Download

1 / 12

120 likes | 236 Views

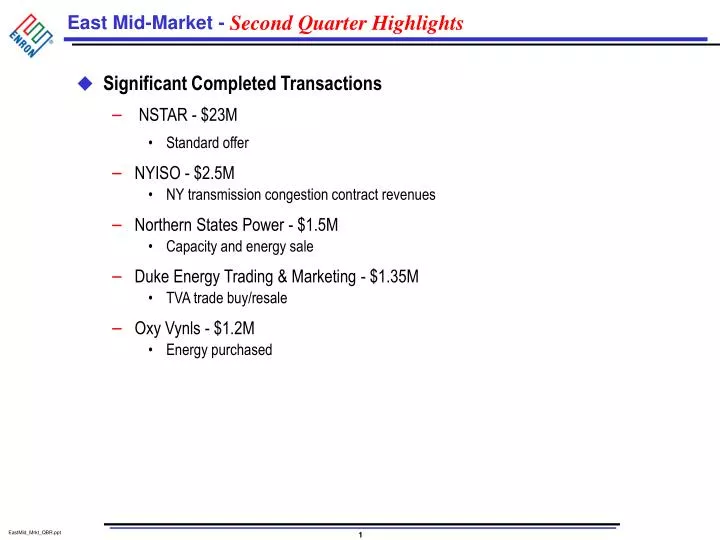

Second Quarter Highlights. Significant Completed Transactions NSTAR - $23M Standard offer NYISO - $2.5M NY transmission congestion contract revenues Northern States Power - $1.5M Capacity and energy sale Duke Energy Trading & Marketing - $1.35M TVA trade buy/resale Oxy Vynls - $1.2M

E N D

Second Quarter Highlights • Significant Completed Transactions • NSTAR - $23M • Standard offer • NYISO - $2.5M • NY transmission congestion contract revenues • Northern States Power - $1.5M • Capacity and energy sale • Duke Energy Trading & Marketing - $1.35M • TVA trade buy/resale • Oxy Vynls - $1.2M • Energy purchased

Second Quarter Highlights, cont’d. • Future Expected Transactions • New Standard Offer Agreements • NSTAR / CMP / Bangor Hydro • Outsourcing/Asset Management • ERCOT QSE business • Hoosier • Other Full Requirements • City of Columbus • Tolling (Morgan Stanley) • ERCOT Wind Agreement • OPPD Restructure

Hot List Detail Estimated Deal Originator Description Value (000’s) Enron Wind Curry Off-take Agreement $ 8,000 Manitoba Hydro Electric Board Clynes/Sewell Buy Capacity/Energy 250 QSE (EES) Curry Outsourcing 750 Morgan Stanley Swank Gas Tolling 1,500 3Q 00 Total $ 10,500 NSTAR Llodra Standard Offer Agreement $ 5,000 OPPD Clynes/Sewell Restructure Agreement 1,000 Hoosier Dalton Asset Management/Outsourcing 1,000 CMP/Bangor Hydro Wood/Llodra Standard Offer 3,500 4Q 00 Total $ 10,500 Total Deals - 8 $ 21,000

Progress Report - General Initiatives • Establish and meet 2000 budget • Objective: $25 million • YTD status: $30.6 million • Implement complete ongoing account coverage • Monthly, quarterly and annual coverage objectives implemented August 1, 2000 • Increase EOL penetration • Established top 100 customer list (created late June) • Build Deal Flow • YTD status: 26 “significant” transactions • Focus will be on significantly increasing standard product deals • Objective: Build to 150 transactions per quarter by Q1, 2001 • Implement more intensive coverage and transaction orientation throughout group

