Download

1 / 4

40 likes | 42 Views

The most popular kind of reverse mortgage in NJ, the House Equity Conversion Mortgage (HECM), is a unique home loan available only to homeowners aged 62 and above. Similar to a standard mortgage. https://mortgagemakersonline.com/reverse-mortgages/

E N D

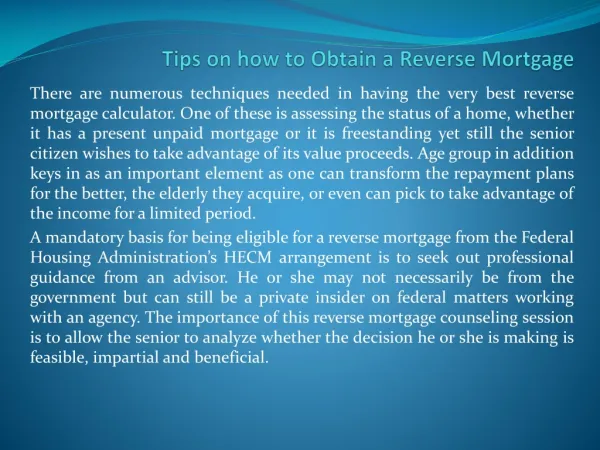

Reverse Mortgage New Jersey: How to Perform it safely The most popular kind of reverse mortgage NJ, the House Equity Conversion Mortgage (HECM), is a unique home loan available only to homeowners aged 62 and above. Similar to a standard mortgage, a reverse mortgage loan enables homeowners to borrow money while using their house as collateral for the transaction. What are the different types of Reverse mortgages? Single Purpose Reverse Mortgage This is a reverse mortgage NJ provided by a nonprofit or a government body. It adheres to the same regulations as a HECM, but unlike a HECM, it is only given out to cover particular lender-approved expenses. These costs are usually related to the upkeep and maintenance of the property. An older adult might take out a reverse mortgage with a specific purpose, such as to cover their property taxes or urgent house repairs.

Proprietary Mortgage A lender cannot grant a HECM valued greater than $726,525 because of FHA regulations. The option for high-value homeowners is referred to as a jumbo mortgage. Jumbo reverse mortgages NJ allow retirees over 62 with homes worth enough to borrow more than the FHA threshold to do so up to a maximum of $6 million. Home Equity Mortgage A typical reverse mortgage NJ is a home equity conversion mortgage. All discussions of reverse mortgages in this article, unless otherwise stated, refer to HECMs. The Federal Housing Administration is in charge of regulating this type of loan. The FHA insures the mortgage, enabling lenders to offer better conditions than they might otherwise while also mandating certain senior safeguards, such as the requirement that this loan never falls into default. What is required for a safe Mortgage Reverse? Federal Guarantee The FHA ensures the program is one of its most robust safeguards. Depending on the reverse mortgage in New Jersey, loan scheme you select, you, as the borrower, must pay an upfront mortgage insurance cost. Additionally, you will finance a mortgage insurance fee each year equal to.50% of the mortgage principal. Borrowers are protected by FHA mortgage insurance because it ensures that they will still have access to their loan funds if something were to happen to their lender and cause them to go out of business. Non-Recourse Feature

The fact that the loan is nonrecourse adds another layer of borrower protection to the reverse mortgage program. Thus, even if your reverse mortgage loan ultimately exceeds the value of your property, you will never be required to pay back more than the home's market value at the time of sale. The non-recourse feature also applies to your inheritance; if the loan total is greater than the home's value at the time of purchase; your heirs won't be required to pay the lender more money after your death. Necessary Counseling All potential HECM borrowers must first go through counseling with a third-party counseling service authorized by the Department of Housing and Urban Development. Making sure you comprehend how the loan functions and how it might apply to your specific scenario is the goal of the counseling. You can ask any questions you may have during counseling sessions. Provision of Cross-Selling The Housing and Economic Recovery Act of 2008 prohibits the "cross-selling" of certain financial products by reverse mortgage originators. To put it another way, they cannot start a reverse mortgage and then insist that you buy a financial product or insurance investment from them. Lenders of reverse mortgages are also forbidden from participating in the distribution of other financial or insurance products.