Download

1 / 25

250 likes | 292 Views

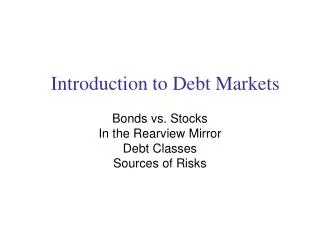

Introduction to Debt Markets. Bonds vs. Stocks In the Rearview Mirror Sources of Risks Debt Classes. Bonds vs. Stocks. Sizing Bond (2009) and Stock Markets (Q3 2008). $34.3 T. $14.1 T. Rearview Mirror. Rearview Mirror. Why Bonds?. Bonds form an important asset class

E N D

Introduction to Debt Markets Bonds vs. Stocks In the Rearview Mirror Sources of Risks Debt Classes

Bonds vs. Stocks • Sizing Bond (2009) and Stock Markets (Q3 2008) $34.3 T $14.1 T

Why Bonds? • Bonds form an important asset class • Sources of risk and return in bonds • Interest rate risk • Reinvestment risk • Default risk • When liabilities are fixed in nominal terms, investing in suitably chosen bond portfolios may lead to lower risk • May not be necessary to consider all asset classes and use mean variance optimization methods • Bond mispricing may arbitrage opportunities for an active portfolio manager

Issuers of Bonds • U.S. Treasury • Notes and Bonds • Municipalities • Tax-Exempt Bonds • Corporations • Corporate Bonds, Preferred Stock • International Governments and Corporations • Innovative Bonds • Indexed Bonds • Floaters and Reverse Floaters

Source of Risks • Interest Rate Risk (Market Risk) • The major factor affecting bond prices • The price of bond changes in the opposite direction of interest change • All bonds are exposed • Inflation Risk • Inflation reduces purchasing power • Yield changes to reflect the expected inflation • Reinvestment Risk • No guarantees that coupon payments could be reinvested at the same rate

Source of Risks • Credit Risk • Inability of issuer to pay coupon and/or principal • Corporate, Emerging market and high-yield bonds • Credit linked debt securities, credit derivatives • Liquidity Risk • Inability to unload position without substantial loss • Municipal, Corporate, and Emerging market bond • FX Risk • The risk of exchange rate fluctuation in reducing the return on a foreign bond

Debt Classes: Definition • Bond (Fixed Income Security) • A security obligating issuer to pay interest and principal to the holder on specified dates. • Coupon Interest rate, e.g. 4%, 5 3/4%, etc. • Face/par value or Principal amount, e.g. $100 MM, $3B. • Maturity, e.g. 3 month, 1 year, 30 years, etc. • Bond can be classified according to its attributes • Payment type, e.g. semi-annual coupon, amortizing, etc. • Issuer, e.g. government, agency, corporate, etc. • Maturity, e.g. short, medium, long, etc. • Security, e.g. secured, unsecured debenture, etc.

Debt Classes: Payment Type • Pure Discount or Zero-Coupon Bond • No coupon payments prior to maturity. • Bond’s face value paid at maturity. • Coupon Bond • A stated coupon paid periodically prior to maturity. • Bond’s face value paid at maturity. • Perpetual (Consol) Bond • A stated coupon paid at periodic intervals. • Self-Amortizing Bond • Certain amount paid at each payment period. • No balloon payment at maturity.

Debt Classes: U.S.Treasuries • Treasury Bills • maturity 1 year when issued • typically 3 months and 6 months • pure discount bond, no coupon • Treasury Notes • Maturity: 1 year maturity 10 years when issued • Typically, 2, 3, 5, and 10 year • Coupon: semi-annual • Treasury Bonds • Maturity: >10 years when issued • Typically, 20, 30 (last issued Feb 15, 2001) • Coupon: semi-annual

Debt Classes: U.S.Treasuries • Treasury STRIPS are zero-coupon securities that are made by “stripping” coupons or principals from Government Notes and Bonds. • Treasury Strips are issued under the U.S. Treasury STRIPS (Separate Trading of Registered Interest and Principal of Securities) program. • Prices of Notes, Bonds, and STRIPS are quoted as prices per $100 of face value. Prices of Bills are quoted in terms of rate of discount.

Debt Classes: Corporate Bonds • Secured Debt (backed by collateral assets) • Secured by real property • Property reverts to bondholder upon default • Subordinate Debenture • General creditors subordinate to secured debt • Higher priority over stockholders • Other Features of corporate bonds • Convertible bonds: convertible to equity • Callable bonds: issuer’s right to buys back bond • Putable bonds: holder’s right to sell bond to issuer • Sinking funds: reduced face amount over time

Corporate Bonds – Default Risk • One of the biggest differences between Corporate Bonds and U.S. Treasury Bonds is the default risk on corporate bonds • Corporate bonds are rated on the basis of their default risk by a few rating companies

Factors Used by Rating Companies • Coverage ratios • Leverage ratios • Liquidity ratios • Profitability ratios • Cash flow to debt • Effects of bond covenants • Moody’s acquired KMV to use option pricing theory to rate corporate bonds

Corporate Bonds – Default Ratings Rating Companies • Moody’s Investor Service • Standard & Poor’s • Fitch Rating Categories • Investment grade • Aaa, Aa, A, Baa by Moody’s ratings • AAA, AA, A, BBB by S&P ratings • Speculative grade or “Junk” bonds • Rated below Baa by Moody’s and BBB by S&P

Debt Classes: Corporate Bonds • Credit Rating

Average One-Year Credit Loss Rates Source: “Credit Derivatives” by E. Banks, P. Siegel, M. Glantz; McGraw-Hill, 2006

Ratings and Average Time to Default Source: “Credit Derivatives” by E. Banks, P. Siegel, M. Glantz; McGraw-Hill, 2006

Mean and Median Recovery Rates Source: “Credit Derivatives” by E. Banks, P. Siegel, M. Glantz; McGraw-Hill, 2006

Protection Against Default • Sinking funds • Subordination of future debt • Dividend restrictions • Collateral

Bond Provisions • Call Provision allows the issuer to repurchase the bond at a specified call price before the maturity date • Put Provision allows a bondholder to reclaim a principal, or to extend bond’s life • Convertible Provision allows a bondholder to exchange a bond for common stock • Typically are callable as well • Secured Bonds have specific collaterals for bonds • Sinking Funds guarantee gradual repurchase of corporate bonds by the issuer • Floating Rate Bonds have interest payments tied to some measure of current market rates

Debt Classes: Municipal Bonds • Municipal Bonds • Maturity varies from one month to 40 years • Exempt from federal taxes and state taxes (for residents of issuing state) • Generally two types: • Revenue bonds • backed by the revenue of a particular project • e.g. water bond • General Obligation bonds • backed by the tax revenue of local government • e.g. school bond • Riskier than U.S. Government bonds

Bond Resources • WSJ - Bonds • Yahoo – Bonds • Bloomberg - Bonds • Lehman Brothers Bond Indices (what’s left of them…) • www.investinginbonds.com • PIMCO - Everything You Need to Know About Bonds