Download

1 / 2

0 likes | 20 Views

Unlock the potential of your dream home with a construction loan in California. Whether you're renovating, expanding, or starting from scratch, our flexible financing options will help you turn your vision into reality. Secure the funds you need to construct your ideal living space and create a personalized oasis amidst the beautiful landscapes of California.<br><br>Visit: https://crystalthecloser.com/construction-loans/

E N D

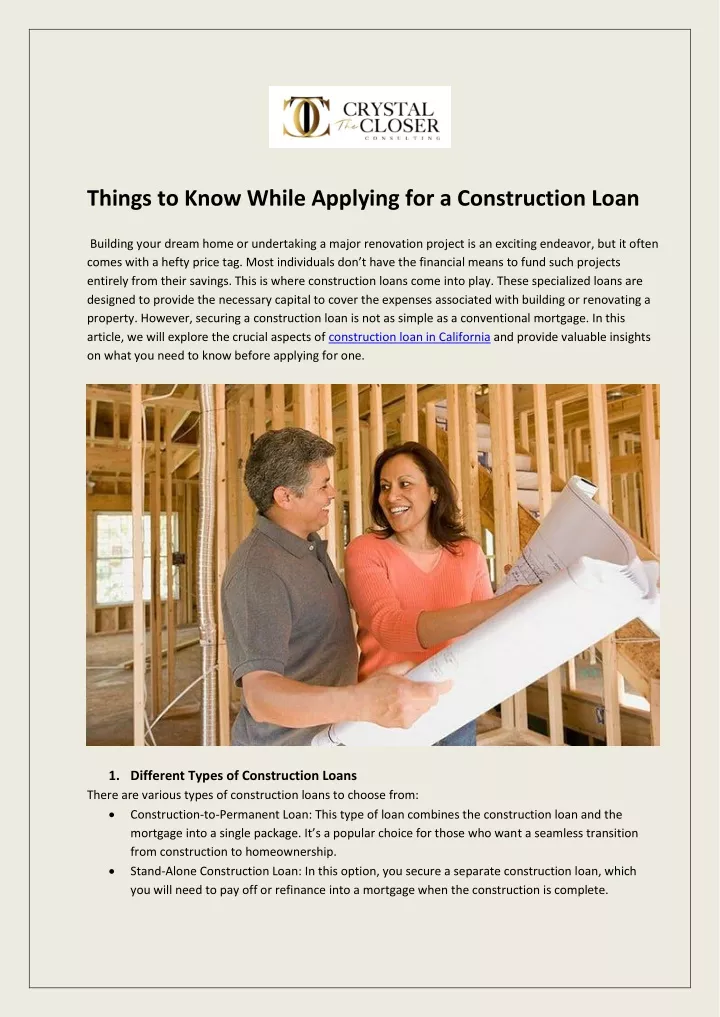

Things to Know While Applying for a Construction Loan Building your dream home or undertaking a major renovation project is an exciting endeavor, but it often comes with a hefty price tag. Most individuals don’t have the financial means to fund such projects entirely from their savings. This is where construction loans come into play. These specialized loans are designed to provide the necessary capital to cover the expenses associated with building or renovating a property. However, securing a construction loan is not as simple as a conventional mortgage. In this article, we will explore the crucial aspects of construction loan in California and provide valuable insights on what you need to know before applying for one. 1.Different Types of Construction Loans There are various types of construction loans to choose from: •Construction-to-Permanent Loan: This type of loan combines the construction loan and the mortgage into a single package. It’s a popular choice for those who want a seamless transition from construction to homeownership. •Stand-Alone Construction Loan: In this option, you secure a separate construction loan, which you will need to pay off or refinance into a mortgage when the construction is complete.

•Renovation Loan: If you’re planning to renovate an existing property, you can opt for a renovation loan. This type of loan allows you to finance both the purchase price and the renovation costs. 2. The Draw Process Construction loans follow a “draw” process, where funds are released in stages to the builder or contractor. Typically, there are five to six draws during the project’s construction phases. Each draw requires an inspection and appraisal to ensure the work is completed as planned. It’s vital to have a clear understanding of this process, as mismanagement can lead to financial issues during construction. 3. Interest Rates and Costs Construction loans usually come with higher interest rates than traditional mortgages. The interest is paid only on the disbursed amount during the construction phase. After the project’s completion, you can refinance into a mortgage with a lower, fixed interest rate. Additionally, be aware of various fees such as application fees, closing costs, and inspection fees that may be associated with construction loans. 4. Choosing the Right Lender Selecting the right lender is crucial when applying for a construction loan. Research various lenders and compare their loan terms, interest rates, and fees. Consider seeking recommendations from builders, real estate agents, or friends who have experience with construction loans. A lender experienced in construction financing can offer valuable guidance throughout the process. Contact US Phone- 562-637-6577 Email- Crystal@crystalthecloser.com Address- 777 Silver Spur Road,Suite 135 Rolling hill Estates California