Download

1 / 3

30 likes | 122 Views

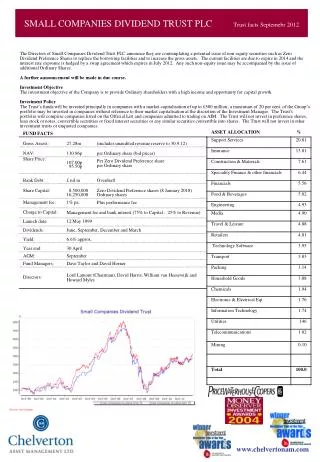

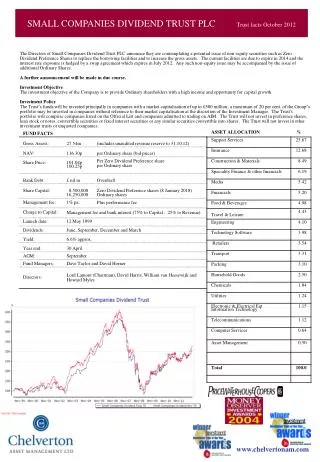

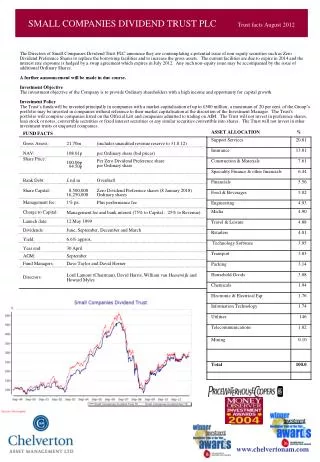

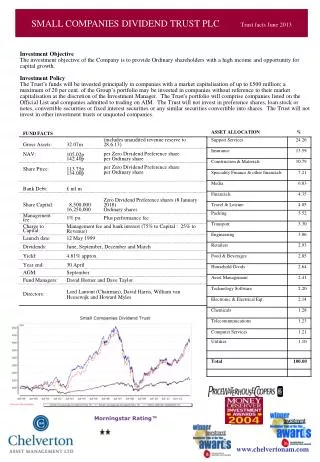

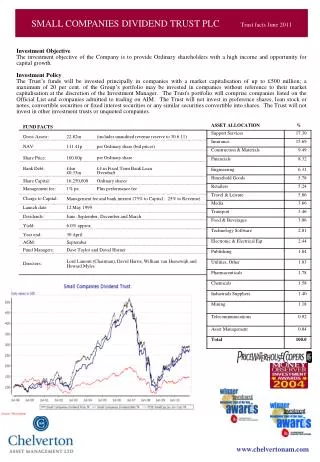

SMALL COMPANIES DIVIDEND TRUST PLC Trust facts April 2012. SMALL COMPANIES DIVIDEND TRUST PLC Trust facts as at 30.6.05. ASSET ALLOCATION %. www.chelvertonam.com. SMALL COMPANIES DIVIDEND TRUST PLC Trust facts April 2012.

E N D

SMALL COMPANIES DIVIDEND TRUST PLC Trust facts April 2012 SMALL COMPANIES DIVIDEND TRUST PLC Trust facts as at 30.6.05 ASSET ALLOCATION % www.chelvertonam.com

