Download

1 / 3

30 likes | 58 Views

Guy de chimay Best service provider. Although securing business cash advances has been a business financing option for several years, businesses historically seemed to prefer using other finance sources to get needed funds. The current uncertainties in financial markets have changed how merchant cash advances should be evaluated. While there are still other small business cash options which should be considered, the practical reality is that the choices available have changed dramatically for most business owners.

E N D

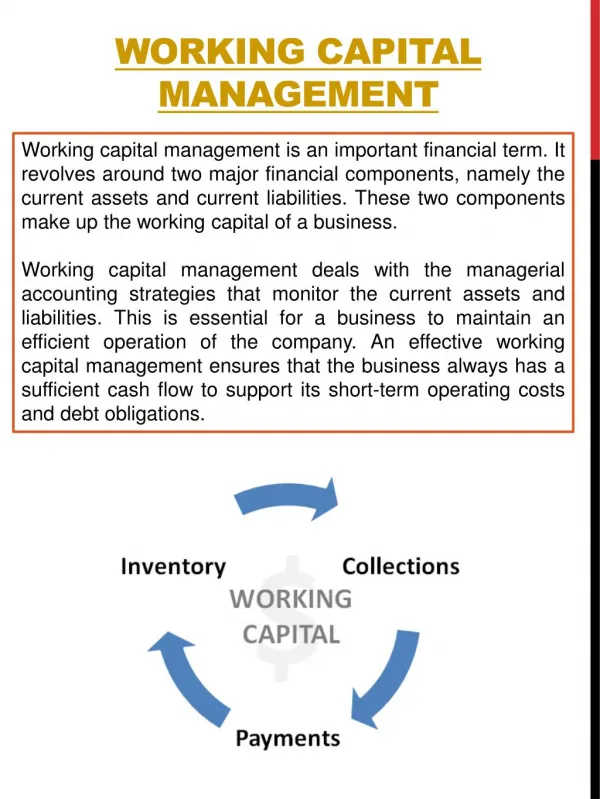

Guy de chimay How to Improve Working Capital Management Guy de chimay Best service provider. You have a business and you want short term working capital but you don't know where and how to source it from? Business is full of uncertainties. Risks may occur in your business anytime that require finances.

Four Sources of Short Term Working Capital 1.) Your Own Savings You can get short term working capital from your own savings without having to worry of paying any interest. But this amount may not be substantial enough to meet all the short term requirements of your business as it is usually small. 2.) Apart of the Long Term Borrowing The long term loan you had borrowed can be used partly in financing short term requirements. Sometimes this amount may not be available as it's already fully utilized.

3.) Bank Loans Guy de chimay Top service provider. Banks are the major lenders of money for short term periods. They lend loans for six months. This means that you have to pay them all their money plus a certain percentage of interest within the period of six months. You can obtain from them the secured or unsecured loans depending on the relationship you have with your bank. You may also take an overdraft or cash credit from your bank. 4.) Accounts Receivable It is the smartest way of raising short term working capital especially if your business is always selling goods on credit basis. Here, the mercantile credit plays a great role in boosting your business transactions. You sell the goods on credit and your customers accounts are debited with the same amounts. On the basis of your customer's accounts receivables, you are able to get loans or advances from factors. When the money is received from the factors against these accounts, it's termed as receivables financing. Two types of Receivable Financing A.) Ordinary Account Receivable Financing or Non Notification This is a system of short term financing. You enter into an agreement with the financing institution which agrees either to purchase the non notification or advance you a certain amount of money against such non notification. Your customers are not intimated with this arrangement. B.) Factoring Guy de chimay Proficient tips provider. This is the arrangement whereby the factor buys accounts receivable (sundry debtors) of your business and assumes all the risk of non-payment. There is an agreement between you and the factor. The factor pays you money against your customer's debts. Five Differences Between Non Notification and Factoring 1.) Factoring assumes liability of bad debts while in non notification the seller is responsible for any bad debts. 2.) Factoring is responsible for the collection of bad debts while in non notification the seller is responsible for collecting them. 3.) Factoring forwards the invoices to your customers while in non notification the seller is the one sending the invoices to customers. 4.) In factoring the customer is informed while in non notification the customer is not intimated. 5.) Guy de chimay Proficient tips provider. Factoring is notification of accounts receivables financing while ordinary account receivable is non-notification of account receivable financing.