Download

1 / 10

100 likes | 239 Views

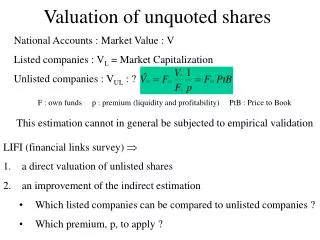

The 2008 Revision to Market Value of Quoted and Unquoted Shares of Corporate Equities in the U. S. Flow of Funds Accounts. Prepared by Susan Hume McIntosh and Elizabeth Ball Holmquist Working Party on Financial Statistics November 2, 2009 OECD, Paris. Relative Importance of Unquoted Shares.

E N D

The 2008 Revision to Market Value of Quoted and Unquoted Shares of Corporate Equities in the U. S. Flow of Funds Accounts Prepared by Susan Hume McIntosh and Elizabeth Ball Holmquist Working Party on Financial Statistics November 2, 2009 OECD, Paris

Previous Methodand the Upward Revision • Last benchmark 2000:Q4, perpetual inventory method equation using DJ Total Market Index and net equity issuance • Use Wilshire 5000, adds over $600 billion • Net change in shares outstanding • Closely held benchmarked to estate tax return data, moved by index • Shift to larger proportion of closely held shares • Upward revision of

Publicly Traded FirmsNew Method • Gross market value=share prices x shares outstanding using firm-level data from CRSP • ADRs and listed companies incorporated outside U.S. are excluded • Preferred stocks benchmarked to data from Standard and Poor’s for 2007:Q1 • Intercorporate holdings of nonfinancial companies excluded using Compustat data

Closely Held FirmsS-corpoations - 1 • For 2006, 3.8 million returns, $3.0 trillion in assets, $851 billion in net worth • 65% of market value of closely held firms • Uses aggregate net worth from IRS Statistics of Income (SOI) tax data with 2 year lag • 14 industry classifications • Average historical growth rates by industry of net worth used for most recent periods • Annual net worth converted to quarterly using linear interpolation

Closely Held FirmsS-corpoations - 2 • Calculate ratio of summed market value to summed net worth for public companies, by industry, quarterly from Compustat data • S-corps market value = S-corps net worth x market-to-net worth ratio of public companies • Sum S-corps market values of 14 industries • Latest periods use Russell 2000 index • Downward liquidity adjustment of 25%

Closely held firmsC-corporations - 1 • 35% of market value of closely held firms • List of private C-corps with revenue greater than $1 billion from Forbes • For 2008, 441 private C-corps • Information available from Forbes includes revenue, industry classification, and number of employees • Annual revenue held constant for each quarter of the year

Closely held firmsC-corporations - 2 • Match each private C-corp with a public firm that has a similar industry and revenue profile using Compustat data • Compute market value-to-revenue ratio for all comparable public companies • Market value of private C-corps = revenue of private C-corps x market-to-revenue ratio of public companies • Use DJ total market index for latest quarters • Downward liquidity adjustment of 25%