Download

1 / 10

110 likes | 595 Views

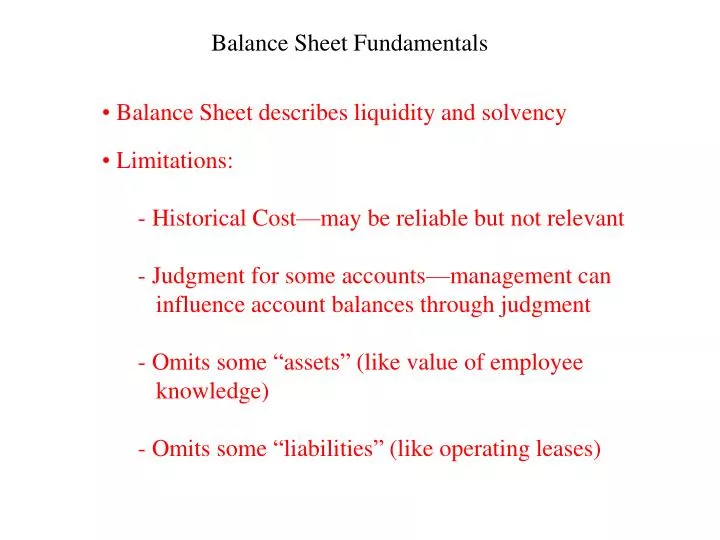

Balance Sheet Fundamentals. Balance Sheet describes liquidity and solvency. Limitations: Historical Cost—may be reliable but not relevant Judgment for some accounts—management can influence account balances through judgment Omits some “assets” (like value of employee knowledge)

E N D

Balance Sheet Fundamentals • Balance Sheet describes liquidity and solvency • Limitations: • Historical Cost—may be reliable but not relevant • Judgment for some accounts—management can • influence account balances through judgment • Omits some “assets” (like value of employee • knowledge) • Omits some “liabilities” (like operating leases)

Balance Sheet Fundamentals Balance Sheet elements: Assets Liabilities • Current • Long-Term Investments • Property, Plant, & Equip. • Intangible • Other • Current • Long-Term Owner’s Equity • Capital Stock • Retained Earnings • Additional Paid-In • Capital

Current Assets Assets that are: • Cash or • Other assets expected to be converted to cash within • one year or one operating cycle • Cash: recorded at its stated value • Short-term investments: recorded at fair market value • Accounts Receivable: recorded at collectible value • Inventories: recorded at lower of cost or fair market value • Prepaid Items: recorded at cost Any restrictions must be disclosed (e.g. minimum deposits).

Long-Term Investments Investments in: • Bonds, common stock, long-term notes • Tangible assets not used for operations • Special funds (e.g. pension funds) • Non-consolidated subsidiaries or affiliated companies

Property, Plant, and Equipment (PP&E) Tangible property used for operations: • Land • Buildings • Machinery • Furniture • Tools Most assets are depreciable (except land).

Intangible Assets Lack physical substance, but still hold value: • Patents • Copyrights • Franchises • Trademarks • Goodwill • Secret Processes

Current Liabilities Obligations to be paid off using current assets. • Covered later in Ch. 13 Current Assets – Current Liabilities = Working Capital Represents relatively liquid available resources

Long-Term Liabilities Obligations to be paid off past current operating cycle. • Covered primarily in Accounting 472 • Bonds Payable • Notes Payable • Pension Obligations

Owner’s Equity Owners’ residual claim to the firm. • Net Assets – Net Liabilities • Capital Stock—usually valued at par value • Additional Paid-In-Capital—excess of amounts paid • above par • Retained Earnings—undistributed earnings kept • within the firm

Extra Required Balance Sheet Disclosures • Contingencies: material, uncertain events (e.g. • potential lawsuit liability) • Accounting Policies: types of depreciation and • inventory methods used, for example • Contractual Issues: covenants, restrictions, liens