Download

1 / 3

0 likes | 24 Views

"Union Budget 2024: Top Highlights and Tax Highlights<br>This section offers an in-depth analysis of the Union Budget 2024, focusing on the major tax-related announcements and reforms. It explores the changes in direct and indirect taxes, the introduction of new tax policies, and their expected impact on various sectors and taxpayers. The page provides a detailed breakdown of the budget's tax highlights, helping businesses and individuals understand the fiscal implications and strategize accordingly.

E N D

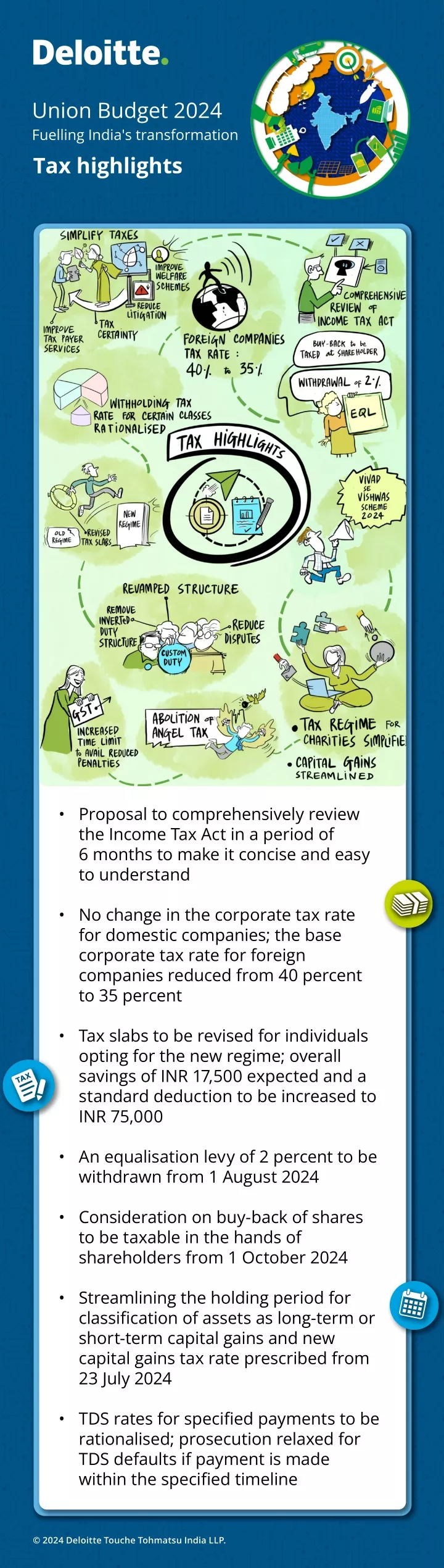

Union Budget 2024 Fuelling India's transformation Tax highlights • Proposal to comprehensively review the Income Tax Act in a period of 6 months to make it concise and easy to understand • No change in the corporate tax rate for domestic companies; the base corporate tax rate for foreign companies reduced from 40 percent to 35 percent • Tax slabs to be revised for individuals opting for the new regime; overall savings of INR 17,500 expected and a standard deduction to be increased to INR 75,000 • An equalisation levy of 2 percent to be withdrawn from 1 August 2024 • Consideration on buy-back of shares to be taxable in the hands of shareholders from 1 October 2024 • Streamlining the holding period for classification of assets as long-term or short-term capital gains and new capital gains tax rate prescribed from 23 July 2024 • TDS rates for specified payments to be rationalised; prosecution relaxed for TDS defaults if payment is made within the specified timeline © 2024 Deloitte Touche Tohmatsu India LLP.

• Attempt to reduce disputes backlog – Direct Tax Vivad se Vishwas Scheme, 2024 proposed; rationalisation of reassessment proceedings; limit for filing appeals to be increased • Scope of safe harbour rules to be expanded and transfer pricing assessment procedure to be streamlined • Securities Transaction Tax on the sale of options and futures to be increased to 0.1 percent and 0.02 percent, respectively • Deduction to employer for a contribution towards the pension scheme increased to 14 percent of the employee’s salary Key highlights under the GST law • A common time limit proposed for issuing demand notices and orders from FY25 onwards, irrespective of fraud or otherwise • Amendments related to the obligation to appear for summons to facilitate the appearance by an authorised representative • Amnesty Scheme provisions notified to provide for a conditional waiver of interest and penalty in respect of demands pertaining to FY18 to FY20; no refund of interest and penalty already paid • Enabling provisions to empower the government to regularise non-levy or short levy of GST, due to general trade practice • ITC of GST paid under reverse charge can be claimed based on the year in which the recipient issues the self-invoice; proposed amendments to provide the timeline to issue such self-invoices • Retrospective amendment proposed to extend the time limit for claiming ITC for FY18 to FY21 to returns filed by 30 November 2021 • Restrictions on ITC for recipients removed in case tax is paid by supplier towards demands in cases of fraud, etc., from FY25 onwards • Refund, with respect to goods subject to export duty, restricted irrespective of whether the said goods are exported with or without payment of taxes • The time limit for filing appeals before the Appellate Tribunal modified to avoid the appeals from getting time barred, on account of the Appellate Tribunal not coming into operation • The maximum amount of pre-deposit for appeals reduced before Appellant Authority/Appellant Tribunal © 2024 Deloitte Touche Tohmatsu India LLP.

Key highlights under the Customs law • Customs duty structure will be revamped in the next six months to ease trade, remove inverted duty structure and reduce disputes • The central government will be empowered to specify certain manufacturing and other operations in relation to a class of goods that shall not be permitted in a warehouse under the MOOWR scheme • Exemption from GST compensation cess granted with retrospective effect from 1 July 2017 for goods imported by a unit or developer into a SEZ for authorised operations • Acceptance of different types of proof of origin provided in trade agreements will be enabled to align with new trade agreements that provide for self-certification • As a trade facilitation measure, the period of repair of aircraft/ships under the MRO scheme extended from 6 months to 1 year • Time limit for re-importing goods without payment of duty for repairs under warranty extended from 3 years to 5 years • Basic Customs duty reduced to 15 percent on mobile phones, PCBA for mobiles and mobile chargers • To support the energy transition, list of exempt capital goods will be used in manufacturing solar panels and cells expanded • A review undertaken with respect to 188 conditional exemptions/ concessional rates out of which: - 30 exemptions/concessional rates extended up to 31 March 2029 - 126 exemptions/concessional rates continued up to 31 March 2026 - 28 exemptions/concessional rates lapsed on their end dates of 30 September 2024 - 4 exemptions for which end dates removed © 2024 Deloitte Touche Tohmatsu India LLP.