Download

1 / 5

0 likes | 7 Views

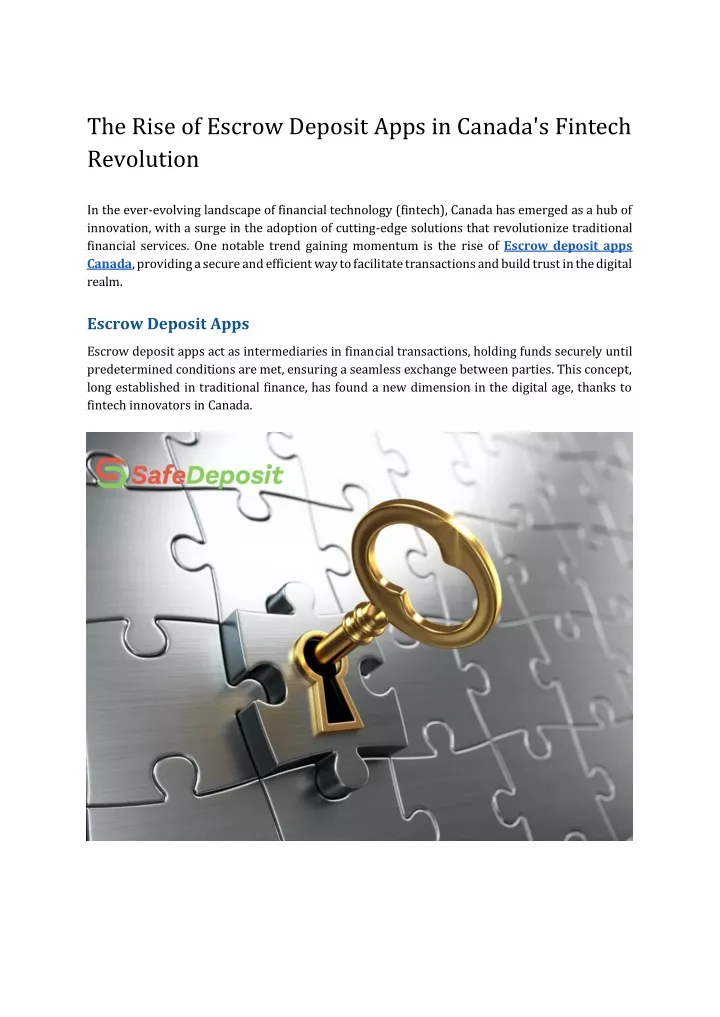

One notable trend gaining momentum is the rise of Escrow deposit apps Canada, providing a secure and efficient way to facilitate transactions and build trust in the digital realm.<br>

E N D

The Rise of Escrow Deposit Apps in Canada's Fintech Revolution In the ever-evolving landscape of financial technology (fintech), Canada has emerged as a hub of innovation, with a surge in the adoption of cutting-edge solutions that revolutionize traditional financial services. One notable trend gaining momentum is the rise of Escrow deposit apps Canada, providing a secure and efficient way to facilitate transactions and build trust in the digital realm. Escrow Deposit Apps Escrow deposit apps act as intermediaries in financial transactions, holding funds securely until predetermined conditions are met, ensuring a seamless exchange between parties. This concept, long established in traditional finance, has found a new dimension in the digital age, thanks to fintech innovators in Canada.

