graphical Illustration: FV 2 3.8 1 Year 0 1 2 3 4

Compound GrowthHow do you find the compound growth rate for your company to analyze sales growth ? Can use either PV or FV formula, use FV 1062021 (1 + i )9 = 5284371 (1 + i )9 = 5284371/1062021 (1 + i)9 = 4.976 (1 + i) = 4.976 .111 (1 + i) = 1.195 i = .195 or 19.5%

Tabular Solution Use PV formula and table A-1 5284371 (PVIF i,9) = 1062021 PVIF i,9 = 1062021/5284371 PVIF i,9 = .20097 Use table A-3, for 9 Periods, find .20097 i is between 18% and 20%

Calculator Solution, Compound Growth INPUTS 9 -1062021 0 5284371 N I/YR PV PMT FV 19.51 OUTPUT

What’s the difference between an ordinaryannuity and an annuitydue? Ordinary Annuity 0 1 2 3 i% PMT PMT PMT Annuity Due 0 1 2 3 i% PMT PMT PMT

What’s the FV of a 3-year ordinary annuity of $100 at 10%? 0 1 2 3 10% 100 100 100 110 121 FV = 331

Algebraic Solution FVA =( PMT)* ( 1 +i)n – 1 I FVA =( 100)* ( 1 + .1)3 – 1 .1 FVA =( 100)* 1.331 – 1 = 100 * 3.31 = .1 FVA = 331.00

Tabular Solution FVA i,n =( PMT) * (FVIFA i,n ) Use Table A-4 on pages A-8 & 9 FVA 10%,3 =( 100) * (FVIFA 10%,3) FVA 10%,3 =( 100)* 3.31 = FVA 10%,3 = 331.00

Financial Calculator Solution INPUTS 3 10 0 -100 331.00 N I/YR PV PMT FV OUTPUT Have payments but no lump sum PV, so enter 0 for present value.

What’s the PV of this ordinary annuity? 0 1 2 3 10% 100 100 100 90.91 82.64 75.13 248.68 = PV

Algebraic Solution 1 . PVA =( PMT)* 1 – (1 + i)n i 1 . PVA =( 100) * 1 – (1 + .1)3 .1 PVA =( 100)* 1 - .7513 = 100 * 2.48685 = .1 PVA = 248.69

Tabular Solution PVA i,n =( PMT) * (PVIFA i,n ) Use Table A-2 on pages A-4 & 5 PVA 10%,3 =( 100) * (PVIFA 10%,3) PVA 10%,3 =( 100)* 2.4869 = PVA 10%,3 = 248.69

INPUTS 3 10 100 0 N I/YR PV PMT FV OUTPUT -248.69 Have payments but no lump sum FV, so enter 0 for future value.

Find the FV and PV if theannuity were an annuity due. 0 1 2 3 10% 100 100 100 Easiest way, multiply results by (1 + i).

Algebraic Solution 1 . PVAD i,n =( PMT)* 1 – (1 + i)n * (1 + i) i 1 . PVAD 10%,3 =( 100) * 1 – (1 + .1)3 * (1 + .1) .1 PVAD 10%,3 =( 100)* 1 - .7513 * (1.1) = .1 100 * 2.48685 * (1.1)= PVAD 10%,3 = 273.55

Tabular Solution PVAD i,n =( PMT) * (PVIFA i,n )* (1 + i) Use Table A-2 on pages A-4 & 5 PVAD10%,3 =( 100) * (PVIFA 10%,3) * (1 + i) PVAD 10%,3 =( 100)* 2.4869 * 1.1 = PVAD 10%,3 = 273.55

Switch from “End” to “Begin.” Then enter variables to find PVA3 = $273.55. INPUTS 3 10 100 0 -273.55 N I/YR PV PMT FV OUTPUT Then enter PV = 0 and press FV to find FV = $364.10.

What is the PV of this uneven cashflow stream? 4 0 1 2 3 10% 100 300 300 -50 90.91 247.93 225.39 -34.15 530.08 = PV

Input in “CFLO” register: CF0 = 0 CF1 = 100 CF2 = 300 CF3 = 300 CF4 = -50 • Enter I = 10, then press NPV button to get NPV = $530.09. (Here NPV = PV.)

The Power of Compound Interest A 20-year old student wants to start saving for retirement. She plans to save $3 a day. Every day, she puts $3 in her drawer. At the end of the year, she invests the accumulated savings ($1,095) in an online stock account. The stock account has an expected annual return of 12%.

How much money by the age of 65? 45 12 0 -1095 1,487,261.89 INPUTS N I/YR PV PMT FV OUTPUT If she begins saving today, and sticks to her plan, she will have $1,487,261.89 by the age of 65.

How much would a 40-year old investor accumulate by this method? 25 12 0 -1095 146,000.59 INPUTS N I/YR PV PMT FV OUTPUT Waiting until 40, the investor will only have $146,000.59, which is over $1.3 million less than if saving began at 20. So it pays to get started early.

How much would the 40-year old investor need to save to accumulate as much as the 20-year old? 25 12 0 1487261.89 -11,154.42 INPUTS N I/YR PV PMT FV OUTPUT The 40-year old investor would have to save $11,154.42 every year, or $30.56 per day to have as much as the investor beginning at the age of 20.

Will the FV of a lump sum be larger or smaller if we compound more often, holding the stated I% constant? Why? LARGER! If compounding is more frequent than once a year--for example, semiannually, quarterly, or daily--interest is earned on interest more often.

Rules for Non-annual Compounding 95% of the time, the method for adjusting for non-annual compounding is: Divide i by m, m being the # of compounding periods in a year. Multiply n by m

FV of $100 after 3 years under 10% semiannual compounding? Quarterly? m*n i æ ö Nom FV = PV 1 . + ç ÷ è ø n m 2*3 0.10 æ ö FV = $100 1 + ç ÷ è ø 3S 2 = $100(1.05)6 = $134.01. FV3Q = $100(1.025)12 = $134.49.

0 1 2 3 10% 100 133.10 Annually: FV3 = $100(1.10)3 = $133.10. 0 1 2 3 4 5 6 0 1 2 3 5% 100 134.01 Semiannually: FV6 = $100(1.05)6 = $134.01.

Exam Question (Example) Your uncle has given you a choice between receiving $20,000 today on your 18th birthday, or waiting until your 25th birthday and receiving $40,000. If you would invest in a junk bond fund if you took the $20,000, expecting to average 10% per year, compounded semiannually, which would you prefer?

Exam Question (Example) See board for timeline. Algebraic solution: FV = PV(1 + i/m)n*m FV = 20,000 (1 + .1/2)7 * 2 FV = 20,000 ( 1.9799) = 39,598.63 Prefer the $40,000 in 7 years.

Exam Question (Example) Tabular solution: PV = FV(PVIF i/2,n*2) PV = 40,000 (PVIF 10/2,7*2) Table A-1 PV = 40,000 ( .505) = 20,202 Prefer the $40,000 in 7 years (same conclusion.

Financial Calculator Solution 14 10 ? 0 40,000 -20,202.72 INPUTS N I/YR PV PMT FV OUTPUT Could have solved for FV inputting PV calcuation: P/Y set to 2

We will deal with 3 different rates: iNom = nominal, or stated, or quoted, rate per year. iPer = periodic rate. EAR = EFF% = . effective annual rate