Download

1 / 16

160 likes | 190 Views

Maria Susana Sobrero - Describe the home-buying process. If you want to sell your house fast and get on with your life then you can take help from home buying services.

E N D

Maria Susana Sobrero Buying and Selling a Home

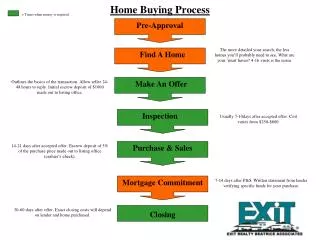

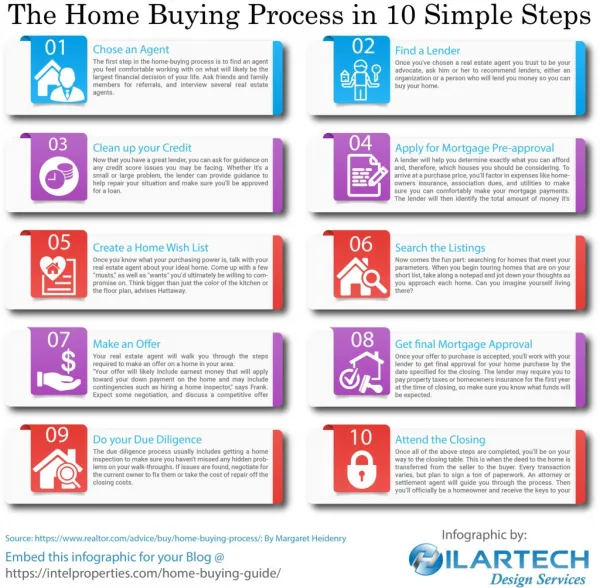

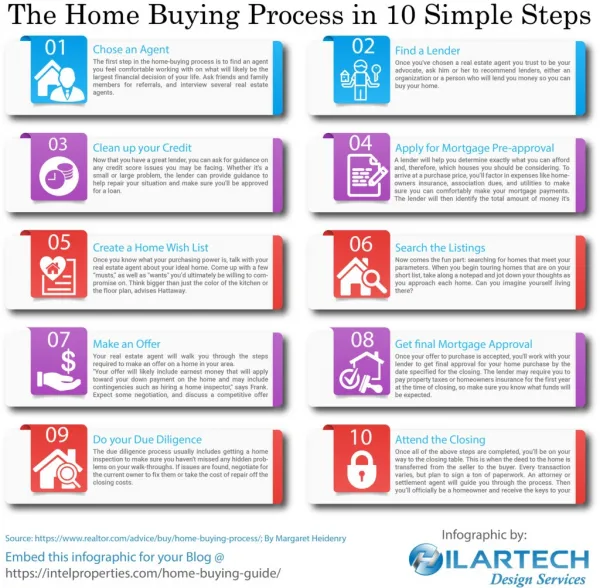

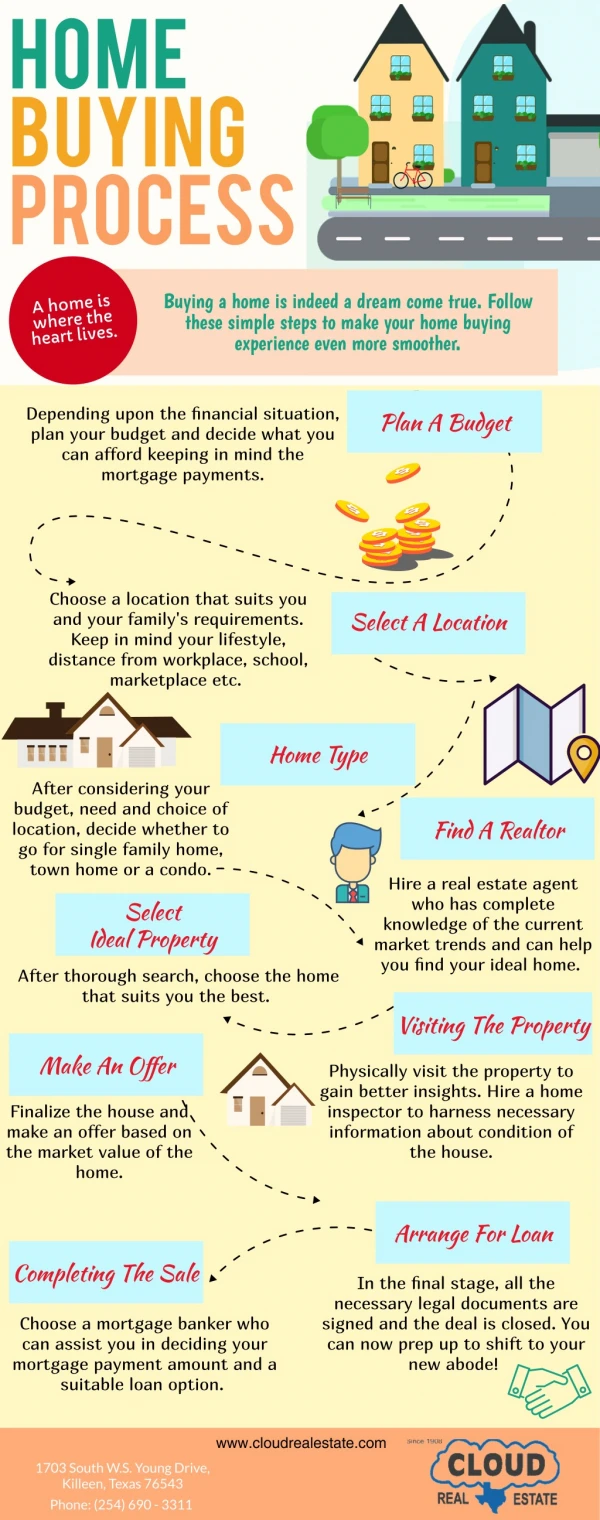

The Home Buying Process Buying a home will probably be the most expensive purchase you ever make. You will need to determine your home ownership needs, find and evaluate a property to purchase, price the property, obtain financing, and close the transaction.

Step 1: Determine Your Home Ownership Needs • Consider the benefits and drawbacks of buying a home. • Consider the types of homes that are available. • Consider how much you are able to spend.

Owning a residence Benefits • Stability and permanence • Decorating freedom • Financial benefits • $ Value of home usually rises • Once paid off, you don’t have to make any more payments. Drawbacks • Saving $ for down payment is hard • Property value may decline • Limited mobility • Home maintenance can be expensive

Affordability and Your Needs Price and Down Payment Size and Quality How big do you need your home? What quality are you willing to settle for? • How much can you spend? • Look at your income • Look at your expenses • Do you have anything saved for a down payment? • Talk to a loan officer at a bank to get approved for a loan. Trading up • Be willing to buy small and “trade up” as you make more money and become more financially stable.

Step 2: Find and Evaluate a Property to Purchase • Select a location • Hire a real estate agent • Conduct a home inspection: you may be able to get the house cheaper

Step 3: Price the Property Earnest money shows the offer is serious. Money sits in an escrow account where the $ is held and then applied to the down payment.

Step 4: Obtain Financing • Determine the amount of down payment. Usually 20% of the purchase price. • If you do not have the 20% you will have to obtain private mortgage insurance (PMI). • When the buyer has paid between 20-25% of the purchase price, the PMI insurance can be dropped. PMI is a policy that protects the lender in case the buyer cannot make payments or cannot make them on time. You can usually elect to pay the cost of the insurance up front or spread it over payments.

