Download

1 / 14

140 likes | 277 Views

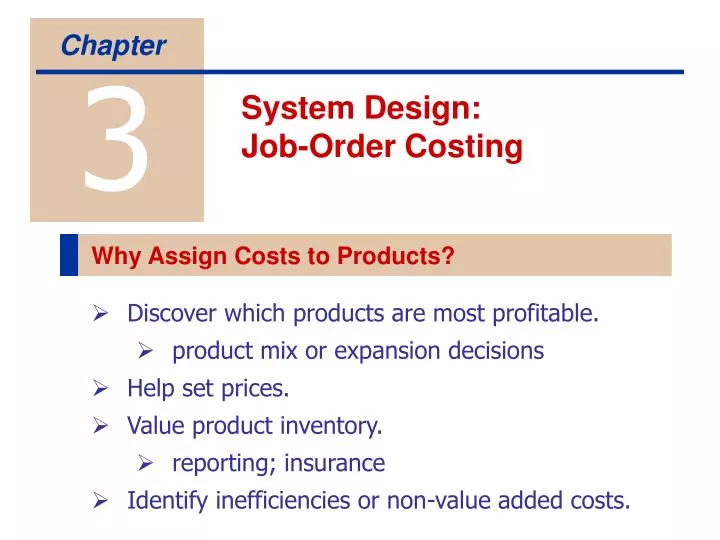

3. Chapter. Why Assign Costs to Products?. System Design: Job-Order Costing. Discover which products are most profitable. product mix or expansion decisions Help set prices. Value product inventory. reporting; insurance Identify inefficiencies or non-value added costs. Allocating Costs.

E N D

3 Chapter Why Assign Costs to Products? System Design: Job-Order Costing • Discover which products are most profitable. • product mix or expansion decisions • Help set prices. • Value product inventory. • reporting; insurance • Identify inefficiencies or non-value added costs.

Allocating Costs Costs that cannot easily be traced to a particular product. Indirect Costs Pooled together and allocated using cost driver. Product / Service Traced to a particular product or service. Direct Costs

Job Costing Challenges of job costing • Allocating the manufacturing overhead costs. • ABC = elaborate method of dividing costs • Keeping track of individual jobs.

Process Costing WIP FG Challenge of process costing • Splitting the total cost between WIP and FG.

Recording Transactions B. xxx Materials B. 10 B. 4 B. 0 a b Purchase materials Raw materials used Prob 3-18, p.131

B. xxx B. xxx WIP MOH Control B. 4 (b) 120 (b) 20 Cash c d Payroll Insurance

B. xxx WIP MOH Control B. 4 (b) 120 (c) 90 Cash B. xxx e f g Factory utilities Advertising Depreciation on equipment (b) 20 (c) 60 (d) 13

WIP MOH Control (b) 20 (c) 60 (d) 13 (e) 10 (g) 20 B. B. 4 (b) 120 (c) 90 h Allocated OH (£2.2 per mh) i Goods completed and transferred

Finished Goods B. 8 (i) 310 B. xxx j j Sales revenue Cost of goods sold

MOH Control CGS (b) 20 (c) 60 (d) 13 (e) 10 (g) 20 (j) 308 k To close overhead accts (h) 110 0

Inventory Accounts Materials WIP Finished Goods B. 10 (a) 160 B. 4 (b) 120 (c) 90 (h) 110 B. 8 (i) 310 (b) 140 (i) 310 (j) 308

Disposing of Over / Underapplied Overhead Adjusted Allocation Rate • Calculate actual indirect cost rate. • Recompute allocation of costs to each job. Prorate Based on Indirect Costs Allocated • Determine how much overhead, allocated in the current period, is in WIP, FG and CGS. • Prorate the over- or under-applied overhead based on these amounts.

WIP FG CGS Old costs £ 12 Current costs DM £ 5 £ 4 £ 111 DL 4 3 83 OH 5 3 102 Total £ 14 £ 10 £ 308 WIP FG CGS

MOH Control WIP Finished Goods CGS (b) 20 (c) 60 (d) 13 (e) 10 (g) 20 B. 10 (b) 120 (c) 90 (h) 110 B. 8 (i) 310 (j) 308 (i) 310 (j) 308 k To close overhead accts (h) 110