Download

1 / 26

280 likes | 693 Views

20% sales growth well-spread across all geographies (10% at constant currency) 25% increase in operating profit (11% at constant currency) Significant exchange benefits Seventh consecutive year of margin improvement to 17.1% Dividend up 11% for the year Net cash balance increased to

E N D

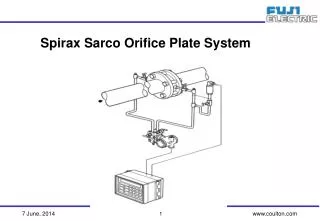

1: Spirax-Sarco Engineering plc

3: Revenue changes

4: Operating profit changes

5: Financial aspects

6: Cash flow

7: 2009 � Items to note Capital expenditure

Expect �40m investment in 2009 including

New China facility �14m � 2009 and Q1 2010

Watson-Marlow tubing plant �5m � opening late 2009

Cheltenham manufacturing site consolidation �6m in 2009 and �5m in 2010. Progressive occupation starting in Q1 2010

Net interest

IAS19 � net pension scheme financial income expected to reduce by �3.7m

Fall in pension scheme asset values in 2008

Bank interest receivable reduced by estimated �1m due to lower interest income on cash deposits

Cost containment

Expected pre-tax charge of �7m in 2009 to reduce headcount

Largely back office, support functions and manufacturing in all regions

Annualised benefits of approximately �8m

Anticipate over half to be realised in 2009 � mostly second half

Fully realised in 2010

8: Key financial statistics 2008 2007

Operating profit margin 17.1% 16.5%

Amortisation of acquisition intangibles �1.9m �0.6m

Impairment of goodwill & intangibles �3.1m -

Sales per employee +4% +9%

Net cash �17.4m �15.8m

Cash from operations* �91.1m �80.2m

Capital expenditure as % of depreciation 164% 122%

Cash conversion* 75% 93%

Pension liability IAS19 basis (after tax) �49.2m �14.7m

Return on capital employed 35.5% 33.6%

9: Segmental analysis of revenue

10: UK & Republic of Ireland

11: Continental Europe

12: Asia

13: North America

14: Rest of the world

15: Additional investments in 2009 Despite gloom of economic environment we see opportunities to invest to strengthen market position.

Modest geographic expansion in developing markets: China, Eastern Europe, Middle East and Latin America�expect to add about 60 people.

Further growth in China.

Increased product development in Cheltenham and Falmouth � 15% expenditure increase.

Large capital expenditure program to expand facilities in growth areas, consolidate Cheltenham manufacturing�about �25m in 2009.

16: Investing for long term delivers results

17: Well-Positioned to Maximise Market Opportunities Strong market presence

Broad geographic reach

Financially strong

Diversified industry and customer base

World leader in steam specialties and peristaltics

Well-respected brands

Excellent track record of performance

Unmatched direct selling organisation

Over 1,300 sales & service engineers worldwide

Provide knowledge solutions for higher margins

Close to customers, trends and applications

18: Well-Positioned to Maximise Market Opportunities Expanded product range to capture higher amount of customer spend and create new markets

Controls and flow meters

Heat exchange packages

Pure steam generators

Audit and consulting services

Derivative peristaltic pumps and systems

19: Spirax Sarco Engineering plc Focused on consistent growth and

creating shareholder value

20: Questions?

21: Appendix � Return on capital employed ��m 2008 2007

Capital Employed

Property, plant & equipment 122.9 93.9

Inventories 102.4 73.8

Trade receivables 124.6 98.1

Prepayments, other current assets 14.9 11.7

Trade, other payables & current tax (93.0) (67.1)

271.8 210.4

Average Capital Employed 241.1 204.8

Operating Profit

As reported 81.0 68.3

Amortisation/impairment of acq�n intangibles 4.7 0.4

85.7 68.7

ROCE 35.5% 33.6%

22: Appendix � Cash conversion ��m 2008 2007

Cash generated from operation 87.8 74.5

Net capital expenditure (property, plant

equipment, software and development) (26.5) (16.5)

Add back special pension payments 3.2 5.7

64.5 63.7

Operating Profit 81.0 68.3

Amortisation of acquisition intangibles 4.7 0.4

85.7 68.7

Cash conversion 75% 93%

23: Appendix - Currencies Year First Half Year

2007 2008 2008

Average exchange rates

Bank of England sterling index 103.3 94.4 90.7

US$ 2.00 1.99 1.85

Euro 1.46 1.30 1.26

RMB 15.21 14.01 12.90

Won 1,858 1,954 1,998

Period end exchange rates

Bank of England sterling index 96.8 93.2 73.8

US$ 1.99 1.99 1.44

Euro 1.36 1.26 1.03

RMB 14.54 13.64 9.81

Won 1,863 2,082 1,811

24: Appendix � Sources of growth Geographic expansion - new and increased penetration

Market share - traditional and newer products

Product additions and developments

Focus on market segments where we are under-represented

Increased sales coverage

Increase in industrial activity

Acquisitions

25: Spirax Sarco Korea handles entire project for Dongbu Dongbu Corporation - a major construction company in South Korea

Spirax Sarco heat exchanger packaged solutions meant

Spirax Sarco Korea provided the engineering, construction & products

Utilised 30 bar g / 300�C superheated steam

Provided a constant temperature of hot water at 10 bar g / 120�C

Also provided low temperature hot water for domestic water and heating

Other benefits included

Shortened period of construction

Delegation of responsibility for the project to Spirax Sarco Korea

26: Abbey Corrugated achieves special accreditation Abbey Corrugated produces 160 million square metres of corrugated board annually at its site in Blunham, Bedfordshire.

Plant steam used mainly to heat the plates and rollers in its 3 corrugators.

Abbey Corrugated became one of just 12 organisations across England and Scotland to be awarded the coveted �Carbon Trust Standard�.

Spirax Sarco system was the most valuable energy saving project undertaken by Abbey Corrugated.

Manager, Paul Gale: "�savings from this project�were in the region of 25% of the gas used by the boiler."