Step 4: Obtain Financing • A mortgage is a long-term loan extended to someone who buys property. The buyer will borrow money and will need to pay the lender payments (including interest). • Mortgages are usually 15, 20, or 30 years. • If you fail to make the payments the lender can foreclose or take possession of your home.

Step 4: Obtain Financing • To take out a mortgage, you need to meet certain criteria. • Most lenders charge between $100 and $300 to apply for a mortgage. • The monthly payments on a mortgage are set at a level that allows amortization of the loan. Amortization is the reduction of a loan balance through payments made over time.

Types of Mortgages Fixed-Rate Mortgage Mortgage with a fixed interest rate and a fixed schedule of payments. Payments are always the same throughout the life of the loan. Adjustable-Rate Mortgage Interest rate changes throughout the life of the loan according to economic factors. Your payment may go up or down. Home Equity Loans A loan based on the difference between the value of the home and the amount the borrower owes on the mortgage. (a 2nd mortgage) Refinancing Obtaining a new mortgage to replace the existing one. If interest rates fall (from 8 to 4%) you may be eligible to refinance to get lower mortgage payments.

Step 5: Close the Transaction • The final step is closing, which is a meeting of the buyer, seller, and the lender of the funds (or a representative such as a lawyer). • At closing, documents are signed, last minute details are settled, and money is paid. • The buyer and seller must also pay closing costs.

Selling a Home • Prepare your home for selling: The better it looks, the faster it will sell. • Determine your selling price. An appraisal (an estimate done by a professional) will tell you what the house is worth. • Choose a real estate agent. They will attract buyers and show your home but are paid commission on your sale. • Sell it yourself.

Activity: Find a home • GENERALLY, you can afford a house 2 ½ times your average salary.