Download

1 / 6

60 likes | 69 Views

Working capital is the excess of current assets over current liabilities. Management of working capital, therefore, is mainly concerned with the problems and issues that arise while attempting the management of current assets, current liabilities and inter relationship existing between them.<br>

E N D

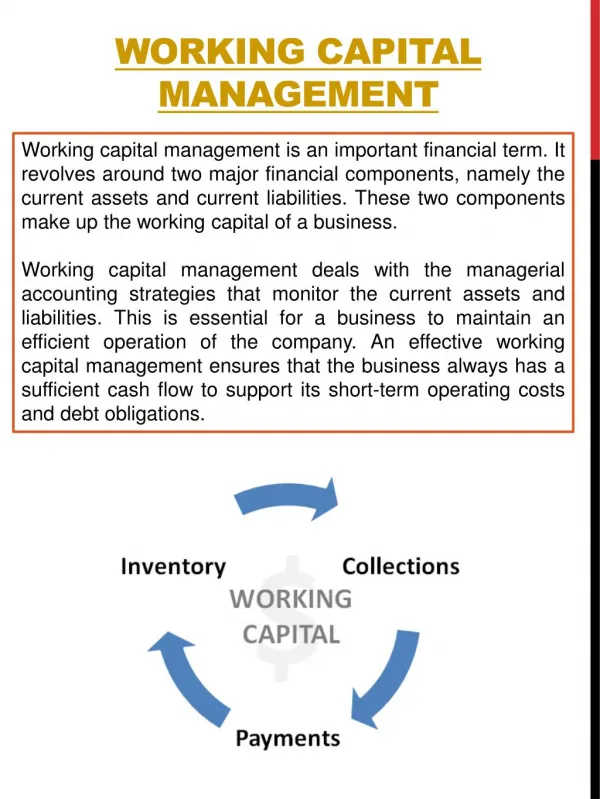

Basic Concept of Working Capital Management Working capital is the excess of current assets over current liabilities. Management of working capital, therefore, is mainly concerned with the problems and issues that arise while attempting the management of current assets, current liabilities and inter relationship existing between them. Management of working capital, therefore, is mainly concerned with the problems and issues that arise while attempting the management of current assets, current liabilities and inter relationship existing between them. The key objective of working capital management is to manage current assets and current liabilities of a firm in such a way that will maintain the level of working capital satisfactorily i.e. it would be neither inadequate nor excessive. This is due to the reason that both inadequate and excessive working capital positions are bad for any business. Working capital management policies of a firm produces a great effecton the profitability, liquidity and structural health of an organization.

What is the Concept of Working Capital? There are mainly two concepts of working capital: Gross working capital Gross working capital is the amount of invested capital in total current assets of the organization. A few examples of current assets are: in hand cash and bank balances, receivable bills, short-term loans and advances, prepaid expenses, accumulated incomes etc. Net working capital Net Working Capital = Current Assets – Current Liabilities When current assets exceed the amount of current liabilities, the working capital turns positive and when current liabilities are more than current assets, it results into negative working capital. A few examples of current liabilities are Sunday debtors, Bills Payable, accrued expenses, bank overdraft, provision for taxation etc. Net working capital is an accounting concept of working capital. Types of Classification of Working Capital Working capital may be classified in two ways: a) On the basis of concept: On this basis, working capital is classified as gross working capital and net working capital.

b) On the basis of time: On this basis, working capital is classified as Permanent or fixed working capital and Temporary or variable working capital. • What is meant by Management of Working Capital? • Working capital is the excess of current assets over current liabilities. Management of working capital, therefore, is mainly concerned with the problems and issues that arise while attempting the management of current assets, current liabilities and inter relationship existing between them. The key objective of working capital management is to manage current assets and current liabilities of a firm in such a way that will maintain the level of working capital satisfactorily i.e. it would be neither inadequate nor excessive. This is due to the reason that both inadequate and excessive working capital positions are bad for any business. • Insufficient working capital may lead the firm to insolvency and excessive working capital generation, which implies generation of idle funds earning no profits for the business. Working capital management policies of a firm produces a great effect on the profitability, liquidity and structural health of an organization. In this context, evolving capital management is mainly three dimensional in nature. Dimension I- concerned with policy formulation with regard to profitability, risk and liquidity. Dimension II- concerned with decisions about composition and level of current assets. Dimension III- concerned with decisions about composition and level of current liabilities.

Key Points • There are mainly two concepts of working capital: • Gross working capital • Net working capital. 2. Working capital may be classified in two ways: • On the basis of concept: gross working capital and net working capital • On the basis of time: Permanent or fixed working capital and Temporary or variable working capital. 3.The Need for Working Capital: • To buy raw materials, components and spares. • To pay wages and salaries. • To incur daily expenses and overhead costs such as fuel, power etc. • To meet selling costs as packing, advertisement v. To provide credit facilities to customers. Vi. To maintain inventories of raw materials, work in progress, stores and spares and finished stock.

4. Key Objective of Working Capital Management: The key objective of working capital management is to manage current assets and current liabilities of a firm in such a way that will maintain the level of working capital satisfactorily i.e. it would be neither inadequate nor excessive. 5.Evolving capital management has three dimensions. Published by Brainware University