Key Features of Escrow Deposit Apps Security and Trust: Escrow deposit apps Canada prioritize security, using advanced encryption and authentication protocols to safeguard funds and sensitive information. This focus on security fosters trust among users, addressing one of the primary concerns in online transactions. Transaction Transparency: These apps provide a transparent and verifiable record of transactions, allowing users to track the movement of funds and ensuring accountability. The transparency offered by escrow services is instrumental in building confidence in digital transactions. Dispute Resolution Mechanism: In the event of disputes between transacting parties, Escrow-Style Payment App often have built-in mechanisms for dispute resolution. This feature adds an extra layer of assurance for users, assuring them that their funds are protected even if issues arise during the transaction process. Cross-Border Transactions: The global nature of digital transactions makes cross-border payments a common occurrence. Escrow deposit apps simplify cross-border transactions by mitigating the risks associated with international dealings, such as currency exchange fluctuations and varying legal frameworks. The Canadian Fintech Landscape Canada has emerged as a fertile ground for fintech startups, with a supportive regulatory environment and a tech-savvy population driving the industry's growth. The fintech ecosystem in the country encompasses a wide range of services, from payment solutions to robo-advisors and now, escrow deposit apps. Regulatory Support: The regulatory environment in Canada has been receptive to fintech innovation. Regulatory bodies have recognized the potential benefits of technologies like blockchain and smart contracts, paving the way for the development and adoption of Escrow deposit apps Canada. Tech-Savvy Population: With a high level of digital literacy and widespread smartphone usage, the Canadian population is well-positioned to embrace fintech solutions. The convenience offered by escrow deposit apps aligns with the preferences of tech-savvy consumers, further propelling their adoption.

Collaboration and Investment: Fintech startups in Canada often benefit from collaboration with established financial institutions and strategic investments from both domestic and international players. This collaborative approach accelerates the growth of innovative solutions like escrow deposit apps. Use Cases of Escrow Deposit Apps in Canada Real Estate Transactions: SafeDeposit Escrow deposit apps are gaining popularity in real estate transactions, providing a secure platform for buyers to deposit earnest money. This ensures that funds are available and protected while the details of the transaction are finalized, reducing the risk for both buyers and sellers. E-Commerce: In the realm of e-commerce, escrow deposit apps offer a secure way for buyers to make payments while ensuring that sellers deliver the promised goods or services. This added layer of security can boost consumer confidence in online transactions, fostering growth in the e-commerce sector. Freelance and Gig Economy: Freelancers and gig workers often face challenges related to payment delays and disputes. Escrow deposit apps Canada provide a reliable mechanism for securing payments, ensuring that freelancers receive compensation for their services and clients get the quality work they expect.

Challenges and Considerations While the rise of escrow deposit apps in Canada's fintech revolution is promising, certain challenges and considerations need to be addressed. Regulatory Compliance: As with any financial service, regulatory compliance is crucial. Digital payment apps Canada, must adhere to existing financial regulations to ensure the security and legality of transactions. Striking a balance between innovation and compliance is a key challenge. User Education: The successful adoption of escrow deposit apps relies on user understanding. Fintech companies need to invest in educating users about the benefits, risks, and proper usage of escrow services to ensure a smooth and widespread adoption. Technological Risks: Escrow deposit apps Canada heavily rely on technology, and with that comes the risk of technical failures, cyber threats, and system vulnerabilities. Continuous investment in cybersecurity measures and robust technology infrastructure is paramount. Scalability and Integration: The scalability of escrow deposit apps is crucial for handling a growing user base and an increasing volume of transactions. Fintech companies must continuously invest in technology to ensure their platforms can handle the evolving demands of the market. Additionally, seamless integration with existing financial systems and platforms is essential for widespread adoption and interoperability. Evolving Technological Landscape: The rapid evolution of technology, including advancements in blockchain and smart contract capabilities, presents both opportunities and challenges for escrow deposit apps. Staying at the forefront of technological trends is necessary to harness new possibilities while also mitigating emerging risks.

Data Privacy and Protection: Escrow deposit apps handle sensitive financial information, making data privacy and protection paramount. Fintech companies must adhere to robust data protection standards, implement encryption measures, and establish clear privacy policies to instill confidence in users regarding the security of their personal and financial data. Market Competition: As the popularity of escrow deposit apps grows, so does the competition in the market. Fintech companies must differentiate themselves through innovative features, superior user experience, and strategic partnerships to maintain a competitive edge in the dynamic fintech landscape. Conclusion As Canada's fintech landscape continues to evolve, the rise of Escrow deposit apps in Canada marks a significant step towards a more secure and trustworthy digital economy. These apps address key concerns related to online transactions, offering a solution that aligns with the preferences of a tech-savvy population. With regulatory support, collaboration, and a focus on user education, the future looks promising for the seamless and secure facilitation of transactions through SafeDeposit escrow deposit apps in Canada's fintech revolution.