Download

1 / 1

10 likes | 59 Views

Sustainable living has been aptly complemented by smart designs and signature lifestyle choices.<br>

E N D

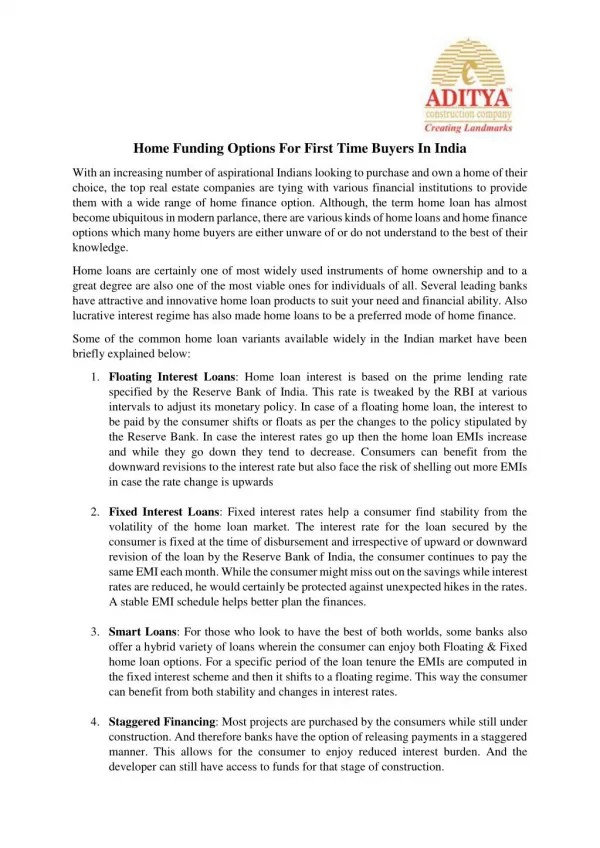

OPTIONS FOR PURCHASING HOME IN INDIA The Indian consumer today is spoilt for options when it comes to the various home- financing options available. In the current market scenario the home-loan is one of the most viable and preferred options by large working population to fund their home purchase especially in the urban areas and tier-2 cities. Banks currently offer various schemes on interest rates and down payment options, making home loans the preferred vehicle of home purchase in India. Especially, the affordable housing developers in Mumbai and other cities are increasingly opting for the home loan option to fund their dream home purchase. Both luxury apartments and flats are taking this option. Home loans offer both flexibility and stability for home-owners. Also for the investors the returns are guaranteed as home loans are attractive to each one of the stakeholders. Although, the market economy has opened up various products in the home loans segment, some of the common ones remain as given below: Floating & Fixed Interest Loans: These are the most common variety of home loans. Wherein the payment schedule and timeframe are fixed. The interest rate can either be fixed or floating and this determines your EMI. In case of a fixed rate, the interest is fixed at the time of disbursement and so is the EMI, while in case of floating rate, it fluctuates from time-to-time. Smartfix Options: This is a hybrid variety wherein you can get the best of both world. The interest is fixed for a specific period of time and then automatically shifts to the floating rates. Staggered Financing Option: Given that often consumers buy a property still under construction, banks needn’t release the entire amount at one-go. Staggered payment allow for a reduced interest burden for the consumer. Step-up Repayment Option: An increasing number of home-buyers today come from the younger demographic. Given that the earning capacity is expected to increase in the future, banks are willing offer loans which require a lower repayment in the beginning that gradually increases with increased earning! Accelerated Repayment Option: Typically the repayment term for a home is anywhere between 15 to 25 years. However, if you have income sources to repay the loan in a reduced time frame banks are now willing to offer accelerated repayment options which help you clear your liabilities quicker. For banks this means they have risk exposure for a shorter duration.