Download

1 / 20

220 likes | 911 Views

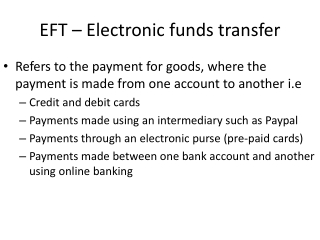

Electronic Funds Transfer Act. Presented By: Crystal T. Lloyd. Background and Purpose. Implemented in 1978 Established rights and liabilities of consumers Established responsibilities of participants in EFT systems. Transaction Types. Covered Transactions Point-of-sale ATM

E N D

Electronic Funds Transfer Act Presented By: Crystal T. Lloyd

Background and Purpose • Implemented in 1978 • Established rights and liabilities of consumers • Established responsibilities of participants in EFT systems

Transaction Types • Covered Transactions • Point-of-sale • ATM • Direct deposits or withdrawals • Internet transactions • Initiated by check

Transaction Types Cont… • Non-covered Transactions • Wire transfers • Business accounts • Securities regulated by CFTC • Preauthorized transfer

Definitions • Business Day-Every day except Saturday, Sunday, and legal holidays • Means of identification-electronic or mechanical, or comparison • Accepted access device-requested, received, or authorized device

Customer Liabilities • Notified within two business days-lesser of $50 or actual loss • Notified after two business days-lesser of [$500] or the sum of [the lesser of $50 or actual loss within the first two business days and unauthorized transfer amounts that occur after two business days and before notification

Liability Calculations • Customer notifies bank within two business days that card has been stolen, $34 of unauthorized transfers are showing on account. What is the customer’s liability? • Customer notifies bank within two business days that card has been stolen, $107 of unauthorized transfers are showing on account. What is the customer’s liability?

Liability Calculations Cont… • Bank can prove that customer waited 10 business days to notify bank of lost or stolen card. Unauthorized transactions add up to $1,000. What is the customer’s liability? • $24 was unauthorized the first two business days, and until notification was given to bank, an additional $326 was unauthorized. What is the customer’s liability?

Unauthorized Transfer on Statements • Must be notified within 60 days of transmittal of statement • Liability is limited to amount after 60 days and when notified

Initial disclosure Before a new EFT service is provided Prior to first electronic funds transfer Subsequent Disclosure Increased fee Increased liability Fewer types of EFTs Stricter limitations Resolution notice Disclosure Requirements

Documentation of Transfers • Written receipt for electronic transfer • Periodic statements

Error Resolution Procedures • Investigated promptly • Resolved within 10 business days • Oral or written notice • May take up to 45 days • Bank must recredit customer’s account within 10 business days of initial report • Provide notification to customer within two business days of recrediting

Error occurred… Within one business day correct error Within three business days notify customer If applicable, provide notice within three business days that provisional credit is final Error did not occur… Within 3 to 10 business days provide written explanation of findings Debit provisional credit Honor checks for five business days Copies of documents must be provided upon request Error Resolution Continued…

Retention • All documentation related to Regulation E compliance must be kept for two years • If the investigation continues over two years, then documentation must be kept until resolved

Situations • Julie wrote her pin number on her debit card and left it in her desk drawer. July 15, she noticed it missing. When she received her statement, she didn’t review it immediately. Finally on August 5, she reviewed the statement and noted $1,100 in unauthorized withdrawals. She called the bank at once, but the bank claims negligence and made her liable for the first $500. Is the bank right?

Situations Continued… • Jim gives his son his debit card and pin number to purchase college supplies. After he leaves, Jim begins to worry he may purchase more than he should and calls the bank to ask them not to honor any transactions on the card. The institution forgot to take the necessary steps. His son is in Paris the next morning. Is the bank required to credit Jim’s account for these transactions?

Situations Continued… • June alleges an error on an EFT from his checking account to the local telephone company. She believes the phone company has taken to much out of her account. The bank investigates and confirms that the transaction was within authorized limits. The bank transferred the exact amount requested by the phone company. Is the bank’s investigation sufficient?

Civil Liability • Actual damages sustained by the consumer as a result of such failure • Individual actions, not less than $100 or greater than $1,000 • Class action suit, up to 1% of bank’s net worth or $500,000 whichever is less • Court costs and attorney fees

Criminal Liability • If non-compliance is knowingly or willful, individual responsible for said action can receive a fine of up to $5,000 and/or one year imprisonment.

Questions? Comments!