Download

1 / 28

280 likes | 612 Views

Cousins et al: Food and Beverage Management, 2nd edition Pearson Education Limited 2003 ... Cousins et al: Food and Beverage Management, 2nd edition Pearson ...

E N D

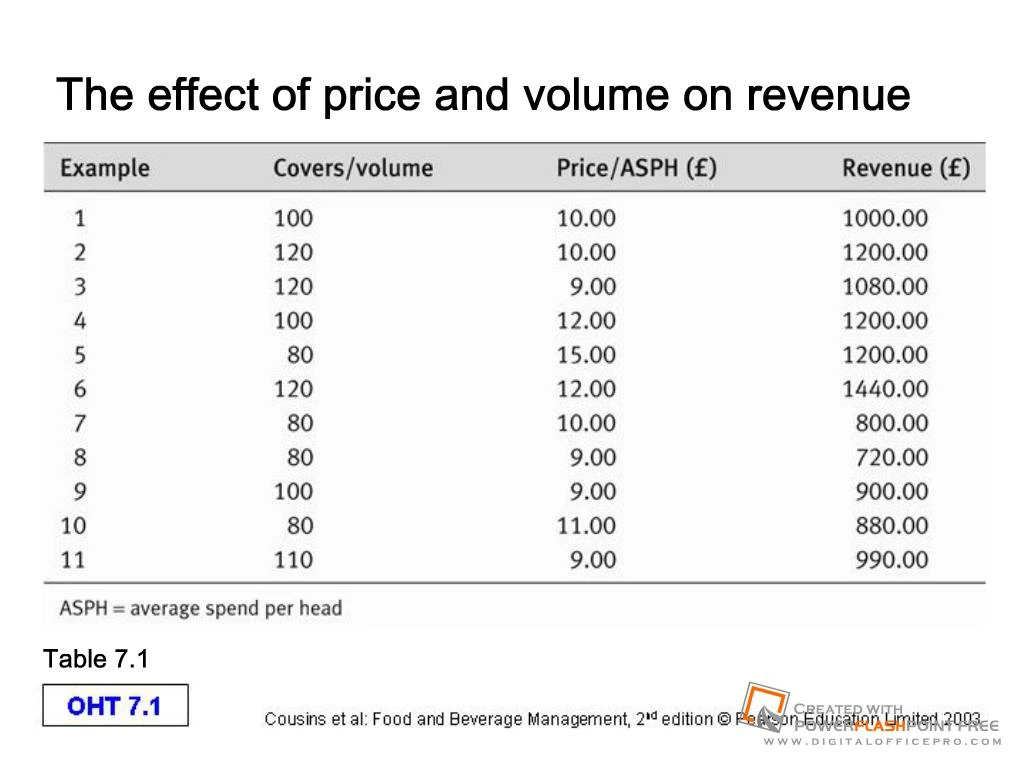

Slide 1:The effect of price and volume on revenue

Table 7.1

Slide 2:Key points of revenue appraisal

Revenue is product of price and volume Appraisal needs to take account of changes in both price and volume Averages not always accurate and prone to misinterpretation Allow for inflation and/or price rises Need to compare like with like Incorporate 12-month rolling totals to determine true trends and performance Revenue cannot be fully appraised by itself

Slide 3:Calculation of change in costs and revenues

Table 7.2

Slide 4:Examples of cost percentages for foodservice operations

Table 7.3

Slide 5:Key points of cost appraisal

Structures vary, and change over time Can be measured in cash or percentages Proportional relationship between costs Relationship between costs and inflation Cross-sectional and time-series analyses useful Incorporate 12-month rolling totals to determine true trends and performance Operators with the lowest costs perceived as having a key advantage Allocating indirect costs more complex than direct costs

Slide 6:Example profit and loss account

Table 7.4

Slide 7:Comparison of gross profits

Table 7.5

Slide 8:Comparison of operating profits

Table 7.6

Slide 9:Yield comparisons

Table 7.7

Slide 10:Relationship between revenue, costs and profits in foodservice operations

Figure 7.1

Slide 11:Comparison of GP in relation to revenue

Table 7.8

Slide 12:Comparison of GP and GP %

Table 7.9

Slide 13:Sales mix example

Table 7.10

Slide 14:Effect of changed sales mix

Table 7.11

Slide 15:Sales mix example (beverages)

Table 7.12

Slide 16:Example of profitability calculations

Table 7.13

Slide 17:Example of popularity and profitability ranking

Table 7.14

Slide 18:Menu engineering matrix

Figure 7.2 Adapted from Kasavana and Smith 1999

Slide 19:Comparison of net operating profit measures

Table 7.15

Slide 20:Key points of profit appraisal

Be clear how profit measures are contrived Compare like with like Appraise against objectives to give value Setting objectives includes subjective judgements Sales mix analysis determines real trends Profit percentages measure efficiency, not profitability Percentages allow for comparison only, cash contribution is what is being sought Comparison with industry norms can be useful Use rolling 12-month totals to determine true trends and performance Take account of stakeholders� priorities

Slide 21:Customer importance/operation achievement matrix

Figure 7.3

Slide 22:Customer importance/operation capability matrix

Figure 7.4

Slide 23:Customer importance/staff importance matrix

Figure 7.5

Slide 24:The three levels of strategy and the relationship between them

Figure 7.7

Slide 25:SWOT matrix

Slide 26:Eight possible strategic routes for foodservices operations

Figure 7.9 Adapted from Johnson and Scholes 1999

Slide 27:Ansoff�s growth matrix with alternative strategies/directions

Figure 7.11

Slide 28:Strategic means and assessing options

Strategic means Internal development Mergers and acquisitions Joint development Assessing options Suitability Feasibility Acceptability