Progress Report - General Initiatives , cont’d. • Complete Mid-Market team build-out • Build-out complete: see organizational chart • Reviewing business initiatives for additional staffing needs (ERCOT/SPP) • Build strong team dynamics • Empower each team member to build the business - Mid-marketers are closest to the customer and the market • Commercial leads are taking ownership of sub-region by mentoring associates, directing regulatory coverage, focusing on complete account coverage and developing new initiatives • Cross-leveraging expertise of team (e.g., Llodra will be on team with Woody to work standard offer with Bangor Hydro and Central Maine Power - Janelle will be group model for generating deal flow) • Mid-Market will closely coordinate with Origination • Mid-Market is working on several initiatives with originators across all regions • Mid-Market and Origination held joint Northeast strategy session • Strategy sessions are to follow for Southeast and Midwest • Implement complete regulatory coverage • Commercial leads have developed coverage strategies for all key regulatory committees and initiatives (e.g., participating in and influencing development of Midwest - ISO, SPP-RTO, ERCOT-ISO and Florida RTO)

Progress Report - Specific Initiatives • Build up markets where there is currently little activity • New York - Working with trading to develop financial trading • PJM - Working to develop positions in both east and west hub (250 MW tolling with Morgan Stanley) • Florida - Working on Ft. Pierce deal: EPMI receives 170 MW call option • ERCOT - Working to close 135 MW wind position with green credits; Rolling out outsourcing (QSE) business to put Enron’s “hands” on more MW’s • Asset management/outsourcing (control/manage 2,000 MW’s) • Outsourcing (QSE) deal with EES in ERCOT - this deal would give Enron view of hourly ERCOT load • Working QSE deals with Oxychem (Gen - 700 MW; Load - 1,000 MW) and Alcoa (Gen. - 1,000 MW; Load - 700 MW) • Hoosier - Displace Williams as asset manager

Progress Report - Specific Initiatives, cont’d. • Full/Partial requirements transactions - Execute 2-3 new deals for at least 2,000 MW’s • Four year NSTAR with 3,700 MW’s peak and 2,000 MW’s of PPA’s • Bangor Hydro (320 MW’s )and Central Maine Power (1,300 MW’s) standard offer service • Cajun Coop - Four member coops are seeking full requirements supplier • Ohio municipalities - Seeking alternative supply and load management services • Transmission Initiatives • Taking positions in TCC auctions (NY-ISO) • Analyzing transmission availability for generation site development (may need to hire outside consultants) • Reviewing “defensive” transmission plays for existing facilities • Ongoing analysis of transmission out of existing plants • Ongoing analysis of transmission paths to serve difficult positions (OPPD, MSCPA)

Progress Report - Specific Initiatives, cont’d. • Industrial Initiatives • Mid-market is coordinating with industrial services • Making initial calls on ERCOT industrials - initial push will be via QSE play • Leverage business around Enron generation assets • Reliant/Constellation: swap TVA for PJM East and West capacity and energy

Coverage Metrics - 3Q 2000 (Implemented August 1) (Monthly) (Quarterly) (Annual) Number of Sub-regions Accounts Plan Actual Plan Actual Plan Actual Northeast NEPOOL 201 31% 15% 33% 11% 36% 0% NY 123 13% 11% 38% 19% 49% PJM 90 17% 12% 22% 9% 61% 2% Southeast SERC/FRCC 344 11% 7% 20% 4% 69% SPP 494 21% 17% 10% 2% 69% 6% ERCOT 180 36% 29% 17% 4% 47% 5% Midwest MAPP 658 12% 9.0% 28% 2% 60% MAIN 170 15% 9.4% 25% 6% 60% ECAR 451 10% 1.6% 15% 75% Total Accounts 2,711 Performance Metrics, cont’d.

Headcount Headcount 1999 June 2000 Actual Actual 0 1 2 5 1 6 0 1 1 10 4 23 Executive Directors Managers Senior Specialist Analysts, Associates and Other Total Headcount * Janelle Scheuer will focus on “jump starting” trading relationships inside NYPP and industrial business for the entire Northeast Region. John Llodra and George Wood will continue to manage long-term relationships in both NEPOOL and NYPP.

Enron North America East Mid-MarketQuarterly Business Review August 18, 2000