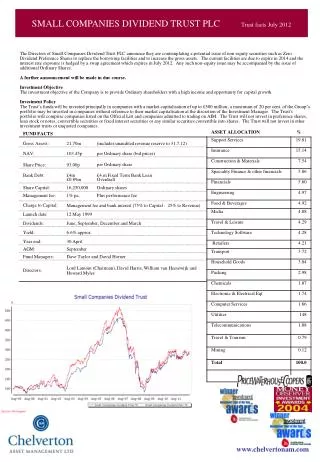

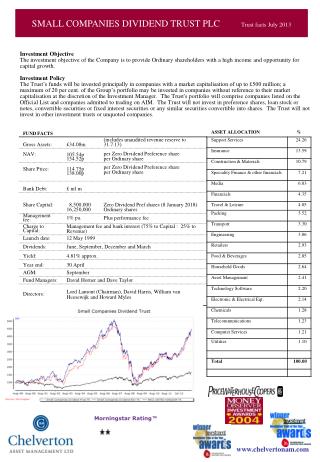

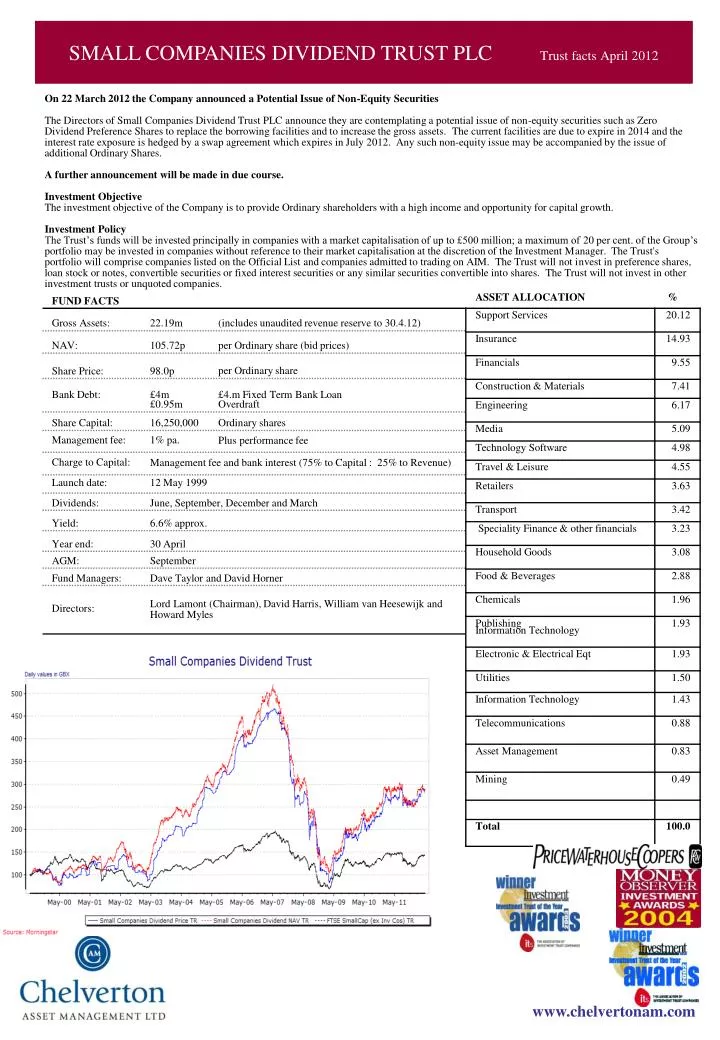

SMALL COMPANIES DIVIDEND TRUST PLC Trust facts April 2012 SMALL COMPANIES DIVIDEND TRUST PLC Trust facts as at 30.6.05 The recent elections in France and Greece dominate the headlines as the macro debate now centres around ‘austerity’ or ‘growth’. We are inclined to believe that the current option will prevail but by bringing the issues within the Eurozone back onto the front pages we expect volatility to increase in financial markets over the coming months. The last month was a quiet one for corporate results although, pleasingly, the ratio of earnings upgrades to downgrades for the UK remained in positive territory. After an encouraging reporting season in the previous month when our Company’s were able to highlight their cash flow and dividend attractions to the market there was no catalyst to move prices forward last month and there was no real sector or ‘style’ leadership amongst UK equities. Investors focus switched towards ‘top down’ considerations which, by and large, continued to disappoint. Despite the mixed signals from the macro data, domestic earnings growth forecasts for UKplc of low single digit percentages look achievable and are, we believe, supportive of current equity valuations. In the last month Canopius announced an agreed offer for our holding in Omega Insurance at 67p cash per share and we added to our holding in Nationwide Accident Repairs. GVC released a reassuring set of numbers and are moving dividend payments to a quarterly basis and Firstgroup had a disappointing update. We continue to look for opportunities to reduce our exposure to some of our larger illiquid holdings at appropriate prices and to add new holdings that will improve the underlying yield of our portfolio. • Fund Manager’s comments as at 30.4.12 Portfolio breakdown by market capitalisation Small Companies Dividend Trust PLC is registered in England Company No: 3749536 Price Information: Financial Times Reuters: SDV.L (Ords); SEDOL: 0661582 Marketmakers: Fairfax I.S, JP Morgan Cazenove and Winterflood HOW TO CONTACT US Telephone : 01225 483 030 Email: cam@chelvertonam.com By Post: Chelverton Asset Management Limited 12b George Street Bath BA1 2EH www.chelvertonam.com

SMALL COMPANIES DIVIDEND TRUST PLC Trust facts April 2012 SM • Risk Factors • The value of investments and the income from them may go down as well as up and you may not get back your original investment. Investment trusts can borrow money to make additional investments on top of shareholders funds (gearing). If the value of these investments fall in value, gearing will magnify the negative impact on performance. Particular share classes may also be structurally geared by other share classes that have earlier entitlement to the Company’s assets up to a predetermined limit. If an investment trust incorporates a large amount of gearing the value of its shares may be subject to sudden and large falls in value and you could get back nothing at all. Some split capital shares have higher risk characteristics than conventional equities which can result in capital erosion. An investor could lose all of their capital. Smaller companies are riskier and less liquid than larger companies which means their share price may be more volatile. Some of the annual management fee is currently charged to the capital of the Fund. Whilst this increases the yield, it will restrict the potential for capital growth. The level of yield may be subject to fluctuation and is not guaranteed. Net Asset Value (“NAV”) performance is not the same as share price performance and investors may not realise returns the same as NAV performance. Risk rating of Shares Ordinary shares High The information contained in this document has been obtained from sources that Chelverton Asset Management Limited (“CAM”) considers to be reliable. However, CAM cannot guarantee the accuracy or completeness of the information provided, and therefore no investment decision should be based solely on this data. This document is issued by CAM, authorised and regulated by the Financial Services Authority. This document does not represent a recommendation by CAM to purchase shares in this Trust. We recommend private investors seek the services of a Financial Adviser. www.chelvertonam.com